![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

Energy markets are trying to digest what a Trump presidency means for oil and gas prices. While the bulk of Trump’s policies are expected to be bearish for prices, the key upside risk is how the future president deals with Iran.

“We will drill, baby, drill” – Or maybe not so much

“We have more liquid gold than any country in the world,” Trump mentioned in his victory speech, which ties in with previous comments from the president-elect that the US will “drill baby, drill." And while the incoming administration will hold a more favourable view towards the oil and gas industry, ultimately the potential for production growth is going to be largely dictated by price. There is additional upside to US oil production, but we do not think it will significantly move the needle. According to the quarterly Dallas Fed Energy Survey, oil producers need US$64/bbl to profitably drill a new well, and the Kansas Fed Energy Survey shows a similar number. This compares to 2025 and 2026 forward prices of around $70/bbl and $67/bbl respectively.

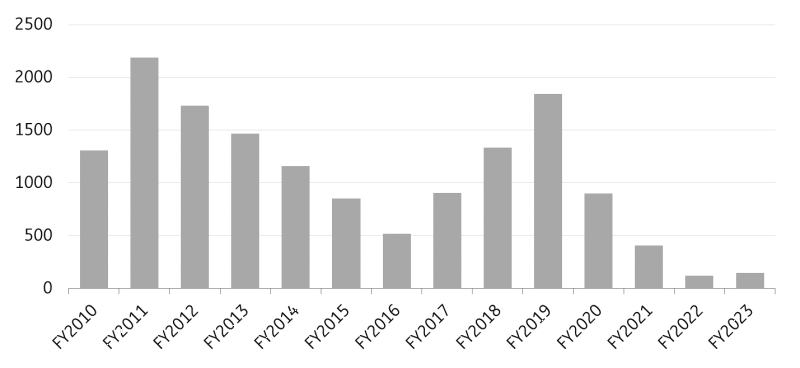

The potential additional growth in US output is likely to come from federal lands with a reversal of some of President Joe Biden’s policies – although it may take a while until we see the impact of this. Onshore oil production on federal lands made up around 12% of total output in 2023; if you include offshore production, this share grows to around 26%. The Biden administration reduced lease sales on federal land and also increased royalty payments and bond requirements for production on federal land. If we compare the number of new leases issued during Trump’s first three years in office, it totalled more than 4,000. In Biden’s first three years, new lease issuances totalled a little over 1,400. However, lower issuances of leases are having little impact on output so far, with oil production on federal lands growing every year that Biden has been in office.

Any upside in oil production would likely also provide upside to natural gas output through associated production. A Trump presidency may also provide more certainty to the industry and provide comfort to them to invest in pipeline infrastructure, alleviating a persistent bottleneck for the US natural gas market, particularly in the Permian region. Investment in natural gas pipeline capacity also leaves the potential for stronger crude oil output.

In addition, under Trump's presidency we are likely to see a lifting of Biden’s pause on LNG export project approvals. While this does not change the short to medium-term outlook for the global LNG market, it will help remove some of the longer-term uncertainty around LNG supply.

Oil & Gas lease issuances on federal land grew under Trump but slowed under Biden

Source: BLM, ING Research

Could energy get caught up in trade tensions?

Trade uncertainty is another factor that could have a negative impact on energy prices, specifically when it comes to US energy prices. Our house view is that Trump is likely to focus on domestic issues initially, but his attention will turn to trade eventually. This could happen in late 2025/early 2026.

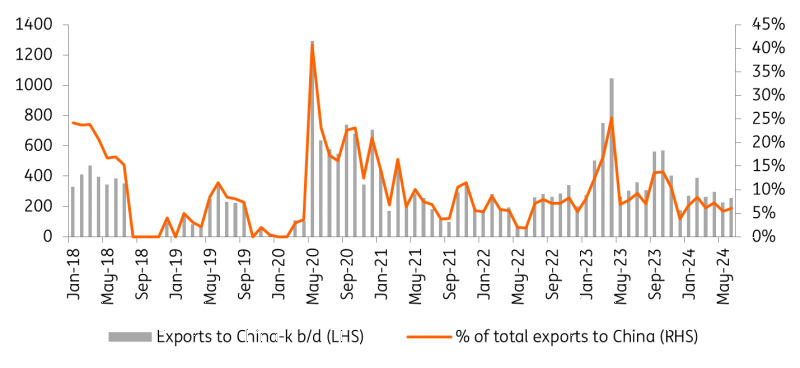

The potential for growing trade friction will likely provide headwinds to energy prices, particularly if energy trade gets entangled in any of these tensions. US trade tariffs could see retaliatory action taken against the US on some exports, much like we saw from China during the 2018 trade war. Chinese oil buyers were reluctant to purchase US crude oil due to the risk and the eventual implemention of tariffs. This saw the WTI-Brent discount widen from around US$3/bbl to more than US$11/bbl in 2018. A ratcheting up in the trade war with retaliatory tariffs – or even the risk of tariffs – could see the WTI-Brent spread coming under pressure once again. However, we may not see as much pressure on the spread given that in early 2018, close to a quarter of US crude exports went to China, while this share has fallen to around 7% currently.

For natural gas, the risk arises from LNG exports. In 2018, China imposed retaliatory tariffs of 10% on US LNG imports, which were then increased to 25% in June 2019. This saw US LNG exports to China fall to zero and they only started to recover when China issued tariff waivers as part of the trade deal. Since 2018, there have been large shifts in the global gas market, with a tight LNG market and Europe a significantly more important buyer of US LNG – which may provide some comfort to the US, if China were to target US LNG. But timing is important as there is a significant amount of LNG capacity set to start up towards the end of this decade, and this is likely to push the LNG market to a buyer’s market.

A smaller portion of US Crude Oil exports end up in China

Source: EIA, ING Research

Trump and foreign policy

For energy markets when it comes to foreign policy, how president-elect Trump will handle the Russia/Ukraine war and the Middle East conflict will be most important. Trump has said that he will bring an end to the Russia/Ukraine war, but it is unclear how he will go about doing so. However, managing to broker a peace deal would likely remove a large amount of geopolitical risk hanging over energy markets. It is unclear whether any peace deal would also involve the removal of certain sanctions against Russia.

It is difficult to see a scenario where Europe agrees to increase its reliance once again on Russian fossil fuels. It would be in the interest of the US that Europe continues to shun Russian fossil fuels, given the US oil and gas industry has been one of the key beneficiaries of this move.

The Middle East is the other geopolitical factor that continues to hang over energy markets. While Trump is supportive of Israel (which was evident during his previous term), he has said that he would look to bring peace to the region. This will be no easy task. It's possible that he aims to achieve this by taking an aggressive stance against Iran, which would also put pressure on Iran’s proxies. Any de-escalation would take a large risk premium out of both the oil and gas market.

Iran sanction risk

The biggest potential impact of an incoming Trump presidency could come from his stance against Iran. It was Trump who re-imposed sanctions against Iran in 2018, which saw a significant fall in Iranian oil exports. And while President Biden did not lift these sanctions, they have not been strictly enforced. This has allowed Iran to increase exports significantly during President Biden’s term. The upside risk for the oil market is that Trump once again takes a hawkish view against Iran and strictly enforces these sanctions. This leaves the potential for a loss of more than 1m b/d of supply from the oil market. This would be enough to erase the surplus that we currently expect through 2025 and would require us to revise our current 2025 Brent forecast of US$72/bbl.

Trump would likely try to counter any strength in oil prices as a result of this by pressuring OPEC+ to increase output. This was a fairly common occurrence during his previous term.

Read the original analysis: What a Trump presidency means for Oil and gas markets

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD under pressure near 1.0350 after mixed sentiment data

EUR/USD remains in the negative territory near 1.0350 in the European session on Tuesday, erasing a portion of Monday's gains. The pair is undermined by risk aversion and the US Dollar demand, fuelled by US President Trump's tariff threats, and mixed sentiment data.

GBP/USD drops to 1.2250 area on broad USD strength

GBP/USD stays under bearish pressure and trades deep in the red near 1.2250 on Tuesday as the USD gathers strength following US President Trump's tariff threats. The data from the UK showed that the ILO Unemployment Rate edged higher to 4.4% in the three months to November.

Gold price eases from over two-month top on stronger USD, positive risk tone

Gold price (XAU/USD) retreats slightly after touching its highest level since November 6 during the early European session on Tuesday and currently trades just below the $2,725 area, still up over 0.50% for the day.

Bitcoin fails to sustain the $109K mark after Trump’s inauguration

Bitcoin’s price steadies above the $102,000 mark on Tuesday after reaching a new all-time high of $109,588 the previous day. Santiment’s data shows that BTC prices quickly corrected, as social media showed major greed and FOMO among the traders in Bitcoin after President Donald Trump’s inauguration.

Five keys to trading Trump 2.0 with Gold, Stocks and the US Dollar Premium

"I have the best words" – one of Donald Trump's famous quotes represents one of the most significant shifts to trading during his time. Words from the president may have a more significant impact than economic data.

Trusted Broker Reviews for Smarter Trading

VERIFIED Discover in-depth reviews of reliable brokers. Compare features like spreads, leverage, and platforms. Find the perfect fit for your trading style, from CFDs to Forex pairs like EUR/USD and Gold.