Weekly wrap: What the heck just happened?

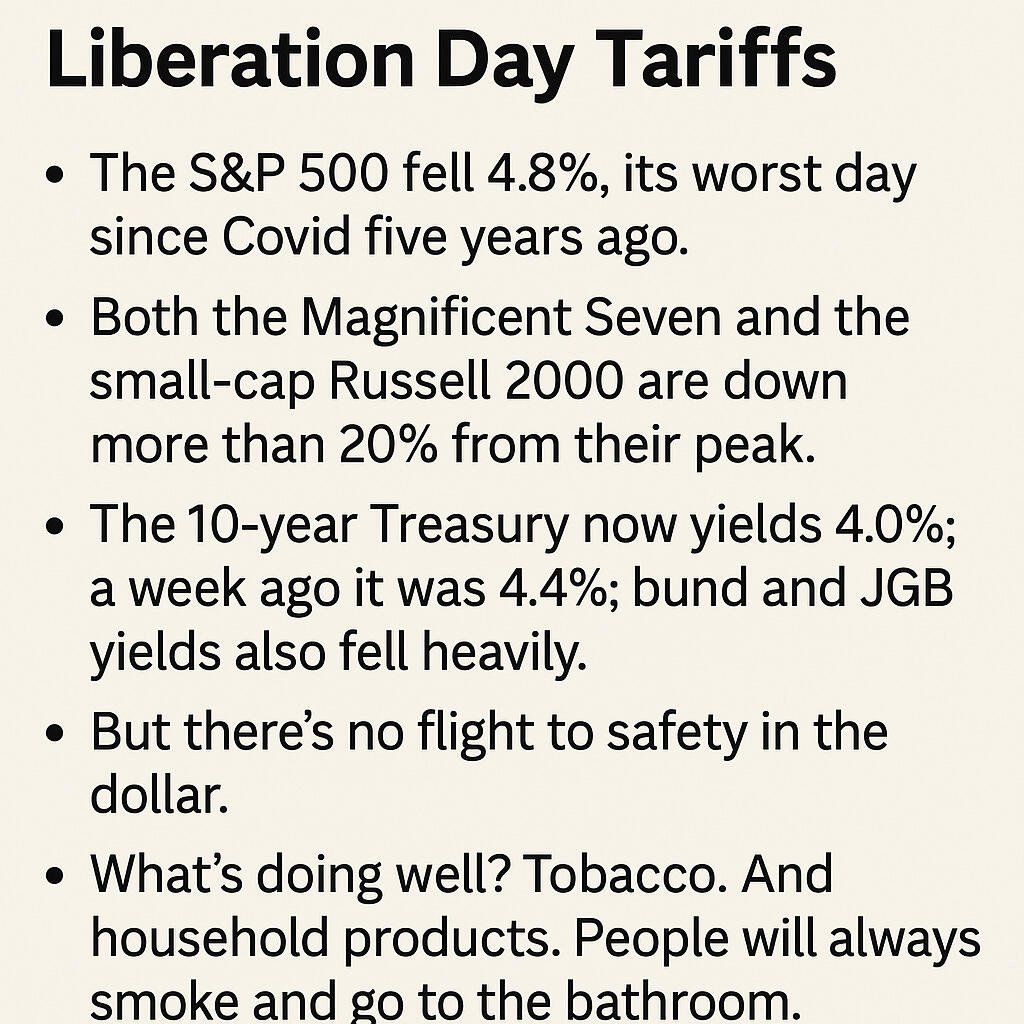

Markets buckled Thursday under the weight of Trump’s Liberation Day tariffs — a policy shift so jarring it sparked the worst single-day selloff since the Covid panic. The S&P 500 cratered 4.8%, while the once-bulletproof Magnificent Seven and small-cap Russell 2000 both plunged into bear market territory, down more than 20% from peak. Bonds, unsurprisingly, caught a bid as investors dove for duration — the 10-year Treasury yield collapsed from 4.4% to 4.0% in a matter of days, dragging bunds and JGBs with it. But the classic risk-off playbook broke at the currency level: there was no flight to the dollar. That’s the market’s tell — capital isn’t looking for safety inside the U.S., it’s looking for the exits.

The tariffs, branded “reciprocal,” are anything but. Instead of matching tariff for tariff, the Trump administration rolled out a policy that penalizes countries based on their trade surplus with the U.S., using a bizarre formula that’s already been memed by economists. It’s not a trade negotiation tool — it’s a surplus hit list. The higher your net exports to America, the harder you get smacked. As Paul Krugman put it, the logic is mathematically tortured; as investors put it, it’s economically destabilizing. The new policy nukes the old concept of reciprocity and treats trade as a zero-sum arena, with Washington unilaterally deciding who’s ‘too successful’ at selling into its market

This is where the deeper risk lies. Since the Global Financial Crisis — and even more so post-Covid — U.S. equities have been the world’s money box. Foreign investors, particularly Europeans, have plowed trillions into U.S. markets, riding not just the equity rally but the strong dollar and the reflexive feedback loop that comes with it. In FX-adjusted terms, the S&P 500 delivered a staggering 140% return over five years. That era may have just ended. As tariffs threaten to choke trade flows, capital flows — which move far faster — are next. The dollar’s failure to rally on Thursday is a warning: foreign capital may already be rebalancing out. Apple, a poster child of global tech exposure, has already shed nearly $1 trillion in market cap — more than Walmart’s entire peak valuation. If these policy shocks persist, Big Tech becomes a liability, not a lifeboat.

The irony? Trump may be getting what his economic team wanted. Treasury Secretary Bessent and his mentor George Soros have long understood market reflexivity — that markets create their own reality. They aimed for a weaker dollar, cheaper oil, and lower long-end yields to re-energize U.S. competitiveness. On paper, all three are happening. But they’re happening for the wrong reasons. The yield curve is falling because growth fears are accelerating, the dollar is weak not from diplomacy but from capital outflows, and oil is cheaper because markets are now bracing for a slowdown in global trade volumes. You can’t call that a soft landing. You call that financial whiplash.

Defensive rotation is already underway. Household staples and tobacco stocks are catching a bid — not because they’re exciting, but because they're bulletproof to geopolitical chaos and trade fragmentation. The brutal truth is that in times of uncertainty, people still smoke and go to the bathroom. Meanwhile, everything else — growth, innovation, cyclicals — is under pressure. Investors are shifting out of the U.S. and into less exposed markets, and this repricing could accelerate. This isn’t just a selloff; it’s a regime change.

The only real off-ramp is political. Historically, Trump has made 20+ tariff threats and walked most of them back. But this one was different — premeditated, branded, and backed by a surreal new “doctrine” of trade imbalance retaliation. Unless polling turns ugly or inflation rips through the consumer base (which it might — tariffs are inherently inflationary), this policy could stick. And if it does, we’re entering a world where capital reroutes, trade shrinks, and U.S. outperformance becomes a memory, not a baseline.

Bottom line: throw out the 2020–2024 playbook. A weaker dollar, falling yields, and Big Tech pain no longer signal a Fed pivot — they may now mark the start of a global repositioning away from U.S. assets. The virtuous cycle has cracked. Whether it snaps outright depends on what Trump does next — or what the market forces him to undo.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.