Weekly FX chartbook: Fed to start its rate cut cycle

Key points

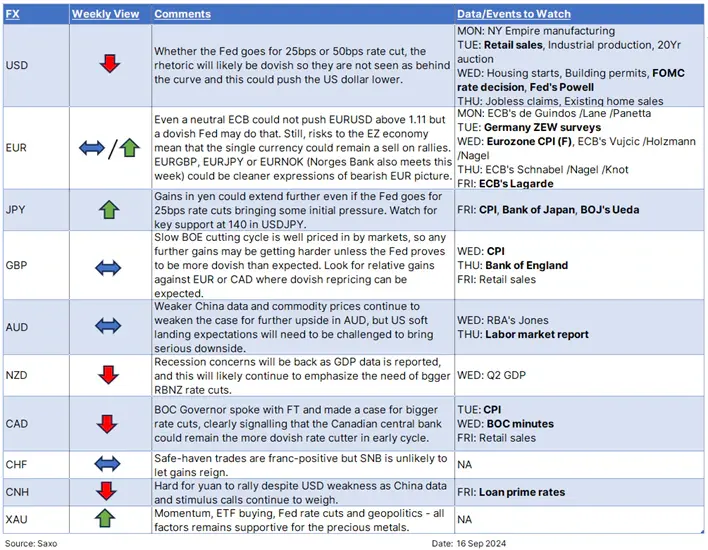

- USD: 25 or 50bps, Fed will be dovish.

-

JPY: More gains likely on Fed-BoJ divergence and safe-haven demands.

-

EUR: Sell on rallies amid Eurozone economic headwinds.

-

GBP: Resilience on test as BOE path is well priced in.

-

CNH: China’s growth concerns fuelling more stimulus calls.

USD: Fed’s dovish stance, Dot Plot and Powell on watch

The debate over the size of the upcoming FOMC rate cut remains undecided, with the market still weighing a 25bps versus a 50bps reduction. While recent data, like August’s stronger-than-expected core CPI, supports a 25bps cut, the narrative has increasingly shifted towards a 50bps move. A recent Wall Street Journal article from Fed whisperer Nick Timiraos and comments by former NY Fed President Bill Dudley have fueled speculation about a more aggressive cut.

If the Fed opts for a 25bps cut, expect dovish rhetoric, potentially setting the stage for a 50bps cut in November or even an inter-meeting adjustment if the labor market weakens significantly. The upcoming labor market data will be crucial as the Fed looks to balance its easing path with maintaining inflation expectations and its data-driven approach.

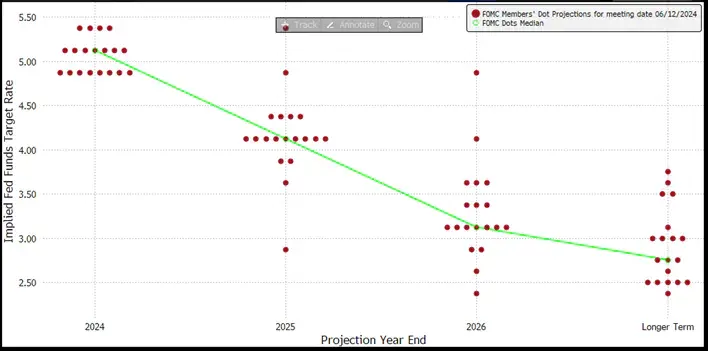

In terms of the dot plot, the 2024 projections are expected to show 2-3 cuts, up from just one in June, signaling a dovish shift. However, the key focus will be on 2025, where a faster pace of cuts could risk signaling recession fears. The Fed is likely to communicate a measured approach to easing, aiming for gradual adjustments to reflect evolving inflation and employment conditions, rather than a rapid, reactive shift.

Fed's June Dot Plot. Source: Fed, Bloomberg

In market terms, a 25bps cut could initially bring higher US Treasury yields and the USD, but Powell is likely to come out dovish in his press conference. That means any bounce in yields or US dollar is likely to be short-lived, with the broader soft-dollar trend expected to persist, especially if the Fed signals a more aggressive easing trajectory.

JPY: Both Fed and Bank of Japan decisions this week

The Japanese yen has strengthened to 140 against the US dollar for the first time since 2003 as markets are increasing the odds of a bigger rate cut from the Fed this week. But it’s not just the prospects of a dovish Fed that is pushing yen higher, but also a mildly hawkish Bank of Japan that announces its policy decision on Friday.

Even though no further policy normalization is expected from the BOJ this week, Governor Ueda is likely to maintain the hawkish tone heard in previous press conferences, with several BOJ members indicating their openness to further rate hikes if the economic outlook remains aligned with expectations. This has been laying the groundwork for rate increases as soon as October.

The yen is also benefitting from lower oil prices and its safe-haven traits that give it an edge to act as a hedge if U.S. equities re-price lower on weaker growth projections. A break below the key 140 level signals potential for further upside for the yen in the near term.

GBP: Outperformance could start to get selective

The upcoming week will be crucial for the GBP, with key events including UK CPI, retail sales, and the Bank of England meeting. UK swaps are currently pricing in only a 22% chance of a 25bps rate cut from the BoE, reflecting a high bar for any rate change. Consequently, unless CPI data significantly deviates from expectations, major shifts in swap pricing or GBP movement are unlikely.

Although services inflation is expected to rise in August, this is primarily due to base effects in areas that the BoE tends to overlook. The Bank has already indicated that it anticipates a temporary rise in services inflation this autumn before it eases by year-end.

Given the persistently high services inflation, the BoE is proceeding more cautiously compared to the Fed regarding rate cuts, and a policy change this month seems unlikely. The committee is not expected to adopt a more dovish stance just yet.

The BoE is anticipated to maintain the current 5% rate, with the voting split potentially impacting GBP movement. A 6:3 split might suggest more urgency for easing putting pressure on sterling, while an 8:1 split could imply less immediate pressure. With the BOE path also well priced in by markets, GBP may face challenges in making further gains, so it might be more prudent to focus on currency crosses, particularly those offering relative outperformance against the EUR or CAD where dovish repricing remains plausible.

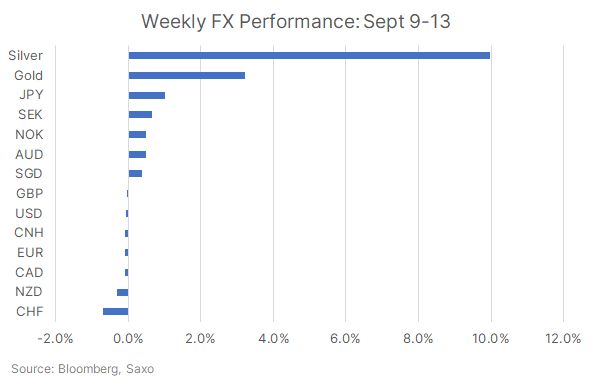

A highly skewed FX performance chart for last week with Silver outperforming with 10% gains. Gold and yen also gained as market positioned for Fed rate cuts, and USD ended lower for a second consecutive week.

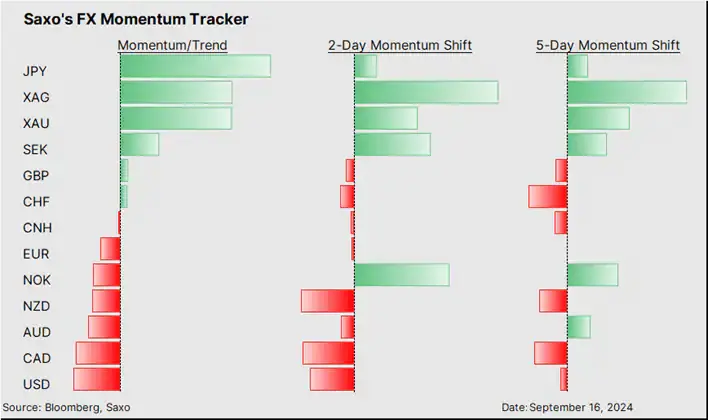

Our FX Scorecard shows bullish momentum increasing in Silver and Scandi currencies, while being maintained in JPY and Gold. NZD, CAD and USD see bearish momentum building.

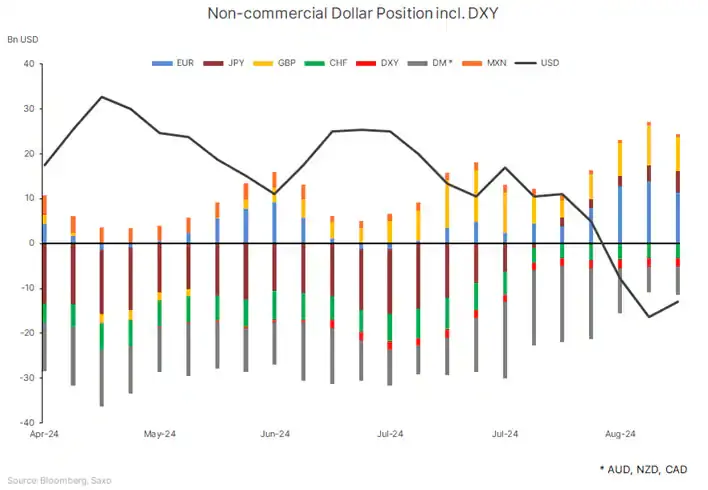

The CFTC positioning data for the week of 10 Sept saw some short-covering in USD against all other major currencies expect the JPY and CHF. Longs were liquidated mostly in EUR and GBP, followed by AUD and NZD.

Read the original analysis: Weekly FX chartbook: Fed to start its rate cut cycle

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.