Week ahead: What are the financial markets watching this week

The week that was:

RBNZ slashed rates by 50bps

The week kicked off with the Reserve Bank of New Zealand (RBNZ) reducing its Official Cash Rate (OCR) by 50 basis points (bps) to 4.75%, a move that was widely expected and marked the central bank’s second consecutive rate cut this year.

The RBNZ signalled that further rate reductions are in the pipeline but depend on the ‘evolving assessment of the economy’. Money markets are currently pricing in 44bps of easing for November’s meeting (assigning a 76% probability that the central bank will cut the OCR again by another 50bps).

This week, attention now shifts to CPI inflation numbers (Consumer Price Index).

Federal Open Market Committee (FOMC) Meeting Minutes – ‘Substantial Majority’ Supported 50bp Cut

The minutes from the September FOMC meeting revealed that all US Federal Reserve (Fed) officials supported a rate reduction. Yet, while a 50bp cut was not unanimous, a substantial majority supported a 50bp rate decrease.

Members also agreed it was ‘appropriate’ to continue reducing the Fed funds rate. If data continued to come in as expected – inflation slowing to 2.0% and ‘the economy near maximum employment’ – it would be appropriate to move to a more neutral policy stance over time.

The minutes emphasised that the pace of reductions would be based on ‘incoming data, the evolving outlook, and the balance of risks’. Additional points in the minutes were that ‘almost all’ members observed upside risks to the inflation outlook have diminished, and weaker employment conditions increased.

US inflation stalls

US CPI inflation surprised to the upside in September, reinforced by shelter and food costs. Still, despite higher than median estimates, headline CPI inflation slowed to 2.4%, observing its slowest rise in three years compared to a year ago and marking a sixth straight month of deceleration. Excluding food and energy costs, nevertheless, core CPI inflation increased 3.3%, up from 3.2% in August. The latest inflation data will be the last print before Americans head to the polls next month.

The inflation update is unlikely to alter the Fed’s current trajectory. The Fed is expected to cut the funds rate target by 25bps at the November meeting (22bps of easing is currently priced in), following the central bank reducing the rate target by 50bps at September’s meeting to 4.75-5.00%.

The FP Markets research team added the following in a recent post:

‘Granted, September’s inflation numbers are mixed and a little more uneven than the Fed would like, but this is still likely sufficient to warrant a 25bp rate cut next month. Overall, though, the US economy is faring well; economic activity is running at an annualised pace of 3.0%, and employment is strong – September’s release showed US non-farm payrolls added 254,000 jobs, and unemployment dropped to 4.1% from 4.2% in August’.

UK GDP rose in August

As expected, UK real GDP (Gross Domestic Product) grew by 0.2% in August, returning to growth after two consecutive months of stagnation. The Chancellor of the Exchequer, Rachel Reeves, welcomed this news as she prepares to deliver her first UK Annual Budget Release on 30 October.

Overall, the latest numbers leave the UK economy on track for growth in Q3 24, yet it will be slower than in the year’s first half.

The week that is:

UK

It will be a busy week regarding tier-1 economic metrics for the UK, each delivering data that could shift the chances of a rate cut for the remaining two meetings this year (November and December). Markets are pricing in 37bps of easing until the year-end, with an 80% probability of a 25bp cut assigned to November’s meeting.

The FP Markets research team added the following in a recent post:

‘Of relevance, the latest batch of data follows dovish comments from BoE (Bank of England) Governor Andrew Bailey in an interview with the Guardian, which marked a notable shift in tone. Bailey underlined that the central bank could become ‘more aggressive’ in easing policy should inflation continue to subside. Bailey also called for a ‘gradual approach’ in September after the central bank held the Base Rate steady at 5.00% in an 8-1 vote; you will also recall that the BoE reduced the Rate by 25bps in August’.

Investors will receive August’s jobs data from the UK on Tuesday at 6:00 am GMT. The unemployment rate is expected to have remained at 4.1%, and employment change is forecast to have dropped to 250,000, down from July’s reading of 265,000. Average earnings will also be of particular focus. Early estimates reveal that regular pay and pay that includes bonuses slowed to 4.9% (from 5.1% [July]) and 3.8% (from 4.0% [July]), respectively, in the three months to August. Some analysts forecast a rebound in wages, potentially underpinning a hawkish rate repricing and likely triggering an unwind in GBP (British pound) short positions. However, in the event of broad softness in wage growth, a dovish rate repricing and GBP downside are expected.

UK CPI inflation data for September will be a key watch on Wednesday at 6:00 am GMT and is forecast to have moderated across both headline and core measures. Headline (YoY) inflation is expected to have cooled to 1.9% from 2.2% in August (estimate range falls between 2.3% and 1.7%). You will recall inflation clipped the BoE’s 2.0% target in June before elbowing to 2.2% in July and August. Excluding energy, food, alcohol and tobacco, core (YoY) inflation is anticipated to have eased to 3.4% from 3.6% (August), with the estimate range currently between 3.5% and 3.2%. This measure has stubbornly circled just north of 3.0% since May. Interestingly, according to the BoE’s latest projections (August), CPI inflation is expected to remain above 2.0% in 2025 and fall below target in 2026. Services inflation, of course, will also be monitored closely by both the BoE and investors; YoY, economists expect to see the measure slow to 5.3%, down from 5.6% in August (which rose from 5.2% in July – its lowest level since mid-2022).

Finally, UK retail sales data will be released on Friday at 6:00 am GMT, with markets anticipating a sharp deterioration of 0.3% from August to September (prior: 1.0%). Nonetheless, September (YoY) is expected to have risen 3.2%, up from August’s 2.5%. Albeit an event that can trigger short-term volatility across GBP pairs, the release is unlikely to alter rate pricing much.

US

The US calendar will be thin this week and follows US CPI inflation stalling and the bumper jobs data for September.

US retail sales data for September will be making the airwaves on Thursday at 12:30 pm GMT; analysts expect a 0.3% rise MoM, extending the mild acceleration seen in August (0.1%). We have a broad estimate range to work with here between 0.7% and 0.0%. Excluding autos, core retail sales are forecast to have grown 0.2% from 0.1% in August (estimate range between 0.4% and -0.2%).

This could boost the US dollar (USD) if data report higher-than-expected numbers this week, particularly at or exceeding upper estimate values. Of relevance, the USD Index recently ventured north of major resistance at 102.78 on the daily chart and retested the area as support. Deprived of notable resistance, follow-through upside from here could have the greenback shake hands with the 200-day simple moving average, currently at 103.75.

Additional data will include regional manufacturing surveys from New York and Philadelphia Fed banks on Monday and Thursday, respectively.

Canada

Canadian CPI inflation numbers for September will be out on Tuesday at 12:30 pm GMT. CPI inflation is anticipated to have slowed again at the headline level to 1.8% (YoY), with the estimate range currently between 2.0% and 1.7%.

For reference, August’s CPI inflation cooled to 2.0% (YoY), down from 2.5% in July and south of economists’ expectations of 2.1%. August’s reading also marked the first time since February 2021 that the headline inflation rate has hit the Bank of Canada’s (BoC) 2.0% inflation target and highlights the eighth consecutive month that headline inflation has remained within the central bank’s inflation band of 1-3%.

The BoC’s preferred measures of inflation will also be closely watched. The CPI Median is expected to rise 2.3% (YoY), matching August, while the CPI Trim measure (YoY) is forecast to rise 2.5%, up from August’s print of 2.4%. Assuming data matches estimates, the average pace of inflation between these two measures would be 2.4%, marking a slight uptick from August’s 2.35%.

This week’s inflation data will be a key watch for traders, and could be pivotal in determining whether the BoC opts for a 25 or 50bp cut. Markets are pricing in 37bps of cuts for the October meeting and a total of 75bps until the year-end (the final meeting is on 11 December). You will note that the central bank cut the Overnight Rate for a third consecutive meeting in September to 4.25% and signalled that further rate cuts are on the table should progress on inflation continue.

New Zealand

Inflation data out of New Zealand will be particularly important on Tuesday at 9:45 pm GMT and may help determine whether the RBNZ opts for another bulkier 50bp reduction in November or a more traditional 25bp cut. This follows the RBNZ cutting its OCR by 50bps. As noted above, markets are pricing in 44bps of easing for said meeting (77% probability in favour of a 50bp decrease).

CPI inflation for Q3 24 (YoY) is expected to have cooled to 2.3% and ease back into the RBNZ’s target inflation band of 1-3%; the estimate range is between 3.3% and 2.0%. The RBNZ’s latest projections have Q3 24 CPI inflation at 2.3% and domestic inflation (or non-tradeable inflation) at 5.1% (YoY); the latest release showed that non-tradeable inflation rose 5.4% in Q2 24 (YoY), down from 5.8% in Q1 24.

Economic activity in New Zealand has been largely at a standstill since exiting a mild technical recession in the second half of 2023. Q2 24 data contracted by 0.2%, down from Q1 24’s paltry 0.1% expansion. The unemployment rate is also at its highest since early 2021 at 4.6% (Q2 24).

Australia

This week’s focus in Australia is the September jobs market, which will be announced at 12:30 am GMT on Thursday. The report is expected to show a decrease in employment to 25,000 from 47,500 in August, with some economists anticipating the unemployment rate to tick higher to 4.3% (from 4.2% in August). An uptick in the unemployment rate will likely underpin an AUD (Australian dollar) bid, possibly altering rate pricing and nudging a rate cut into view this year.

The Reserve Bank of Australia (RBA) next meets in November; while many G10 central banks have kicked off their easing cycle, the RBA is expected to remain on hold at 4.35% for an eighth consecutive meeting amid sticky inflation and robust employment growth.

Europe

The European Central Bank (ECB) is widely anticipated to reduce policy by 25bps on Thursday at 12:15 pm GMT – bringing the Deposit Rate to 3.25% – amid softening CPI inflation data and weak growth metrics. As of writing, investors have fully priced in the cut, with another 25bp reduction expected at December’s meeting. A rate cut this week would follow rate reductions in June and September.

Broadly weaker manufacturing and services PMI numbers (Purchasing Managers’ Index) were seen for September. This consequently dragged the composite PMI output Index into contractionary terrain to 48.9 from 51.0 in August.

Headline (YoY) CPI inflation stepped below the central bank’s 2.0% target to 1.8% in September, its lowest rate since April 2021; the slowdown in inflation was driven by a fall in energy prices. Additionally, core inflation – which excludes energy, food and tobacco – slowed by 0.1 percentage points to 2.7% in September, and services inflation cooled to 4.0% in September from 4.1% in August.

With the rate cut fully priced in, guidance will be important to monitor here as investors look for clues on the ECB’s next moves, namely how fast and how much rates will fall.

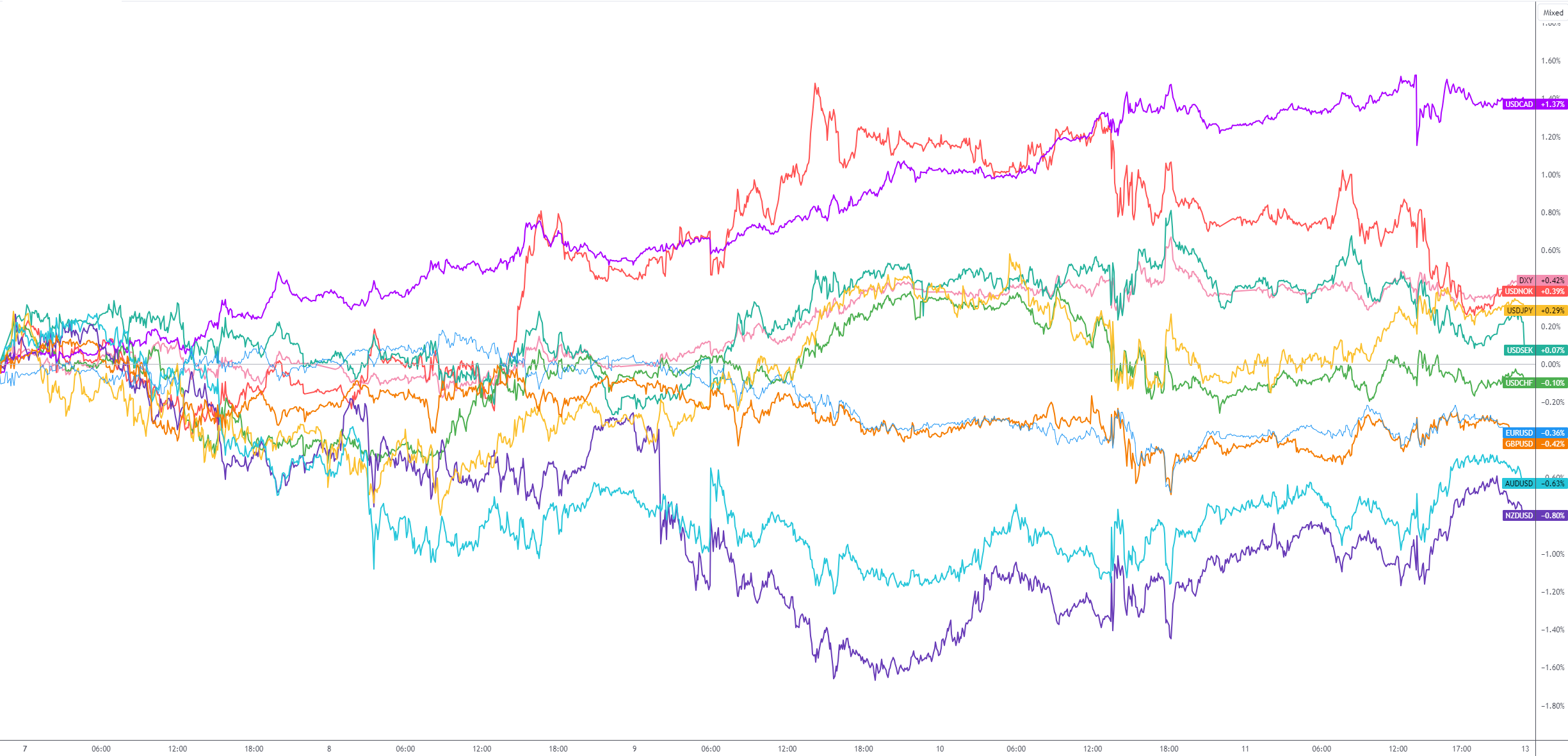

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,