Week ahead: What are markets watching this week?

Despite a holiday-shortened week in the US, most major US equity indices refreshed record highs, and US Treasury yields fell, along with the US dollar, which shed nearly -1.0% against major peers.

Cooling US economic conditions increasing odds of a September cut

Minutes from the latest FOMC meeting last week stressed that Fed officials remain cautious and await further evidence of disinflation before having the confidence to begin easing policy. However, economic conditions display signs of cooling, and the pendulum appears to be swinging in favour of rate cuts.

Last week’s headline June US ISM PMIs fell short of market expectations; given the colossal miss on the services print, both manufacturing and services are now in contractionary territory. The services PMI dropped to its lowest level in four years at 48.8, five points lower than May’s release at 53.8 and comfortably south of the market’s median estimate of 52.5. Friday’s jobs data also firms up expectations of a forthcoming rate cut. The non-farm payrolls report showed 206,000 jobs were added to the US economy in June, slowing from May’s downwardly revised 218,000 print though slightly bettering Bloomberg’s median estimate of 190,000. The unemployment rate ticked higher to 4.1% in June (the highest rate since late 2021), up from 4.0% in May, while June’s average hourly earnings for both month-on-month and year-on-year measures cooled from previous levels, as expected (rising +0.3% [down from +0.4% in May] and rising +3.9% [down from +4.1% in May], respectively). Regarding market pricing, swaps traders see little chance of a rate reduction this month; September’s meeting is firmly on the table (-20 basis points priced in currently), with 46 basis points of easing priced in for the entire year.

Across the pond, another risk event of note last week was euro area CPI inflation, which came in as expected, slowing to +2.5% in the twelve months to June, marking a slowdown from +2.6% in May. Core inflation, which strips out food and energy components, was unchanged at +2.9% over the same period. This will offer some relief for the European Central Bank (ECB), which, in what was an exceptionally well-telegraphed move, reduced its three key benchmark rates at the June policy meeting. Many desks forecast the central bank will hold rates at this month’s meeting; markets are pricing in about a 70% chance of a hold and 44 basis points of easing for the year.

Landslide Labour victory

Last week, we also had the UK general election. In reality, few surprises were seen, and the markets reacted accordingly. Sir Keir Starmer’s Labour party swept to power in a landslide victory, ending a 14-year Tory reign. While there were all smiles in pictures last week, the newly appointed Prime Minister has quite a task ahead, including cutting NHS waiting lists and confronting and tackling the issue of illegal immigration.

The week ahead

This week welcomes a handful of event risk investors will closely monitor, including Fed Chair Powell testifying before the Senate Banking Committee, US CPI inflation, and an update from the Reserve Bank of New Zealand (RBNZ).

Investors will also closely watch how the markets respond to Sunday’s second round of French elections. As most will already be aware, there is a chance of a Hung Parliament, but there is no clear majority at this stage. You will recall that European stock markets and the EUR/USD rose at the open last week following Marine Le Pen’s hard-right National Rally party failing to secure an absolute majority.

Fed Chair Powell’s testimony and US CPI inflation

Federal Reserve Chair Jerome Powell will speak before the Senate Banking Committee in the first half of the week. Powell’s comments at March’s testimony emphasised that the path back to the Fed’s 2.0% inflation target will likely be bumpy and that the Fed may begin dialling back on policy this year but stressed the need for confidence in the disinflation process. Markets expect the Fed Chair to repeat similar points in the latest FOMC minutes, underlining the need for confidence before reducing the policy target range and highlighting signs of slowing inflation.

Thursday’s release of the June CPI data will follow last week’s softer PCE inflation numbers on both the headline and core front. Headline CPI inflation is expected to slow to +3.1% year on year, down from +3.3% in May, and report a +0.1% gain month on month, up from May’s 0.0% print. Core inflation, which removes energy and food components, is anticipated to remain unchanged year on year and month on month at +3.4% and +0.2%, respectively. The inflation release will be particularly important amid increased odds of a September rate cut and recent comments from Fed Chair Powell at the ECB Forum on central banking in Portugal: ‘We’ve made quite a bit of progress in bringing inflation back down to our target, while the labour market has remained strong and growth has continued’. Therefore, should US CPI inflation data print a broad miss this week, this could see a dovish repricing in rate expectations, weigh on US Treasury yields and the dollar, and prompt a bid in equities.

Reserve Bank of New Zealand – No change expected

The Reserve Bank of New Zealand (RBNZ) will take the stage on Wednesday and provide another policy update. As of writing, markets are nearly fully pricing in a hold at this week’s meeting, a move that would see the Official Cash Rate (OCR) left at 5.5% for an eighth consecutive meeting.

The hawkish tone the central bank adopted at the May meeting surprised the market, indicating that the OCR would need to remain restrictive for longer than anticipated in the February statement to ensure inflation returns to the Committee’s 2.0% mid-point inflation target. RBNZ Governor Adrian Orr also communicated that the central bank has ‘limited room for upside surprises in inflation’ and that there was a ‘real consideration’ regarding increasing the OCR at the meeting.

Despite record migration levels for the country, New Zealand’s economy is combating paltry economic growth – the country recently exited a technical recession after GDP growth rose +0.2% in Q1 this year after two back-to-back quarters of negative GDP growth were seen in the second half of 2023 – as well as unemployment increasing to 4.3% in Q1 this year (its highest reading since early 2021). Inflationary pressures, however, remain front and centre. According to the latest release from Statistics New Zealand, consumer price pressures are easing but not as swiftly as the central bank had hoped. Annual inflation slowed to +4.0% in March, down from +4.7% in December, though higher than the +3.8% RBNZ forecast.

Heading into the event, analysts are not anticipating much change to the OCR or forward guidance due to the lack of economic data since the May meeting. The only data print of note was GDP highlighted above. This meeting also does not include updated economic forecasts (these will be released in the August meeting). Therefore, the expectation is for the central bank to maintain its hawkish stance, which could underpin the New Zealand dollar (NZD).

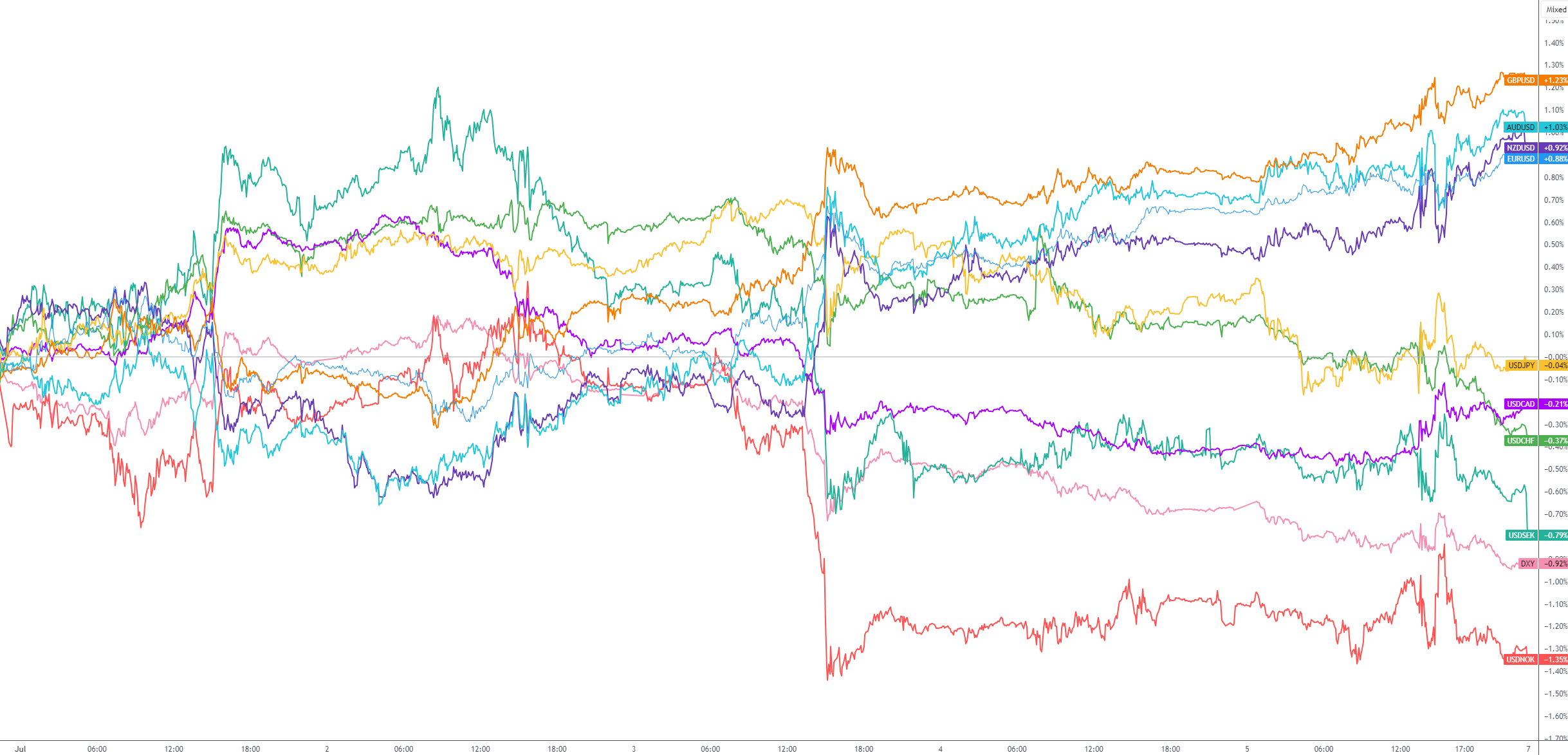

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,