Week ahead – US NFP to test the markets, Eurozone CPI data also in focus

-

King Dollar flexes its muscles ahead of Friday’s NFP.

-

Eurozone flash CPI numbers awaited as euro bleeds.

-

Canada’s jobs data to impact bets of a January BoC cut.

-

Australia’s CPI and Japan’s wages also on tap.

Will the US data add more fuel to the Dollar’s engines?

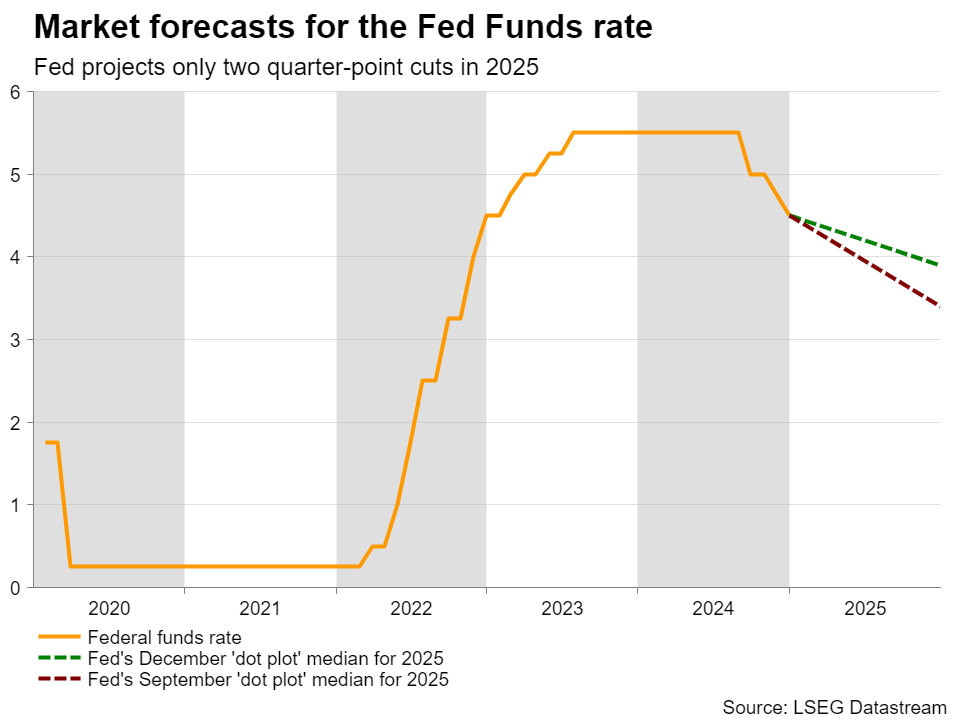

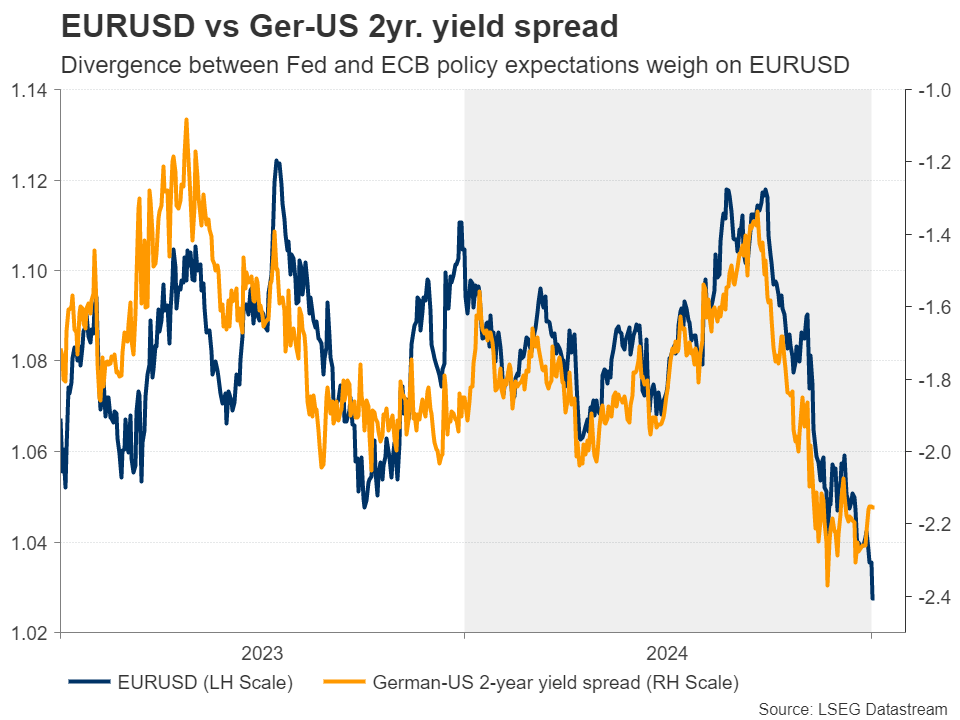

The US dollar opened the new year with a negative gap but was quick to resume its prevailing uptrend as the fundamental landscape has not changed. A hawkish Fed, scaling back its rate cut projections to signal only two quarter-point reductions by December, resulted in widening yield differentials between the US and other major economies, whose central banks began leaning towards a more dovish stance towards the end of 2024.

What led to this was the election of Donald Trump as US president, which raised concerns that his tariff and tax cut policies will refuel inflation. The better-than-expected economic data, and the stickiness in inflation even before Trump’s policies are enacted, have been also corroborating the idea that the Fed should not be in a rush to lower interest rates further.

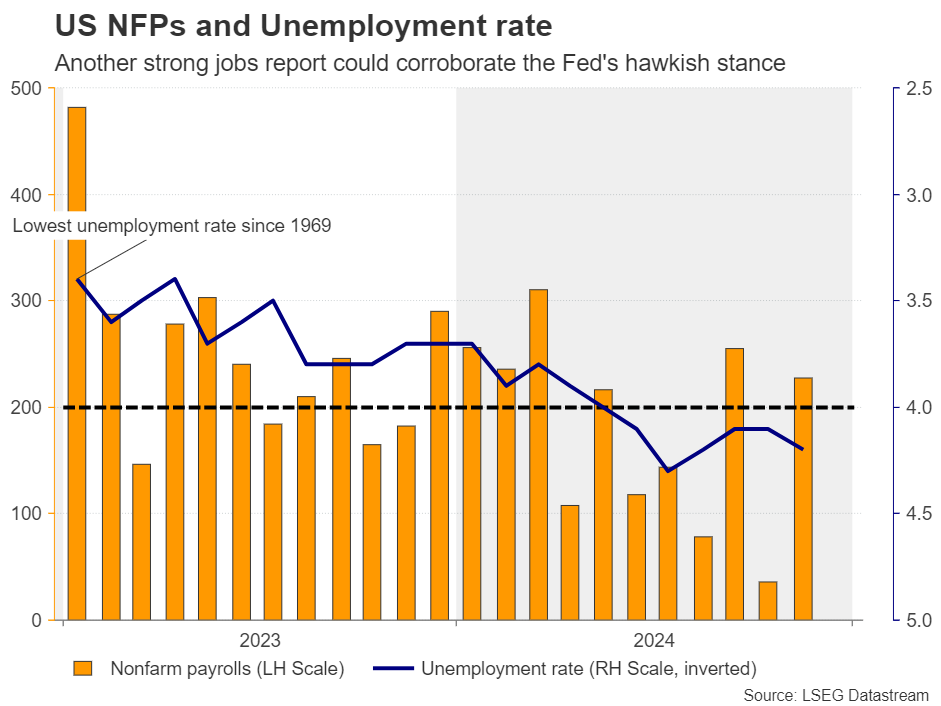

With that in mind, investors will be eagerly awaiting next week’s events, among which is the official employment report for December. The November report revealed that employment rebounded strongly, with the economy adding 227k jobs following October’s 12k, which was the weakest jobs growth since December 2020.

Ergo, another month corroborating the notion that the weakness seen in October was only temporary due to labor strikes and hurricanes, may prompt some investors to think that even two quarter-point reductions may be too many in 2025, and thereby allow the dollar to continue marching north against every other major currency.

The riddle here is whether the stock market will extend its retreat on expectation of even fewer rate cuts, or whether it will gain on signs of robust economic performance. Taking into account that stock enthusiasts are longer-term investors than forex traders, as long as no rate hikes are on the horizon, they may be willing to celebrate another stellar performance of the labor market.

Wednesday’s ADP private-sector employment data and Thursday’s initial jobless claims may provide an earlier glimpse on how the US labor market has been faring, while Monday’s ISM non-manufacturing PMI for December could offer more information about the overall performance of the US economy given that non-manufacturing activity accounts for more than 80% of GDP.

The minutes of the December Fed decision are also due to be released on Wednesday but given that this was one of the meetings that was accompanied by updated economic projections, the minutes may attract less attention than usual, as the new dot plot already provided an idea of policymakers’ thinking about the future course of interest rates.

Will Eurozone’s CPI prints take Euro/Dollar closer to parity?

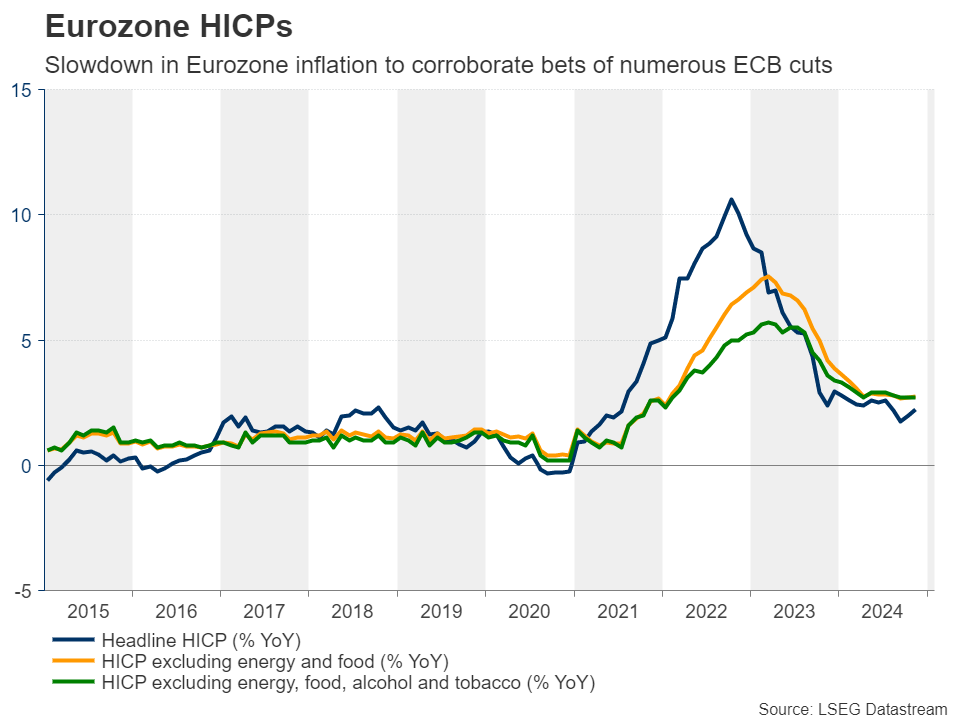

In the Eurozone, the spotlight is likely to fall on the preliminary CPI data for December, coming out on Tuesday. At its December meeting, the ECB trimmed interest rates by 25bps and signaled that more cuts are on the way by removing a reference to keeping interest rates “sufficiently restrictive”.

The following week, President Lagarde reiterated the view that should incoming data continue to confirm their baseline view, more rate cuts will be delivered, adding that she hopes “the picture is a little clearer for those who were wondering what this change in language meant last week.”

Even Isabel Schnabel, the Bank’s most influential hawk, said “Considering the risks and uncertainties we are still facing, lowering policy rates gradually towards a neutral level is the most appropriate course of action.”

President Lagarde noted that ECB research is estimating the neutral rate within a range between 1.75% and 2.5%, which means that more reductions are needed before speculation of whether the Bank has reached neutral heats up.

With all that in mind, market participants are now anticipating another 110bps worth of rate reductions by December, which highlights a clear divergence in policy expectations between the ECB and the Fed. Therefore, should the CPI data reveal some further cooling in inflation, traders may feel more confident about numerus rate cuts by the ECB this year, thereby pushing the euro even lower.

The German preliminary CPI numbers will be released on Monday. Thus, volatility in the euro may begin early as the inflation trajectory in the Eurozone’s largest economy could impact speculation about whether Tuesday’s numbers will come in above or below analysts’ estimates.

Overall, the outlook of euro/dollar remains overly bearish, not only due to the divergence in monetary policy expectations between the Fed and the ECB, but also due to the political crises in France and Germany as well as the uncertainty surrounding Trump’s tariff policies on European goods.

Canada jobs report, Australia’s CPI and Japan’s wages also on tap

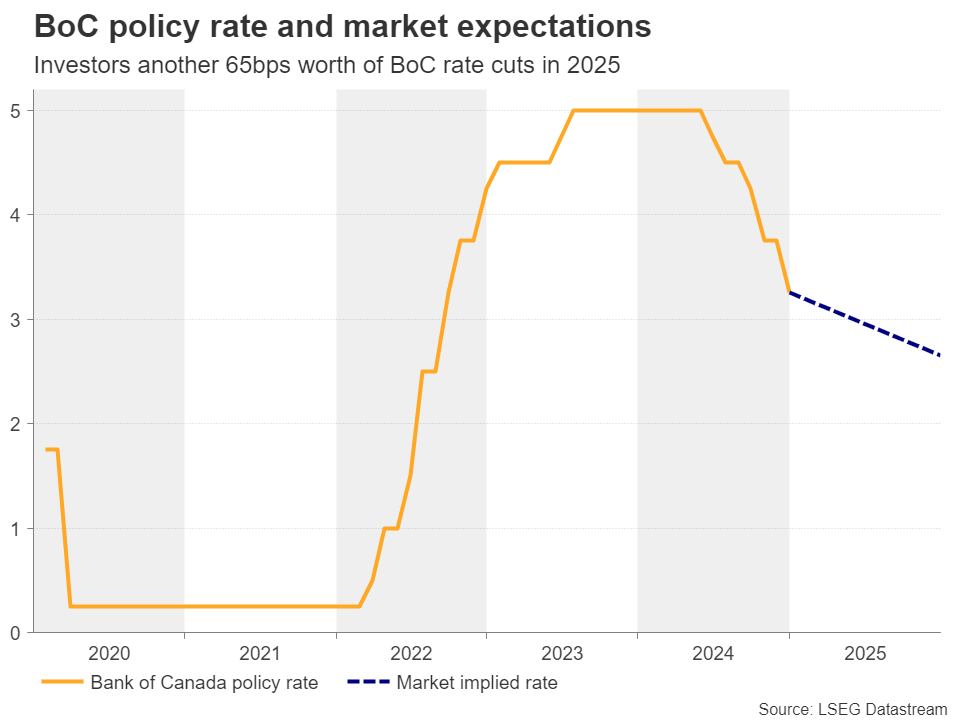

At the same time the US employment report is coming out, Canada will release its own jobs data. At its last decision for 2024, the BoC lowered interest rates by another 50bps, the second double cut in a row, but Governor Macklem refrained from signaling a predetermined path of additional cuts and instead he adopted a more data-dependent approach.

That said, the lower-than-expected CPI data for November and the weaker-than-forecast retail sales for October prompted investors to factor in a 75% chance of another 25bps reduction at the January 29 meeting and a total of 65bps worth of cuts by the end of 2025. In November, the unemployment rate jumped to 6.8% from 6.5% and thus, further cooling of the Canadian labor market could increase the need for lower borrowing costs and thereby deepen the loonie’s wounds.

Elsewhere, Australia’s monthly CPI for November will be released on Wednesday, while on Thursday, Japan publishes wage data for November. Following the emphasis BoJ Governor Ueda placed on the spring wage negotiations at the press conference following the latest BoJ decision, next week’s data have the potential to impact market bets about whether the Bank will hike in January or not. Currently, the probabilities of another 25bps reduction or remaining on hold are those of a coin toss.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.