Week ahead – US NFP and Eurozone CPI awaited as tariff war heats up, RBA meets [Video]

-

Trump’s reciprocal tariffs could spur more chaos.

-

US jobs report might show DOGE impact on labour market.

-

Eurozone inflation will be vital for ECB bets as April cut uncertain.

-

RBA to likely hold rates; Canadian jobs, BoJ Tankan survey also on tap.

![Week ahead – US NFP and Eurozone CPI awaited as tariff war heats up, RBA meets [Video]](https://editorial.fxsstatic.com/images/i/nfp-workers-1_XtraLarge.png)

Markets brace for reciprocal tariffs

There’s a sense of both optimism and fear as we approach the April 2 deadline of when the Trump administration will detail the much talked-about reciprocal tariffs. All indications are that the White House will primarily target the countries with which the US has the biggest trade imbalances, thought to cover 15% of America’s trading partners. Hence, they’ve been dubbed as the ‘Dirty 15’ and include China, the EU, Mexico and South Korea among others.

Negotiations are already underway with several countries to find a middle ground so if Trump shows leniency, a relief rally could ensue. However, if the announcement contains very few exemptions and markets are left disappointed, shares on Wall Street could resume their selloff.

It’s also possible that Trump might unveil further sectoral tariffs, such as for pharmaceuticals. Risk appetite would struggle to get far in such a scenario.

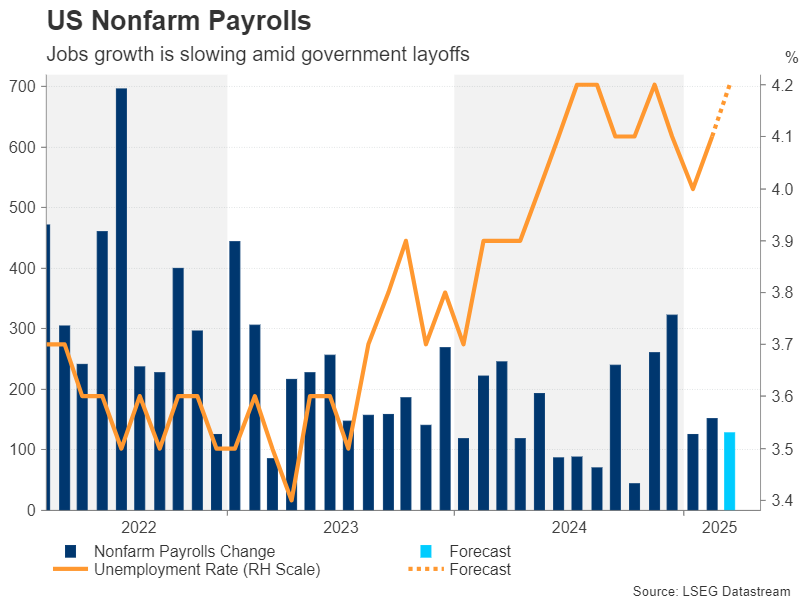

NFP slowdown could fuel recession fears

Worries about the US economy stumbling amid the Trump administration’s radical policies have so far proved unfounded, but next week’s nonfarm payrolls report could change that. The Department of Government Efficiency (DOGE) has been busy laying off federal workers since its inception after Donald Trump’s election victory.

Those job cuts will likely start to come through in the March payroll figures. At the same time, many businesses have turned more cautious with their hiring plans, especially in the manufacturing sector, as President Trump’s erratic decisions on tariffs are generating a lot of uncertainty about the economic outlook.

Fed Chair Powell insists that the US labour market remains “in balance”. Nevertheless, the risks are clearly tilted to the downside and so there is some anxiety about Friday’s jobs data. After a gain of 151k in February, nonfarm payrolls are expected to have increased by 128k in March.

The change in government and private payrolls will be watched very closely to gauge the scale of potential DOGE layoffs and to what extent these will be replenished by the private sector.

The unemployment rate is projected to tick up slightly to 4.2%, while average hourly earnings are forecast to have risen by 0.3% m/m.

Any cooldown in the labor market that’s a lot greater than what’s anticipated could bolster Fed rate cut expectations. The Fed has yet to budge on its wait-and-see stance despite the few cracks that have started to appear in the economy.

Will the data support the Dollar’s rebound?

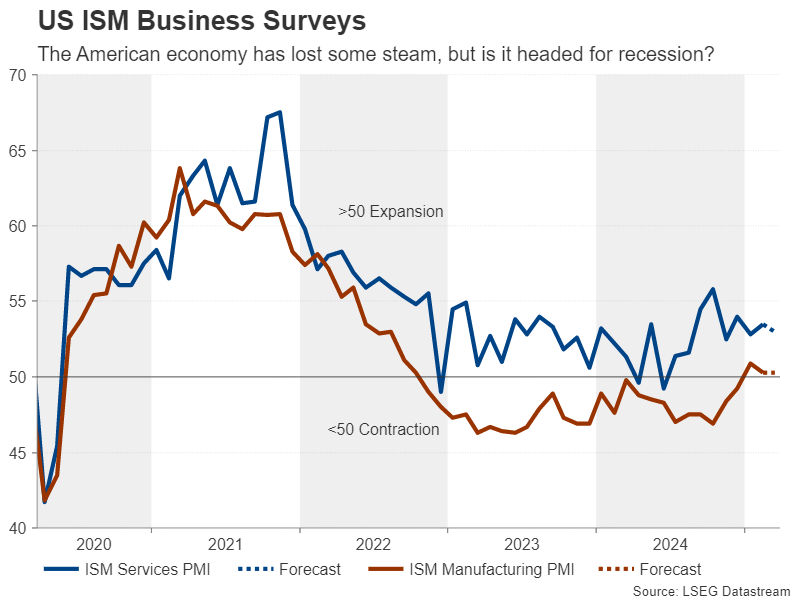

However, the market reaction will likely be influenced by the tone set by the ISM PMIs that will be published in the preceding days. The ISM manufacturing PMI is out on Tuesday and is expected to stay unchanged at 50.3. The ISM services PMI will follow on Thursday and that’s forecast to dip slightly from 53.5 to 53.0.

Other releases include the Chicago PMI on Monday, the JOLTS job openings on Tuesday, the ADP employment report and factory orders on Wednesday, and Challenger Layoffs on Thursday.

The US dollar has been in recovery mode over the past couple of weeks but should the incoming data point to a weakening economic backdrop, it’s likely to face some renewed selling pressure, particularly if investors price in a strong probability of a third rate cut this year.

A major risk for the markets is if any poor numbers are accompanied by a spike in the ISM survey’s price indices, which would indicate a stagflationary environment. It would be tough for Wall Street to find much support from aggressive rate cut bets under such conditions.

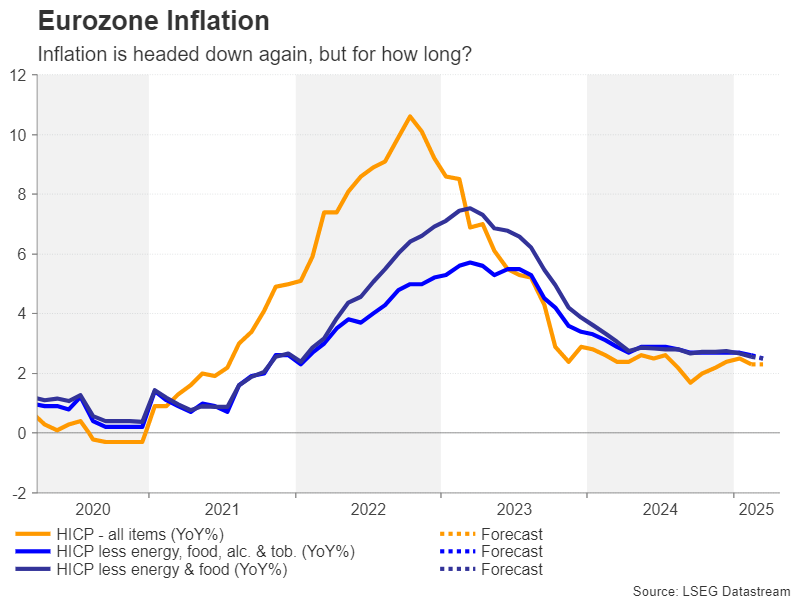

Eurozone CPI eyed as tariffs boost ECB cut bets

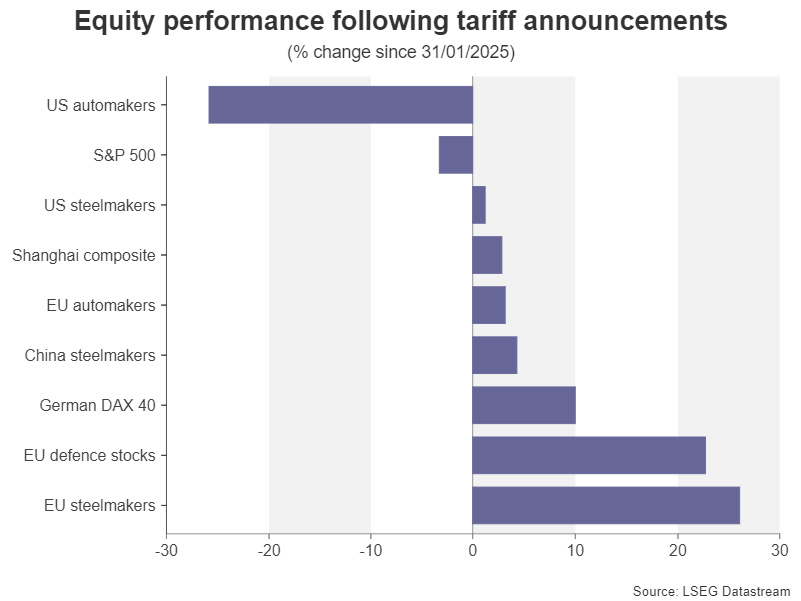

Policymakers from the European Central Bank have hinted at the possibility of a pause in rate cuts at the April meeting, but the decision looks set to be a close one as the case for caution has weakened after Trump’s decision to impose 25% tariffs on all auto imports into the United States as of April 2.

The latest levies, which include imports of all automobile parts, are likely to hit European economies hard as the continent is a major exporter of cars and related parts to the US. Investors seem to think that the ECB will have little choice but to lower rates again when it meets on April 17 to cushion the Eurozone economy from Trump’s trade tirade and are pricing in about a 90% probability of a 25-basis-point reduction.

If Tuesday’s flash CPI estimates for March show another decline in the inflation readings, the euro will be in danger of deepening its recent pullback against the US dollar. The Eurozone’s headline CPI rate fell to 2.3% y/y in February, ending four months of increases. Core measures have also moderated. But if there’s a reversal of this trend, rate cut expectations could be pared back, lifting the euro.

The account of the ECB’s March meeting might offer further clues about the next gathering when it’s published on Thursday.

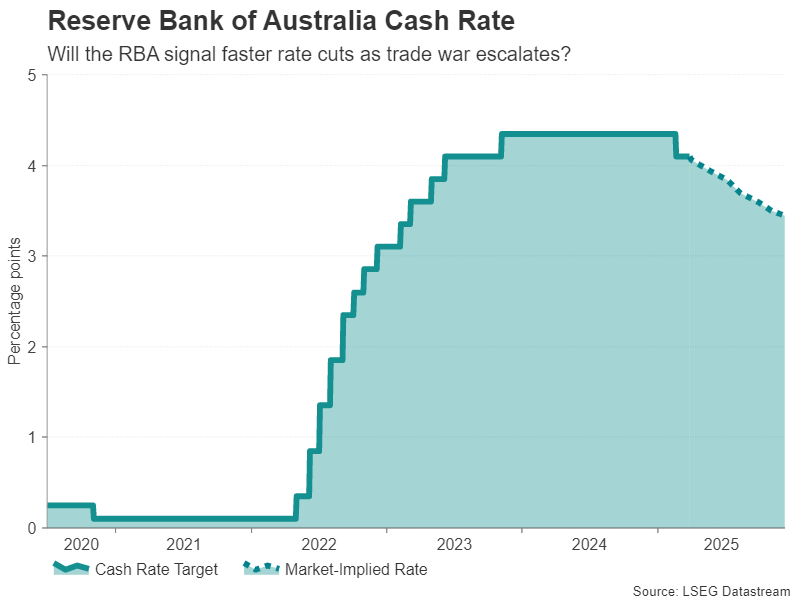

RBA to hold rates amid trade frictions

A central bank that’s almost certain to keep interest rates unchanged at its next meeting is the Reserve Bank of Australia. Having been late to the game, the RBA trimmed its cash rate in its previous decision in February but is not expected to cut again until July. However, the escalating trade war, which China is at the centre of, makes it more likely that the RBA will cut rates sooner rather than later.

Moreover, with inflation in Australia easing slightly in February and employment unexpectedly falling, policymakers may not sound quite as hawkish as they did in February.

Should the RBA open the door to a rate cut at its May meeting, the Australian dollar could reverse lower, although it’s so far been able to hold above its short-term uptrend line despite the heightened trade frictions.

PMI numbers out of China will also be important for the aussie and may offer some support if they signal an improvement in manufacturing activity as forecast. The government’s own manufacturing PMI is due on Monday, while the equivalent PMI from S&P Global/Caixin is out on Tuesday.

Tariffs complicate BoC’s rate cut path

The Canadian dollar has also been on a somewhat steadier footing lately, even though Canada has come under Trump’s direct firing line. The Bank of Canada has not been shy about expressing its concerns about the negative impact of the trade war on the economy. However, although the BoC cut rates by a further 25bps earlier this month, citing tariff risks, Governor Tiff Macklem acknowledged that the risks to inflation have gone up too.

This potentially limits the scope of additional easing and investors see just two more 25-bps rate cuts for the rest of the year. Those odds could increase, however, if the Canadian economy were to take a sudden turn for the worse.

Traders will therefore be keeping a close eye on Friday’s employment data for any signs about a slowing labour market.

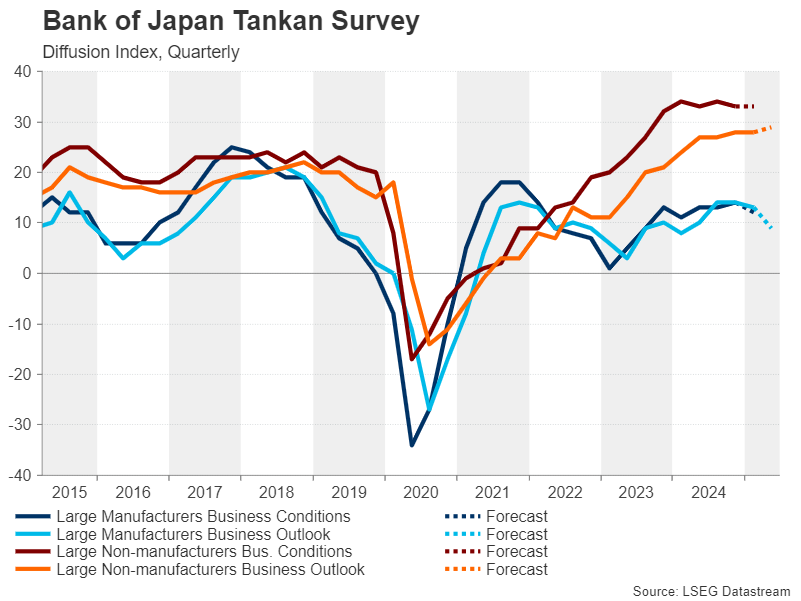

Yen slides as tariffs throw BoJ hikes into doubt

The Japanese yen hasn’t been able to garner much safe-haven bids during the latest wave of tariff headlines. Investors think that Trump’s sectoral and reciprocal tariffs will hurt Japanese growth, making it more difficult for the Bank of Japan to hike interest rates again later this year.

The Bank’s own Tankan business survey that’s conducted quarterly should shed some light on Tuesday as to whether Japanese businesses are becoming less optimistic about the outlook and reducing their capital expenditure plans on the back of the growing trade turmoil.

Preliminary industrial output figures for February are also due on Tuesday, while household spending data will be released on Friday.

The yen could halt its recent slide against its major peers if the data calms jitters about significant damage to the Japanese economy from Trump’s protectionist policies.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl