Week ahead: US labour data and the BoC rate announcement in focus

Highlights:

- US employment situation report

- Bank of Canada (BoC) rate announcement

US jobs data

With US Federal Reserve (Fed) Chair Jerome Powell’s recent speech at the Jackson Hole Symposium confirming that it is time to begin easing policy as well as underlining the importance of the jobs market, this week’s jobs data may help determine how the Fed approaches its easing cycle. Markets are pricing in -33 basis points of easing for September’s meeting. To put that into perspective, there is a 70% probability of a 25 basis point rate cut in September over a 30% chance of a 50 basis point cut. Additionally, investors still forecast -100 basis points of cuts for the entire year (four rate cuts).

Friday’s US employment situation report is key at 12:30 pm GMT. This follows the broad downside surprises across key measures for July (2024), triggering declines in US Treasury yields and the US dollar (USD). According to the Reuters poll, the median estimate for the August non-farm payrolls report indicates 163,000 jobs were added to the US economy, up from 114,000 in July. The unemployment rate for August is expected to ease to +4.2% from +4.3% in July, while average hourly earnings wage growth is estimated to modestly increase in August on both month-on-month and year-on-year measures to +0.3% (from +0.2%) and +3.7% (from +3.6%).

In the event of further softness in data this week, this could swing the pendulum more in favour of a bulky 50 basis point rate cut. This may also further weigh on US Treasury yields and the USD. However, the issue with US equity markets is that bad news may not necessarily be good news based on recession fears, meaning a soft number could send stocks lower.

Before the headline employment numbers, US JOLTs Job Openings will be released on Wednesday, and the ADP non-farm employment change and weekly unemployment claims will be released on Thursday. We also get the Institute for Supply Management (ISM) data for August for manufacturing (Tuesday) and services (Thursday).

BoC: Third rate cut?

The BoC claims a portion of the limelight on Wednesday this week, scheduled to deliver an update at 1:45 pm GMT. As of writing, -29 basis points of easing is priced in for this announcement, meaning investors are anticipating another 25 basis point rate cut, bringing the Overnight Policy Rate to 4.25% and marking a third successive rate cut for the central bank. For the year, investors expect another two rate cuts following this, with a 25 basis point reduction at October and November’s meetings. And the economic landscape in Canada appears to justify rate cuts.

The year-on-year CPI inflation (Consumer Price Index) eased to its lowest levels since early 2021 at +2.5% in July (2024), down from +2.7% in June, remaining within the BoC’s inflation band of 1-3%. The BoC’s preferred measures of inflation, ‘CPI Median’ and ‘CPI Trim’, also pulled back to +2.4% and +2.7%, respectively, bringing the average of the two measures to +2.55%, down from +2.75%. At the July meeting, BoC Governor Tiff Macklem communicated that if further progress on disinflation is observed, it is ‘reasonable to expect further cuts in the policy interest rate’.

Regarding the labour market, unemployment remained at 6.4% for a second consecutive month in July (2024), unchanged from early 2022 peaks. Employment growth also fell by -2,800 in July, following a marginal fall of -1,400 in June. However, Statistics Canada noted: ‘Full-time positions saw an increase of 62K workers, while part-time jobs dropped by 64K’.

Statistics Canada released Q2 2024 Gross Domestic Product (GDP) on Friday and revealed economic activity grew more than expected, though it relied heavily on government spending (up +6.7%). On an annualised basis, GDP rose +2.1%, comfortably surpassing economists’ estimates and the BoC’s forecast of +1.5%. Albeit an impressive start to the first half of the year, under the hood shows it’s not all it’s cracked up to be. GDP per capita declined -0.1% (marking a fifth consecutive quarterly decline), and month-on-month GDP was flat in June. According to the flash estimate, July is also poised for another flat reading, lending to a weak Q3.

With a rate cut baked in, this is unlikely to generate much ‘surprise’; therefore, we can expect a limited market response. Traders will focus on the language from the rate statement and the press conference for clues of further easing, potentially weighing on the Canadian dollar (CAD) and underpinning the USD/CAD currency pair, which ended August lower by -2.3%.

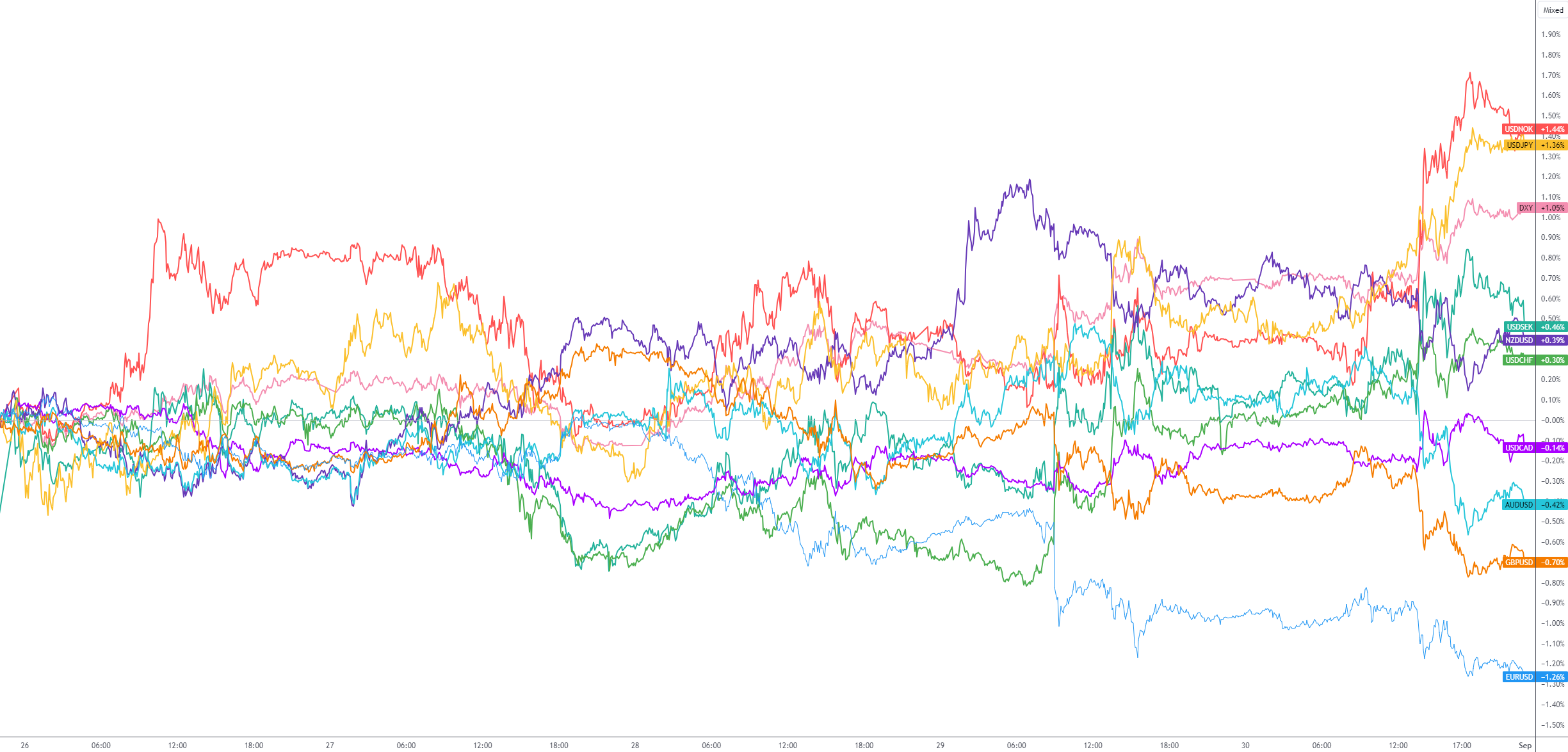

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,