Week Ahead – US inflation report, BoC and RBNZ meetings eyed

Another exciting week lies ahead for FX markets, before trading conditions start to wind down for the summer. The spotlight will fall on the latest US inflation report, which could help the dollar break out of its recent stalemate. Central bank meetings in New Zealand and Canada will also be closely watched, especially the Bank of Canada rate decision, which is currently priced as a coin toss.

Dollar in limbo, awaits inflation test

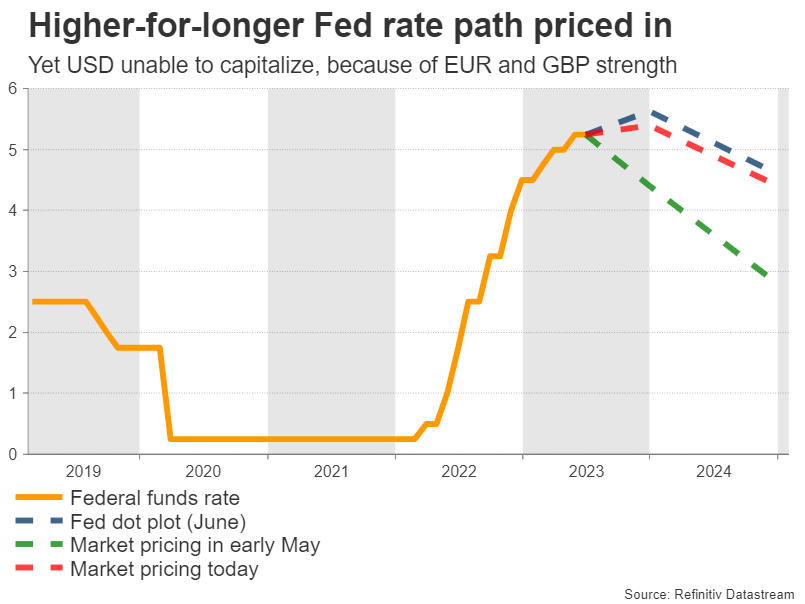

The second quarter of this year was tough for the dollar, even though the US economy seems to be humming along. Economic growth is running near 2%, the housing market has enjoyed a sensational comeback, and the labor market seems to be in good shape.

Investors responded by pricing in a higher-for-longer path for interest rates, pushing out the projected timing of any rate cuts into the second half of 2024. In turn, that sparked some pretty impressive moves in the bond market, with the 2-year yield in particular racing higher.

Yet the dollar was unable to capitalize, drifting sideways instead. This stagnation probably reflects the strength in other major currencies, specifically the euro and sterling, as their central banks telegraphed a series of rate increases ahead.

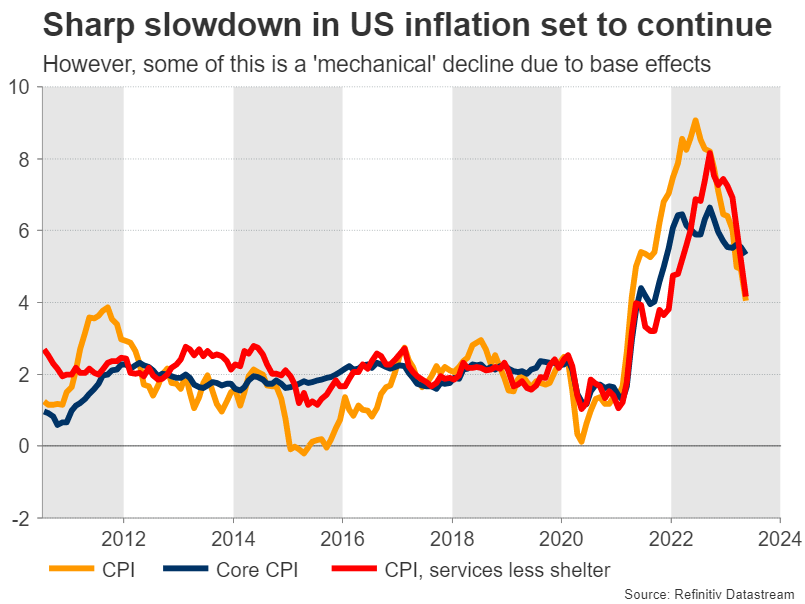

The upcoming US inflation report on Wednesday can help break this FX stalemate. In yearly terms, forecasts point to a sharp slowdown in inflation. The headline CPI rate is set to decline to 3.6% from 4% previously, while the core rate is seen dropping to 5% from 5.3% in May.

Much of this improvement is due to base effects, as some extremely hot CPI prints from June 2022 will now be dropping out of the 12-month calculation. Inflation is definitely coming down, something also confirmed by business surveys, but not at such an astonishing pace. Data on producer prices will also be released on Thursday.

As for the dollar, the outlook for the second half of the year seems brighter. It’s a story of relative economic performance, as the US economy is far superior to the Eurozone’s or China’s at this stage. And this gap could widen further as the year unfolds, amid warnings from business surveys that both Europe and China are losing steam, in contrast to resilient US surveys.

Currency markets have been trading almost entirely on rate differentials lately, helping to explain the strength in the euro as the ECB maintained a hawkish stance. However, with central banks approaching the end of their tightening cycles, the next trading theme might be growth differentials, which clearly favor the US.

A potential shift in global risk appetite could also help the dollar to recover. If the euphoria in stock markets calms down and there’s a correction in risk assets later this year, the world’s reserve currency could finally attract some safe haven flows.

Traders divided on Canadian rate hike

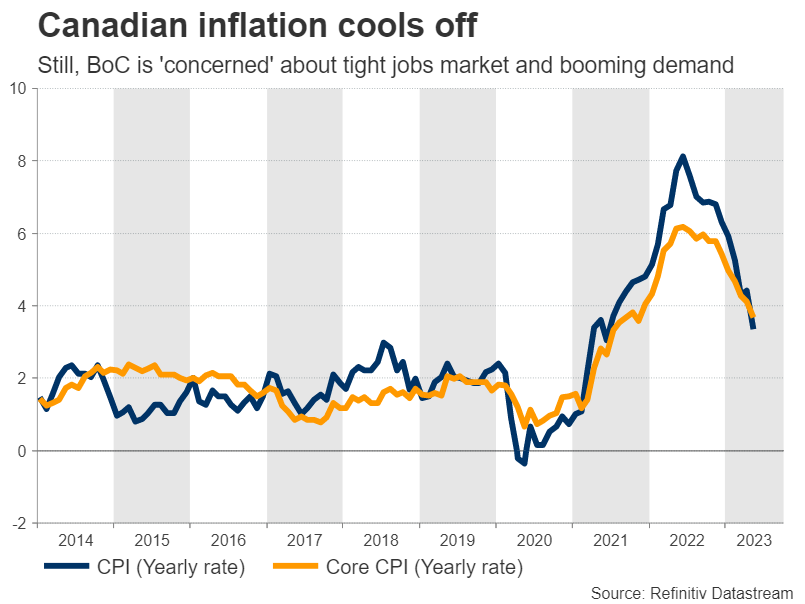

Crossing into neighboring Canada, the central bank will wrap up its meeting on Wednesday, with market participants assigning almost equal chances for a 25bps rate increase or no action at all.

Arguing for the Bank of Canada to do nothing is the steady decline in inflation this year, which is the most important element for any central bank. Additionally, the nation’s manufacturing sector is struggling amid a global downturn and oil prices have declined substantially.

However, the labor market is still very tight, consumer spending has been resilient, and housing costs have not really cooled despite the sharp increase in interest rates, as net population growth has been exceptionally strong.

Hence, it’s a true dilemma for the central bank - inflation is cooling but several factors suggest it could heat up again moving forward.

In the FX market, the risks seem tilted towards a negative reaction in the Canadian dollar. With inflation coming down, it would make more sense for the BoC to take the sidelines for now. Even if the BoC raises rates and the loonie spikes higher, there’s still a risk the initial excitement fades quickly if policymakers signal this is probably their final move.

RBNZ - A quiet meeting

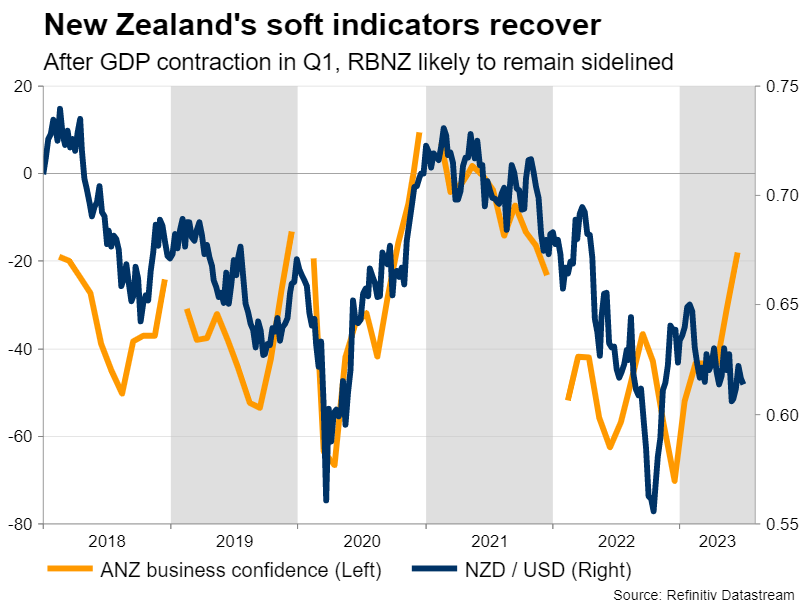

It’s going to be a more straight-forward affair when the Reserve Bank of New Zealand decides early on Wednesday. The RBNZ made it clear at its latest meeting that it will adopt a wait-and-see stance and examine incoming data for some time, before making its next move.

Economic data since then has been mixed, with GDP growth turning slightly negative in Q1 but survey-based indicators pointing to a recovery in the second quarter. Overall though, nothing shocking enough to nudge the RBNZ out of its neutral stance.

Therefore, the reaction in the New Zealand dollar might be relatively minimal, leaving the currency mostly in the hands of global risk sentiment and any news out of China. Specifically, any stimulus announcements by Chinese authorities could be crucial, considering the close trading links between the two economies.

Speaking of China, the nation’s inflation stats for June will be released early on Monday. Producer prices - a proxy for factory demand - have been falling steadily in recent months as the manufacturing sector lost power and it will be interesting to see if this trend persists. The latest trade data will also be released on Thursday.

Last but not least, the UK will see the release of its employment numbers for May on Tuesday, ahead of monthly GDP data for the same month on Thursday.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service