Week ahead: US employment data due out next week

The week is drawing to a close, and as usual, we open the door to see what next week has in store for the markets. Starting on Monday, we note Japan’s preliminary industrial output rate for February, followed by China’s NBS manufacturing and non-manufacturing PMI figure and Germany’s preliminary HICP rates all for the month of March. On Tuesday we get Japan’s Tankan manufacturing and non-manufacturing index service figures both for Q1, Australia’s retail sales rate for February, China’s Caixin manufacturing PMI figure for March, the RBA’s interest rate decision, the UK’s Nationwide house prices rate for March, the Czech Republic’s revised GDP rate for Q4, the Eurozone’s preliminary HICP rate , Canada’s manufacturing PMI figure, the US’s ISM Manufacturing PMI figure all for March. On Wednesday, we get Australia’s building approvals rate for February, the US ADP national employment figure for March and the US factory orders rate for February. On Thursday, we get Australia’s trade balance figure for February, Switzerland’s and Turkey’s CPI rates for March, the US weekly initial jobless claims figure, Canada’s trade balance figure for March and the US ISM non-manufacturing PMI figure for March. Lastly, on Friday we get Germany’s industrial orders rate for February, Sweden’s and the Czech Republic’s preliminary CPI rates for March, the US and Canada’s employment data for March.

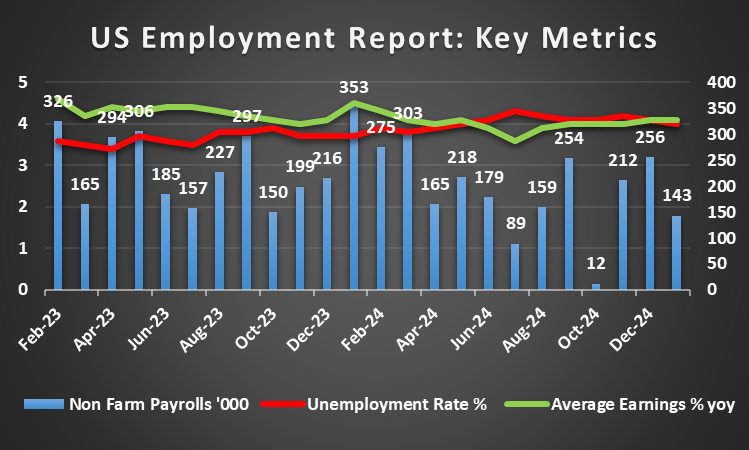

USD – It’s NFP week

On a macroeconomic level, the main event for dollar traders next week may be the release of the US Employment data for March. The current expectations by economists are for the non-farm payrolls figure to come in at 128k and for the unemployment rate to rise from 4.1% to 4.2% which would imply a loosening labour market. The implications of a loosening labour market, could increase pressure on the Fed to cut interest rates in their next meeting in order to ease the financial conditions surrounding the economy which could spur an increase in employment. In turn this may weigh on the dollar. However, should the data imply a resilient labour market it may have the opposite effect and could thus aid the greenback.

On a fundamental level, US President Trump’s “Liberation Day” for the US is set to occur on the 2nd of April, a date where retaliatory tariffs are set to be implemented. However, we may be seeing a sneak peek into what they may entail with the President announcing yesterday a 25% tariff on automobile imports. Furthermore, the President stated that “If the European Union works with Canada in order to do economic harm to the USA, large-scale Tariffs, far larger than currently planned, will be placed on them both”. The possibility of an escalation of trade wars may raise severe concerns over the resiliency of the US economy.

Analyst’s opinion (USD)

Under ‘normal’ circumstances, the anticipated easing of the labour market, could spur Fed policymakers to adopt a more ‘dovish’ tone, i.e implying possible rate cuts in the future as full employment is part of the Fed’s dual mandate. However, as we have continuously stressed, the President’s tariff ambitions raise serious concerns over the possibility of a resurgence of inflationary pressures in the economy and thus the Fed may require the tariff narrative to play out before attempting to gauge the true impact on the US economy.

GBP – UK CPI rates showcase easing inflationary pressures

On a macro-economic level, we note that the UK’s CPI rates for February were released on Wednesday. The inflation print showcased that on a headline and core level, inflationary pressures in the UK economy appear to be easing, with the headline rate coming in at 2.8% and the Core rate at 3.5% both of which are lower than the prior rates of 3.0% and 3.7% respectively. In turn, the implications of easing inflationary pressures may increase pressure on the BoE to cut rates in their next meeting, which in turn may weigh on the sterling.

On a political level, we note that UK Finance Chancellor Reeves announced the Spring Statement earlier this week. Per the FT “Reeves announced a budgetary repair job of £14bn after higher borrowing costs and slower growth pushed her £4bn into the red against her key fiscal rule” and that this gap will be addressed through welfare savings and a reduction in departmental spending.

Analyst’s opinion (GBP)

The lower-than-expected CPI print is welcome news for the Bank, yet the possibility of a trade war with the US could upend the BoE’s progress on combating inflation. Hence, should the UK fail to secure an ‘exemption’ from the tariff wrath of the US, it may weigh on the pound.

JPY – BoJ discussed hiking rates

On a macroeconomic level, of interest this week was Japan’s Tokyo CPI rates for March came in hotter than expected both on a headline and core level, implying an acceleration of inflationary pressures in the Japanese economy. In turn this may amplify calls for the BOJ to hike rates in the future, a scenario we go discuss on the paragraph below. Nevertheless, the acceleration of inflation may aid the JPY as the week comes to an end.

On a monetary level the highlight for Yen traders may have been the release of the BOJ’s last meeting minutes which were published on Tuesday. In the bank’s meeting minutes, “Some members noted that, looking at recent indicators of inflation expectations and other factors, it could be judged that the likelihood of underlying inflation increasing was rising”. The comments may imply that the bank could be prepared to raise interest rates, which in turn could aid the JPY, should the bank adopt a more hawkish rhetoric

However, President Trump’s decision to impose a 25% tariff on auto imports could derail the bank’s ambitions, as Japan’s export economy also relies on Japanese car exports to the US. As such, the recently announced tariffs could severely impact Japan’s economy and could outweigh recent financial releases.

Analyst’s opinion (JPY)

The BOJ’s intentions may have aided the Yen, yet the recent imposition of tariff’s on auto imports to the US may take the stage for the JPY. Should Japan fail to secure an exemption from the Trump administration could significantly raise concern over Japan’s economic outlook and with inflation on the rise, the BOJ may be placed in a difficult position.

EUR – EU-US relationship continues to deteriorate

The EU’s relationship with the US may continue to deteriorate following President Trump’s comments on Thursday. President Trump on a TruthSocial post stated that “If the European Union works with Canada in order to do economic harm to the USA, large scale Tariffs, far larger than currently planned, will be placed on them both in order to protect the best friend that each of those two countries has ever had!”. It appears that the sitting US President is threatening the union with a higher degree of tariff’s despite the EU’s trade chief meeting with Trump earlier on this week. Therefore, the possibility of a further escalation of the trade war with the US could impact the European Equities markets. Moreover, the recent 25% tariff on auto imports may significantly impact European car makers such as Volkswagen which are exposed in the American market.

On a macroeconomic level we note that France’s preliminary services PMI figure and Germany’s preliminary manufacturing PMI figure both for March came in better than expected. The better-than-expected PMI figures appear to provide a relatively optimistic outlook for the two main economies in the Zone. In turn the financial releases may have aided the EUR during the week. For next week EUR traders may be looking forward to the release of the Zone’s preliminary HICP rate for March on Tuesday and Germany’s preliminary HICP rate for March on Monday. Should the HICP rates showcase an acceleration of inflationary pressure, it may aid the EUR as it could increase pressure on the ECB to maintain a more restrictive monetary policy stance and vice versa.

Analyst’s opinion (EUR)

The EU needs to decide on their approach to the US Administration’s trade policies. Do they attempt to go tit-for-tat tariffs and thus embark on a trade war with a crucial trading partner, or do they attempt to walk the thin line of protectionism whilst maintaining a working relationship with President Trump. Moreover, the release of the preliminary HICP rate next week may be crucial for the ECB and their path going forward.

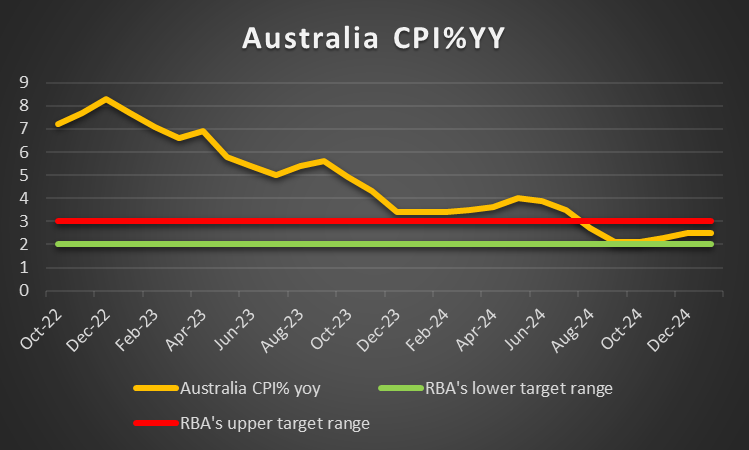

AUD – RBA decision next week

On a monetary level the RBA’s interest rate decision is set to occur next Tuesday. The current expectations by market participants are for the bank to remain on hold with AUD OIS currently implying an 88.1% probability for such a scenario to materialize. Thus our attention turns to the bank’s accompanying statement and as to whether or not the bank is prepared to cut rates in their May meeting which AUD OIS currently implies a 50.4% probability for a 25bp rate cut. Hence should the bank imply that they may cut rates in the near future it may weigh on the AUD. Whereas, should the bank imply that they may remain on hold, it could aid the Aussie.

On a macroeconomic level, Australia’s monthly CPI rate for February was released this Wednesday. The financial release showcased easing inflationary pressures in the Australian economy with the rate coming in at 2.4% versus the expected and prior rate of 2.5%. In turn this may have weighed on the Aussie. Yet the Judo Bank preliminary services and manufacturing PMI figures for March which were released on Monday came in higher than the prior figures, implying that from a manufacturing and services standpoint the Australian economy continues to expand, which in turn may have aided the Aussie.

Analyst’s opinion (AUD)

The RBA’s decision next week is set to be one of the highlights for Aussie traders. We would not be surprised to see the bank remaining on hold, yet with the heightened uncertainty over the impact of the US’s tariffs, the bank may opt for a more cautious tone i.e implying that the bank may need more time to assess the global economic outlook and the impact on the Australian economy, rather than committing to a rate cut in the future which in turn could aid the Aussie.

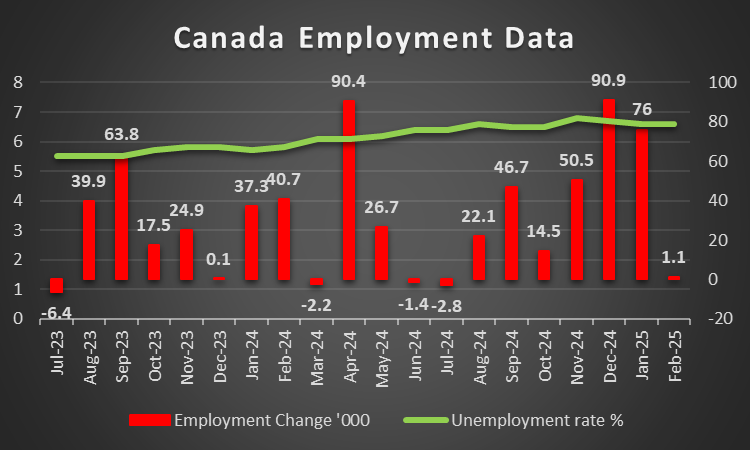

CAD – BoC may have remained on hold if not for Trump’s tariffs

On a monetary level, we note that the Bank of Canada’s summary of deliberations was released this week and tended to provide crucial insight into the bank’s inner deliberations. Specifically the comments that “They agreed that, in the absence of tariff threats and elevated uncertainty, the decision would probably have been to maintain the policy interest rate at 3%.” Implying that the bank may have remained on hold. The comments made by policymakers showcases the extent to which the bank is concerned about the impact on the economy as a result of the trade war with the US. Moreover,thourought the statement the bank’s concern over the implications of tarrifs on the economy is visible and thus may influence the bank’s future decisions.

On a macrolevel we highlight the releae of Canada’s Employment data next Friday. Should the employment data showcase a loosening labour market, such an increase in the unemployment rate and an employment change figure which would be lower than the prior figure then it may weigh on the Canadian dollar. Whereas, should the employment data showcase a resilient labour market it could potentially aid the CAD.

Analyst’s opinion (CAD)

We have seen a visible concern by the Bank of Canada as a result of the tariffs being imposed by the USA. In turn these tariffs may be upending the BoC’s progress on the fight against inflation as the Canadian economy is now under threat. Therefore, we would not be surprised to see heightened volatility in the CAD in the upcoming week, as the trade wars continue.

General comment

As a closing comment, we expect the USD to maintain the initiative in the FX market in the coming week given Trump’s “Liberation Day” on the 2nd of April and the release of the US Employment data on Friday. As for US Equities markets the mayhem continues we note the drop of the S&P500 and the NASDAQ for the week, yet the Dow Jones index appears to be ending the week slightly above it’s opening figure. As for gold’s price, the precious metal continues to soar to new all time highs.

Author

Phaedros Pantelides

IronFX

Mr Pantelides has graduated from the University of Reading with a degree in BSc Business Economics, where he discovered his passion for trading and analyzing global geopolitics.