Week ahead – US and UK inflation data to take center stage

-

US inflation numbers the next event to shake up Fed bets.

-

Pound traders lock gaze on CPIs after BoE’s hawkish hold.

-

Aussie awaits jobs report and Chinese data, Japan’s GDP also on tap.

Can US CPIs convince investors about one more Fed hike

After taking a strong hit last Friday due to the disappointing US employment report, the dollar staged a shy recovery this week as several Fed officials noted that the stellar performance of the US economy keeps the door open to further rate increases. Just on Thursday, Fed Chair Powell said that they “are not confident” that interest rates are high enough to signal the end of their fight against inflation.

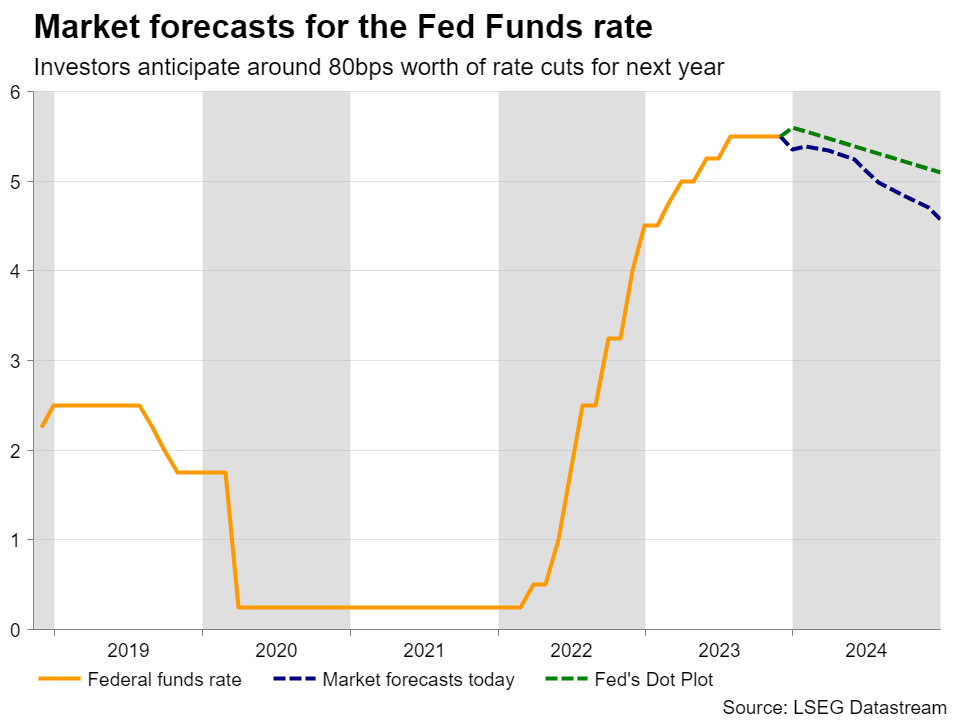

However, despite the recovery in the greenback, investors remained largely unconvinced that another hike may be on the table. According to Fed funds futures, they are assigning only a 20% probability for one last quarter-point increase by January, while pricing in around 80bps worth of rate cuts by the end of next year.

Maybe market participants expect inflation to pull back again, especially after the retreat in oil prices during October, and the economy to weaken going forward. Indeed, the Atlanta Fed GDPNow model estimates a 2.1% annualized growth rate for Q4, but in an environment of high interest rates and a stellar acceleration to 4.9% in Q3, this slowdown appears quite normal.

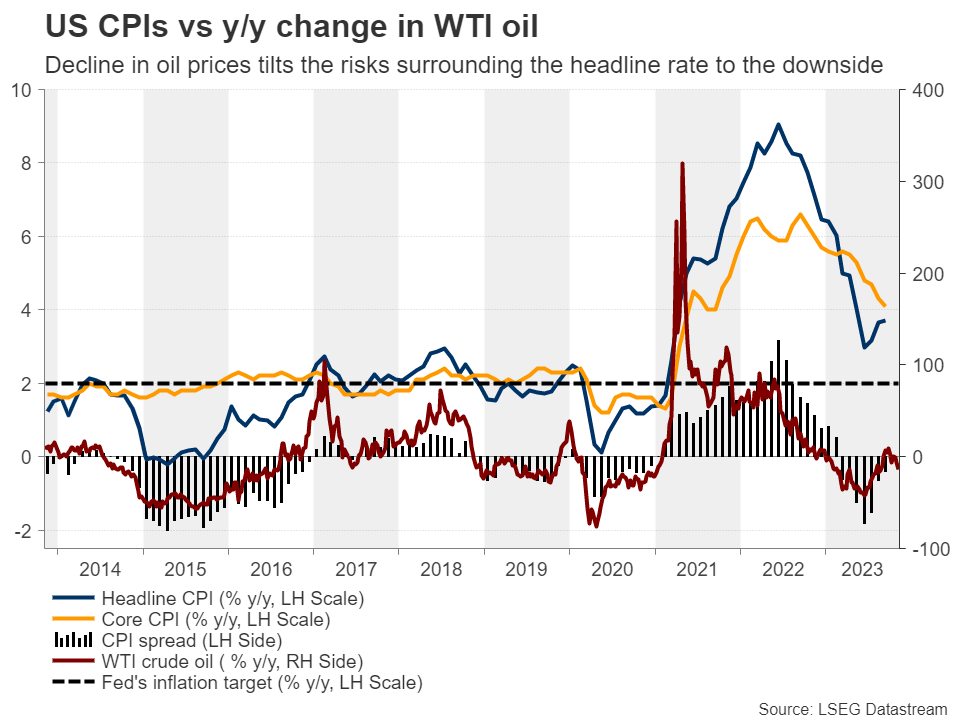

With all that in mind, next week, the spotlight is likely to turn to the US CPI data for October on Tuesday. The headline rate is expected to have pulled back to 3.3% y/y from 3.7% and the core one to have ticked down to 4.0% y/y from 4.1%. That said, considering that the PMIs for October suggested softer price pressures, the risks may be tilted to the downside, and with the y/y change in oil prices turning negative again, headline inflation could continue to soften going into year-end.

This could add credence to investors’ belief of no more rate hikes and several cuts for next year and perhaps hurt the dollar. However, as long as data relating to economic growth continues to suggest that the US economy is performing better than its major counterparts, any retreat in the greenback may just be a corrective phase. This could be confirmed if Wednesday’s retail sales and Thursday’s industrial production for October continue to point to a resilient US economy.

UK jobs and CPI data to affect the pound’s fate

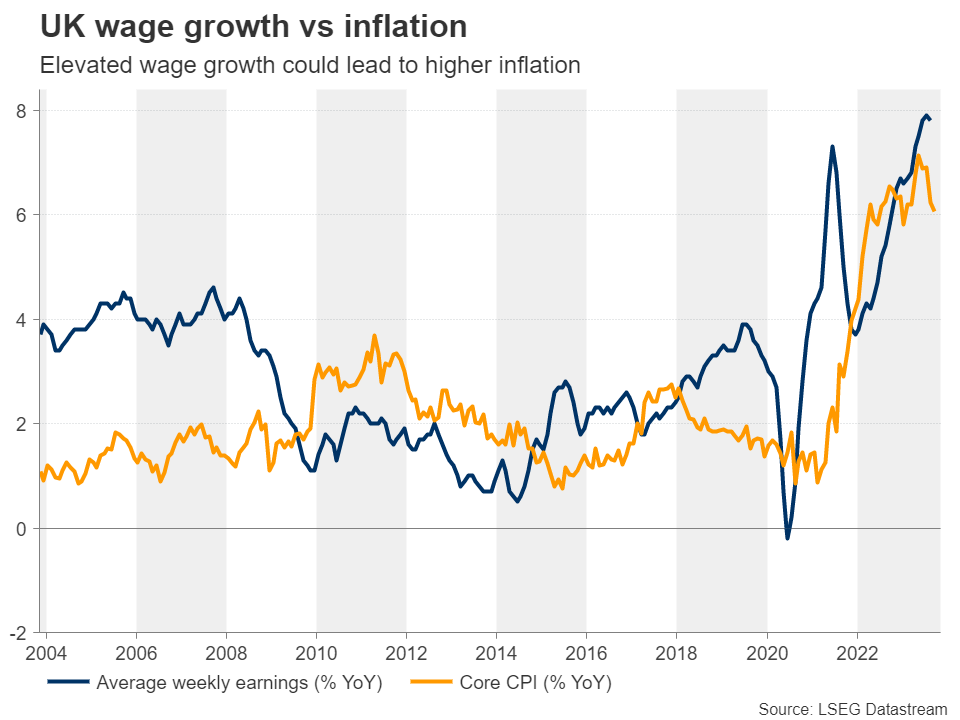

The UK also releases inflation data next week, on Wednesday. The headline CPI rate is anticipated to have slumped to 4.9% y/y from 6.7%, and the core one to have slid to 5.6% y/y from 6.1%. Nonetheless, according to the PMIs, prices charged by companies accelerated to a three-month high in October. Thus, in contrast to the US CPI data, there may be upside risks surrounding the UK numbers. Tuesday’s employment report for September could also be important as the average weekly earnings print may provide a glimpse of where inflation may be headed in upcoming months.

Last week, the BoE kept rates steady but noted that they remain willing to further raise them if there is evidence of more persistent inflationary pressures. Yet, investors see only a 15% probability of another hike. Ergo, data pointing to stickier-than-previously-expected inflation could boost that number, but even if they don’t, they may prompt investors to scale back some basis points worth of rate cuts anticipated for next year; not because of a brighter economic outlook but on fears that cutting massively to support the economy may result in inflation getting out of control, which could in turn lead to deeper economic wounds down the road. This, combined with cooler US inflation, could help Cable return above the key barrier of 1.2310 and perhaps emerge above its 200-day moving average. The nation’s retail sales for October are also coming out on Friday.

Aussie sets for volatility, Japan’s GDP to reveal contraction

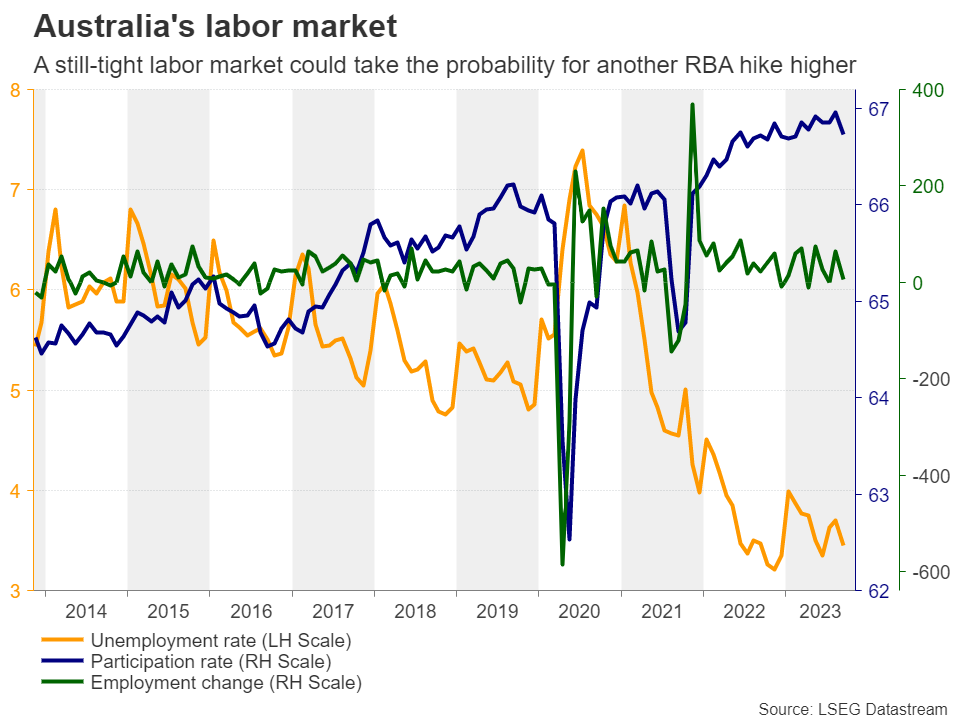

The aussie has been under pressure this week following the RBA’s dovish hike, as well as data and developments adding to concerns about China’s economic outlook. The probability of another hike at the December gathering is a coin toss, and thus traders may seek clarity in Australia’s employment numbers for October on Thursday. With the unemployment rate resting at historically low levels, labor conditions remain tight. The September data pointed to some cooling, but should next week’s numbers point to strength, the probability of a December hike may increase and the aussie could rebound.

However, any recovery could stay limited and short-lived if the Chinese numbers released the previous day add to the woes surrounding the world’s second largest economy. On Wednesday, investors will digest China’s industrial production, retail sales and fixed asset investment, all for October.

Japan’s preliminary GDP for Q3 is due to be released the same day. According to a Reuters poll, the Japanese economy likely shrank during the quarter, marking the first contraction in four quarters. Many analysts believe that the BoJ will phase out its ultra-loose policy next year, but a negative GDP figure could prove a challenge for the Bank’s plans and perhaps prompt traders to push the yen lower.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.