Week ahead: Updates from the RBA and SNB eyed; US PCE data also on the radar

The week that was:

Fed hammers home a 50bp cut

At the centre of things last week was the US Federal Reserve (Fed) rate announcement. In an 11-1 vote, the Fed initiated its easing cycle, reducing the target on the funds rate by an outsized 50 basis points (bps). Bringing the overnight rate to 4.75-5.00% marks the first rate cut since early 2020.

Recent decisions satisfied equity markets; the S&P 500 notched up a fresh record high of 5,733 last week, and the US Dollar Index (USD) refreshed year-to-date lows of 100.21 and clocked levels not seen since July 2023.

The key theme driving a 50bps cut was the shift from inflation to employment risks. The overarching message from the Fed was that employment data is key going forward, and a ‘soft landing’ remains the goal. As a result, upcoming data will determine how fast or slow the Fed proceeds. We have two more employment reports to digest before the next Fed rate decision in November. Markets are currently pricing in a 50/50 chance whether the Fed will opt for a 25 or 50bps cut (38bps priced in) at its next meeting, with any weakness in labour data potentially swinging the pendulum towards the latter.

The latest central bank forecasts project that the Fed funds rate will fall another 50bps by the year-end and another 100bps to 3.4% by the end of 2025, as well as an additional 50bps lower in 2026 to 2.9%, now the central bank’s long-run neutral rate. Fed members also forecast unemployment to rise to 4.4% by the end of this year. At the same time, PCE inflation (Personal Consumption Expenditures) is expected to be lower on both the headline and core measures.

Bank of England: Slow and steady does it

‘Slow and steady’ was the message from the Bank of England (BoE) last week. In an 8-1 vote, the BoE opted for a more cautious path than the Fed, keeping the Bank Rate on hold at 5.00%. The market widely viewed this as a ‘hawkish hold’, resulting in investors paring rate cut expectations and the pound (GBP) pencilling in fresh year-to-date highs of US$1.3340, levels not seen since February 2022.

BoE Governor Andrew Bailey commented that the central bank should be able to lower rates gradually but expressed inflation must stay low. As of writing, OIS traders (Overnight Index Swaps) are fully pricing in a 25bp cut for November’s meeting and just shy of 40bps of cuts until the year-end. November’s meeting will also provide fresh economic forecasts from the BoE.

The strength in the GBP/USD should not raise too many eyebrows. Not only did the central bank hold rates in restrictive territory and signal a slow and steady approach, but the hawkish vote split – with the only dissenter being external member Swati Dhingra, who, once again, opted to reduce policy by 25bps – added fuel to the fire.

While headline inflation is hovering north of the BoE’s inflation target of 2.0% (YoY headline inflation for August rose by 2.2%), core and services inflation remains a concern – the latter rose by 5.6% in the twelve months to August, up from July’s reading of 5.2%. The services sector makes up about 80% of economic output. With the jobs market still considered tight, the worry is that this may trigger higher wages. Therefore, policymakers need more evidence that inflation will continue to slow. On the other side of the fence, restrictive policy is clearly taking its toll on economic output. The Research Team recently noted: ‘The BoE now forecasts real Gross Domestic Product (GDP) to ease to 0.3% in Q3 24, a touch south of the 0.4% August forecast. While the economy grew 0.5% in the three months to July 2024, albeit softer than the market’s median estimate of 0.6% and lower than June’s reading of 0.6%, real GDP flatlined again in July, defying economists’ expectations of 0.2%’.

Overall, the GBP is likely to remain underpinned for the time being.

Bank of Japan: Cautious approach

The Bank of Japan (BoJ) claimed the headlines on Friday; all nine policymakers voted to hold the short-term Policy Rate unchanged at 0.25%, which was widely expected. This follows the central bank hiking its rate for a second time this year by 15bps in July, citing risks of a weak Japanese yen (JPY) increasing price pressures.

BoJ Governor Kazuo Ueda echoed a cautious vibe regarding global economic conditions, communicating that the central bank wants time to assess the economic outlook. Ueda added that while confidence in the domestic economy has improved, global risks are uncertain, particularly the US economy and the upcoming presidential election.

Regarding the next rate hike for the central bank, analysts largely favour January as a possible date for the next rate hike, giving them time to assess economic conditions. January’s meeting is also when they release their updated economic forecasts. However, should the JPY begin to depreciate again, this could trigger action from the BoJ sooner rather than later.

The week that is:

Monday will be about the S&P Global Manufacturing and Services PMIs (Purchasing Managers’ Indexes) for the eurozone, the UK and the US.

Tuesday welcomes an update from the Reserve Bank of Australia (RBA). The central bank is widely anticipated to hold things steady; investors assign a 7% probability that the RBA will cut rates this week over a 93% chance that they’ll leave things the way they are. Inflation numbers out of Australia will also take the spotlight on Wednesday. CPI Inflation (Consumer Price Index) is forecast to ease to 2.7% in August, down from 3.3% in July, consequently penetrating the upper range of the RBA’s 2-3% inflation band, which would be welcomed news by policymakers. Overall, markets are not pricing in a rate cut until February next year.

Amid cooling inflation, the Swiss National Bank (SNB) is widely expected to reduce its Policy Rate on Thursday; however, markets remain uncertain whether the SNB will cut by 25 or 50bps. A rate cut could weigh on the Swiss franc (CHF), providing some welcome relief for domestic industry as the CHF has strengthened for four consecutive months against the USD and euro.

Thursday will also see the final estimate for Q2 2024 US GDP, along with weekly jobless filings and durable goods orders data. Eyes will also be on Friday’s PCE Price Index for clues about future rate decisions. Heading into the event, economists forecast that the YoY PCE inflation eased to 2.3% in August, from 2.5% in July, with core PCE inflation expected to have increased to 2.7% from 2.6% in July. As briefly alluded to above, the updated economic projections from the Fed last week showed YoY PCE inflation was lowered to 2.3% for 2024 from 2.6% (prior forecast) and core PCE inflation projections were reduced to 2.6% from 2.8% (prior forecast).

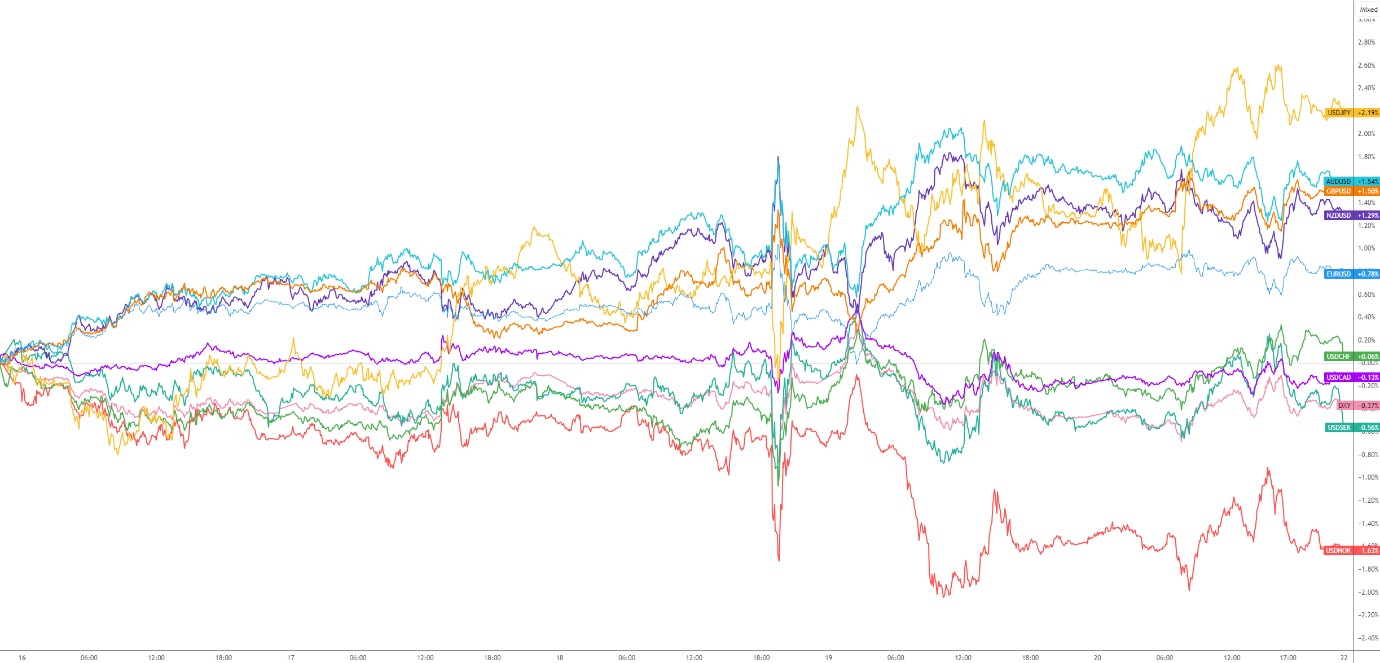

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,