Week ahead – Traders lock gaze on NFP after Thanksgiving holiday [Video]

-

Will the NFP data corroborate bets of a Fed pause?

-

Loonie traders await employment numbers as well.

-

Australia’s GDP to verify whether bets of May RBA cut are realistic.

-

Euro could take directions from ECB President Lagarde.

![Week ahead – Traders lock gaze on NFP after Thanksgiving holiday [Video]](https://editorial.fxstreet.com/images/Macroeconomics/EconomicIndicator/Employment/NFP/america-back-to-work-gm178972493-25143312_XtraLarge.jpg)

NFP and ISM PMIs to shape Fed expectations

The US dollar took a breather this week, pulling back even after being temporarily boosted by US President-elect Donald Trump’s tariff threats on Canada, Mexico and China.

Perhaps traders decided to capitalize on their previous Trump-related long positions heading into the Thanksgiving Holidays and ahead of next week’s all-important data releases. Market pricing is far from suggesting that investors’ concerns about a Trump-led government are receding.

This is evident by Fed funds futures still pointing to a strong likelihood of a pause by the Fed at the turn of the year. Specifically, there is a 35% chance for policymakers to take the sidelines in December, with the probability of that happening in January rising to around 58%. What’s also interesting is that there is a decent 27% likelihood for the Committee to refrain from hitting the rate cut button at both gatherings.

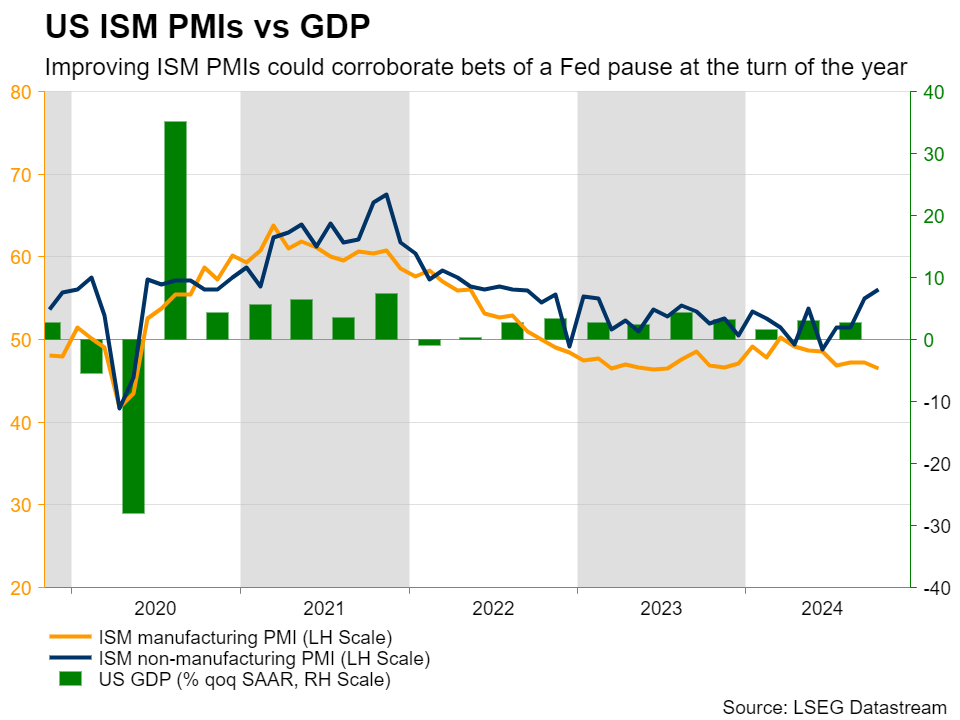

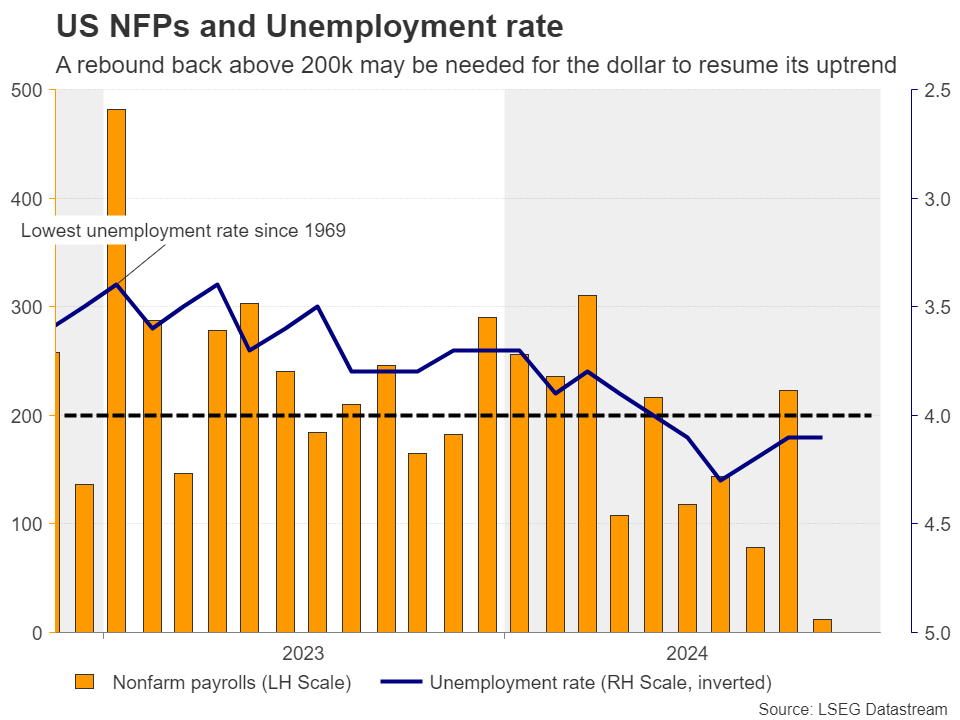

With that in mind, next week, market participants are likely to pay extra attention to the ISM manufacturing and non-manufacturing PMI data for November, due out on Monday and Wednesday, but the highlight of the week is likely to be Friday’s Nonfarm payrolls for the same month.

With inflation proving somewhat hotter than expected in October, the prices charged subindices of the PMIs may be closely monitored for signs as to whether the stickiness rolled over into November. The employment indices will also be watched for early clues regarding the performance of the labor market ahead of Friday’s official jobs data.

Should the ISM PMIs corroborate the notion that the world’s largest economy continues to fare well, the probability for the Fed to take the sidelines at the turn of the year will increase, thereby refueling the dollar’s engines. However, whether a potential rally will evolve into a strong impulsive leg of the prevailing uptrend will most likely depend on Friday’s numbers. Following October’s 12k, which was the smallest gain since December 2020, Nonfarm Payrolls may need to return above 200k for investors to become more confident in the dollar uptrend.

The JOLTs job openings for October on Tuesday and the ADP employment report for November on Wednesday could also offer clues on how the US labor market has been performing.

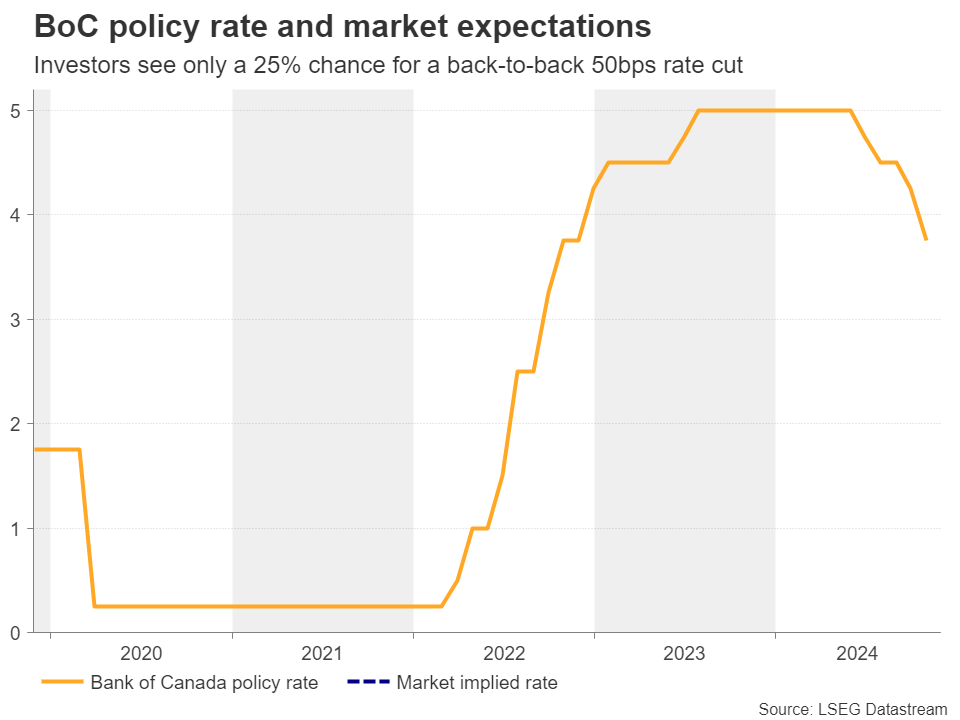

Is a back-to-back 50bps cut off the table for the BoC?

At the same time with the US jobs data, Canada releases its own employment report for November. At its latest gathering, on October 23, the BoC cut interest rates by 50bps to support economic growth and keep inflation close to 2%, adding that if the economy evolves broadly inline with their forecasts, further reductions will be needed.

Investors were quick to pencil in a strong likelihood for a back-to-back double rate cut, but the hotter-than-expected CPI numbers for October made them somewhat change their mind. Currently there is only a 25% chance of such a bold move, with markets becoming more convinced that a quarter-point cut could be enough.

With that in mind, a strong report on Friday could further weigh on the chances of a double cut by the BoC and thereby support the loonie. Nonetheless, an upbeat employment report may not be enough for the currency to change orbit and begin a bullish trend. More threats by US president-elect Trump about tariffs on Canadian goods could result in more wounds for the currency.

Strong GDP could keep the RBA on hold for longer

From Australia, the GDP data for Q3 are coming out on Wednesday, during the Asian morning. The RBA is the only major central bank that has yet to press the rate cut button in this easing cycle, with market participants believing that the first 25bps reduction is likely to be delivered in May.

The latest monthly inflation data revealed that the weighted CPI held steady at 2.1% y/y, but the headline rate rose to 2.3% y/y from 2.1%. With the quarterly prints also pointing to weighted and trimmed mean rates for Q3 at 3.8% and 3.5% respectively, it may take time before this Bank starts considering lowering rates, and a strong GDP number for that quarter could prompt investors to push further back the timing of the first reduction.

This could prove positive for the Aussie, but similarly to the Canadian dollar, it may be destined to feel the heat of Trump’s tariffs as the president-elect has pledged to hit China with even bigger charges than Canada.

Will ECB’s Lagarde agree that a 50bps cut may not be needed?

In the Euro area, although Germany’s preliminary inflation numbers for November came in below expectations, they still revealed some stickiness, with the headline rate rising to 2.2% y/y from 2.0%. The Eurozone’s headline rate also moved higher, to 2.3% y/y from 2.0%.

Combined with hawkish remarks by ECB member Isabel Schnabel who said that rate cuts should be gradual, this weighed on the probability of a 50bps reduction by the ECB at its upcoming meeting, despite the disappointing flash PMIs for the month. Currently the probability for the ECB proceeding with a double cut on December 12 stands at around 20%.

Having that in mind, next week, euro traders may lock their gaze on a speech by ECB President Lagarde on Wednesday, who will make an introductory statement before the Committee on Economic and Monetary policy Affairs (ECON) of the European Parliament. They may be eager to get more information about how the ECB is planning to move forward.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.