Week ahead: Inflation data on the radar

Another week has come and gone. The US Federal Reserve (Fed), the Bank of England (BoE), and the Bank of Japan (BoJ) all left their respective policy rates unchanged. The Fed underlined increased economic uncertainty (most central banks emphasised similar concerns), with growth (inflation) forecasts revised lower (higher). The BoE’s meeting was a bit of a snoozer, though the vote split echoed assumed more of a hawkish vibe – hence the immediate (albeit short-lived) rally in the British pound (GBP), and the BoJ hinted at further policy firming down the road amid recent data.

The week ahead – the final full week of March if you believe it – provides plenty to get our teeth into ahead of 2 April. This is a date many will have jotted down, a day when US President Donald Trump intends to introduce broad reciprocal tariffs, which, according to him, will be a ‘liberating day for America’.

S&P global PMIs

Monday kicks off with S&P Global flash PMIs (Purchasing Managers’ Indexes) for March for several countries. For those new to these data, these reports offer investors insight into how businesses are faring under the current economic landscape and, consequently, can (and often do) move the market’s dial. They’re essentially a survey of purchasing managers that asks respondents their assessment of business conditions, including key categories such as prices and employment within the industry.

These reports will have a lot of attention this week, not only because they help show how businesses react and plan for what seems like an ever-changing landscape of tariffs/geopolitics but also because you may recall that February’s US service PMI dipped into contractionary territory to 49.7 (down from January’s print of 52.9 and marked a 25-month low). Although February’s print has since been revised higher, it unearthed growth concerns and led to a meaningful selloff in US equities from all-time highs of 6,147 (as of last week’s close, the S&P 500 is down 7.4%). Economists estimate that the US services PMI will come in slightly lower at 50.8 (versus the upwardly revised 51.0 print in February), with the manufacturing PMI expected to ease to 51.8 (versus the upwardly revised reading of 52.7 in February).

In addition to the US, PMIs from Europe and the UK will be released. For Europe, the services (manufacturing) PMI is expected to increase to 51.0 (48.2) from 50.6 (47.6) in February, while for the UK, the services (manufacturing) PMI is expected to decrease to 50.9 (46.4) from 51.0 (46.9) in February.

Australian and UK inflation; UK spring statement

Wednesday will be busy for market participants, with Australian and UK CPI inflation data (Consumer Price Index) on the docket, followed by UK Chancellor Rachel Reeves presenting her Spring Statement to Parliament.

Australian CPI inflation rose by 2.5% on a year-on-year basis (YY) in January, matching the December 2024 print. Current estimates suggest inflation could remain unchanged again in February, though we do have an estimate range between a high of 2.6% and a low of 2.3%. At its February meeting, the Reserve Bank of Australia (RBA) reduced the cash rate target by 25 basis points (bps) to 4.10%. While this marked the first time since late 2020 that the RBA has cut rates, the Board echoed caution regarding further policy easing, citing upside inflation risks, a resilient jobs market, and uncertainty regarding US President Donald Trump’s tariffs. This was reiterated in the RBA’s meeting minutes released earlier this month, and essentially aired the notion that the previous rate cut was not an indication of things to come. Understandably, markets are largely ruling out another rate cut next month, though May's (-18 bps) and July’s (-29 bps) meetings are certainly on the table. Therefore, lower-than-expected data this week could have investors ramp up rate-cut bets and consequently weigh on the Australian dollar (AUD); conversely, an upward surprise may underpin the currency.

In the UK, UK CPI inflation rose by 3.0% in January YY – its highest rate since early 2024. February’s reading (YY) is expected to have cooled slightly to 2.9% (from 3.0%), with the core measures (YY) also forecast to have eased to 3.5% (from 3.7%). Last week saw the Bank of England (BoE) maintain the bank rate at 4.50% with an 8-1 majority, and like the RBA, cautioned that global trade uncertainty has intensified. The BoE is in a tricky spot right now amind stagflationary risks – balancing inflation against downside growth risks as well as fragile confidence. Although the vote split was modestly hawkish (consensus: 7-2), it was a difficult one to trade, in my opinion. Looking ahead to this week’s UK inflation numbers. Similar to the Australian inflation report, were UK data to come in lower than expected, the British pound (GBP) could be sold, while any upward surprises could benefit the GBP.

Coupled with the Office for National Statistics (ONS) reporting a £100 million increase in public sector net borrowing in February (compared to February last year), I think it is fair to say that things are not heading in the right direction for Reeves. Increasing austerity fears and having staked her reputation on growing the UK economy, Reeves is not expected to make any tax changes but is anticipated to announce growth downgrades and is set to push through one of the largest spending squeezes seen in years to plug the black hole in the public finances that has emerged from slower growth and rising debt repayments.

US PCE data

Friday’s PCE price index data (Personal Consumption Expenditures) for February is one to watch. Most will already know that the Fed sets an inflation target of 2.0%, measured by headline PCE data. Several analysts often cloud this with core PCE data and what the Fed members prefer. I do not know the preference of each Fed member; I am just going on with what I have seen explicitly stated by the Fed regarding how the central bank measures its inflation target.

Although headline data for the CPI and PPI (Producer Price Index) eased in January, under the hood, some of the components that feed into the PCE data came in hotter, suggesting the possibility of higher/stubborn PCE numbers. Expectations heading into the event show economists forecast month-on-month (MM) and year-on-year (YY) headline PCE data to remain unchanged at 0.3% and 2.5%, respectively. However, the estimate range for the latter is between a high of 2.7% and a low of 2.4%. On the core front – excluding volatile food and energy components – PCE is also expected to remain unchanged on a MM basis at 0.3%, but is forecast to tick slightly higher YY at 2.7% (from 2.6%).

As briefly noted at the beginning of this piece, the Fed met last week and kept the fed funds target range on hold. This was primarily anticipated across the board, though the central bank did note that ‘uncertainty around the economic outlook has increased’, essentially removing the sentence: ‘the economic outlook is uncertain’. In his press conference, Fed Chairman Jerome Powell also emphasised that inflation remains somewhat elevated, but acknowledged that inflation has been rising, ‘partly in response to tariffs’. He stated that it is too early to observe a significant impact on economic data due to tariffs and made note that upside risks to inflation have increased in the short term, but said that the central bank’s longer-term goal of reaching the 2.0% inflation target remains in place. While the March dot-plot showed a small increase in the number of participants forecasting no rate reductions this year, the Fed continue to expect two rate cuts this year, similar to money market expectations (-66 bps of easing priced in).

Should PCE data exceed the median estimates, expect a bid across the USD and US Treasury yields as investors will likely increase pare rate-cut bets, with follow-through selling in equities.

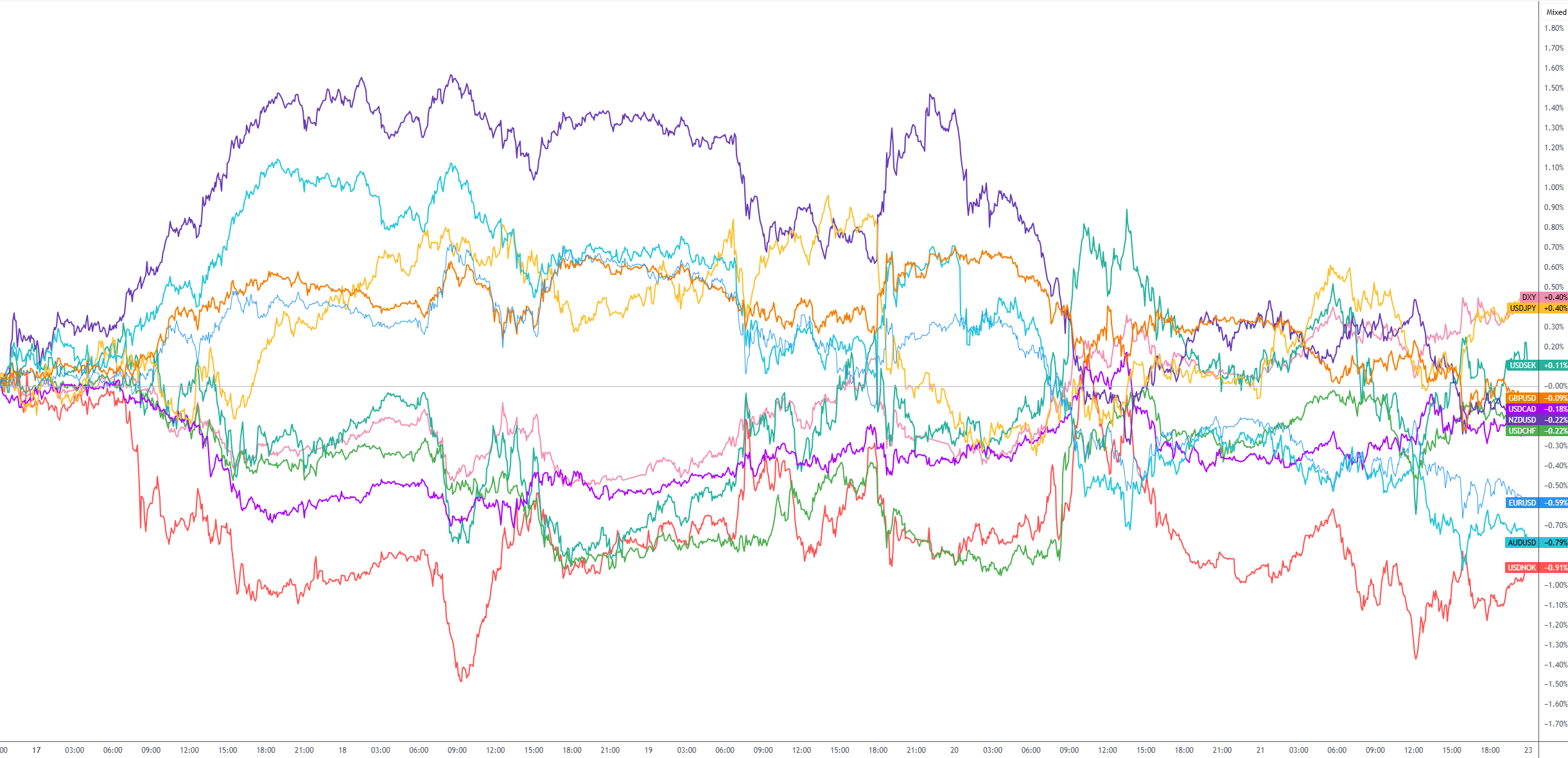

Weekly G10 FX performance

Chart created using TradingView

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,