Week Ahead – Fed minutes, US Retail Sales and UK CPIs the highlights of a packed week [Video]

![Week Ahead – Fed minutes, US Retail Sales and UK CPIs the highlights of a packed week [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/FED/the-federal-reserve-begins-last-meeting-of-2008-18976491_XtraLarge.jpg)

The dollar pulled back after the miss in the US inflation data, but traders may have another opportunity to adjust their dollar positions as next week’s agenda includes the minutes from the latest Fed meeting and the retail sales for July. The pound will also enter the limelight as the UK CPIs could confirm whether investors were correct to slash their hike bets following the latest BoE gathering. Other releases include the RBNZ decision, where no action is expected, and Canada’s CPIs.

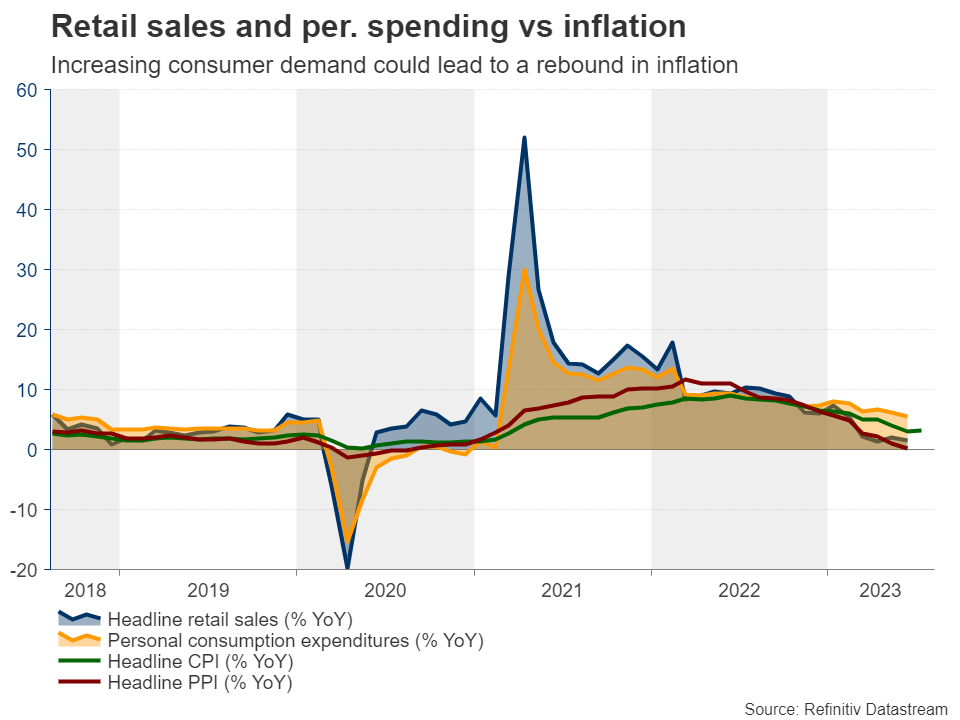

Dollar traders turn attention to Retail Sales and Fed minutes

Following the lower-than-expected CPI data for July, investors remained convinced that the Fed will not proceed with any other hikes and that nearly 130bps worth of rate reductions may be warranted for next year. This kept the euro/dollar uptrend intact, despite the US currency holding strong since July 18, as the pair rebounded somewhat from the upward sloping line drawn from the low of September 26.

At the latest FOMC meeting, Fed Chair Jerome Powell said that they will make decisions meeting by meeting, closely watching economic data, adding that they could hike again in September if the data suggests so, but also that they could choose to hold steady.

Therefore, after the CPIs, Tuesday’s retail sales and Wednesday’s industrial production for July may also be of high importance as they could determine whether the dollar can stage a solid comeback or not. Both the headline and excluding-autos sales are expected to have accelerated to 0.4% month-on-month from 0.2%, while industrial production is forecast to have rebounded 0.3% m/m after shrinking 0.5%.

Although these releases are unlikely to significantly alter the market’s Fed implied rate path on their own, they could add to hopes of a soft landing, while they could make it easier for investors to eventually rethink the probability of a September hike if later on Wednesday, the minutes of the last Fed meeting reveal that there was a decent number of policymakers that were in favor of delivering more hikes before signaling the end of this tightening cycle.

Combined with the US Treasury’s pledge to issue more bonds, this may help yields and the dollar move higher. At the same time, equities may extend their latest correction. The opposite may be true if the data come in softer than expected and the meeting minutes suggest that most Fed officials were skeptical about whether more hikes are needed.

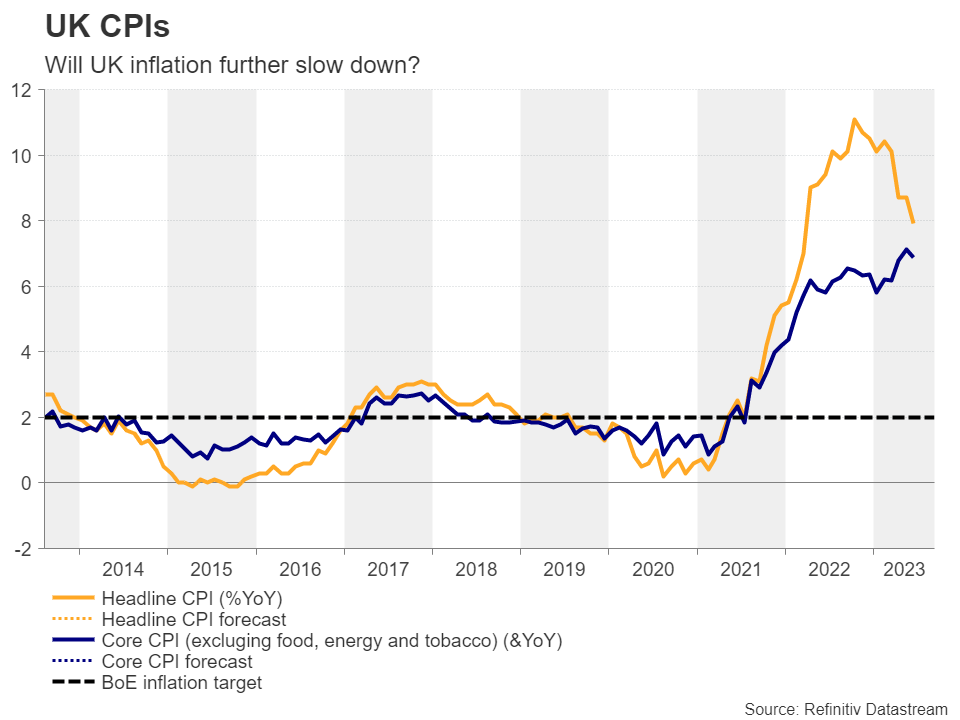

Will UK inflation come further down?

The BoE raised interest rates by the expected 25bps when it last met, but failed to appear as hawkish as many may have anticipated, with Governor Bailey noting that he didn’t think there was a case for another 50bps hike.

Following the decision, investors slashed their rate-hike expectations, now seeing only a 70% probability of a quarter point hike at the September meeting, with the remaining 30% pointing to no action. As for the future, they are anticipating only one more quarter-point increment before this Bank ends its own tightening crusade as well.

Next week, pound traders will likely pay close attention to the UK CPIs for July, due out on Wednesday, as they try to evaluate whether their assessment appears correct or not. No forecast is currently available, but the S&P Global PMIs suggested further cooling of inflationary pressures, which tilts the risks surrounding the CPIs to the downside. Further declines in the CPI rates, especially the core one, could add credence to investors’ choice to lower their implied rate path and may further weigh on the pound.

The nation’s employment report for June and retail sales for July are also due to be released on Tuesday and Friday respectively.

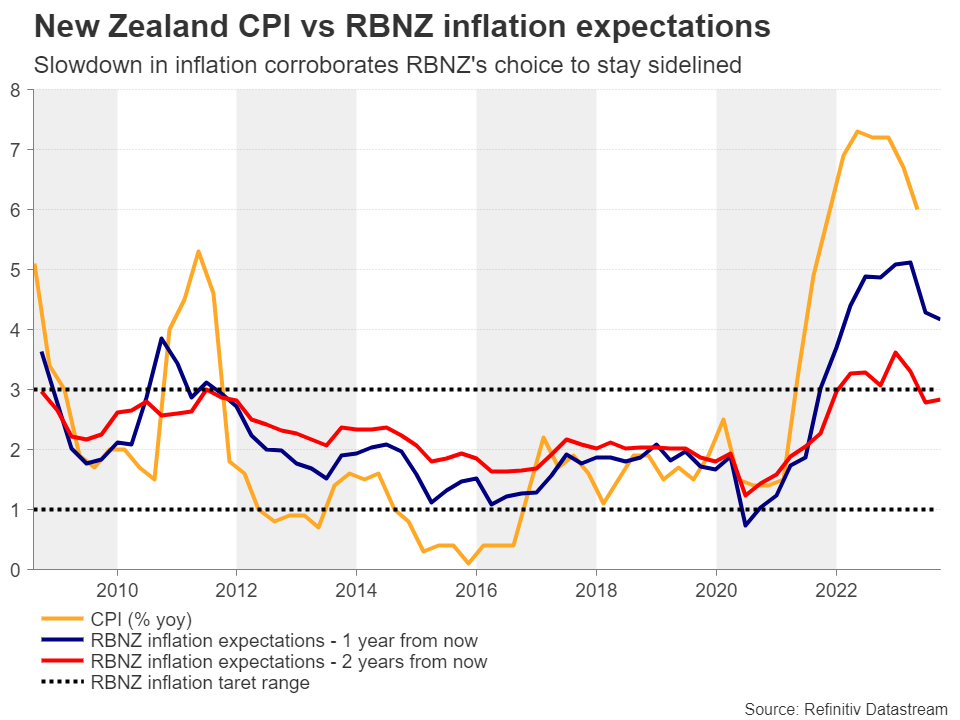

RBNZ to stay sidelined, Kiwi exposed to risk sentiment

The RBNZ meets on Wednesday and staying sidelined appears a virtual certainty, with the probability of a hike resting at a mere 4%. Back in May, this Bank signaled that it is done raising rates and in July, it took the sidelines, saying that high interest rates had constrained spending as anticipated.

With data revealing that the CPI rate fell to 6.0% in Q2 from 6.7%, it seems that this meeting is unlikely to result in any fireworks, as the cooling in inflation corroborates officials’ past choices.

Thus, the kiwi experiencing huge volatility due to this decision is very doubtful, rather it may stay more sensitive to the broader market sentiment and specifically to developments surrounding the Chinese economy.

China data dump, RBA minutes and Australia jobs data

Speaking about China, the world’s second largest economy releases its fixed asset investment, industrial production, and retail sales numbers for July on Tuesday. Following the worsening contraction in both exports and imports, as well as the fall in consumer prices, another set of disappointing numbers could weigh further on market sentiment and especially the currencies whose nations have close trade ties with China, like the kiwi and the aussie.

Aussie traders will also have to digest the RBA meeting minutes on Tuesday and Australia’s employment report on Thursday, although they are nearly certain that the RBA will remain sidelined at its September meeting.

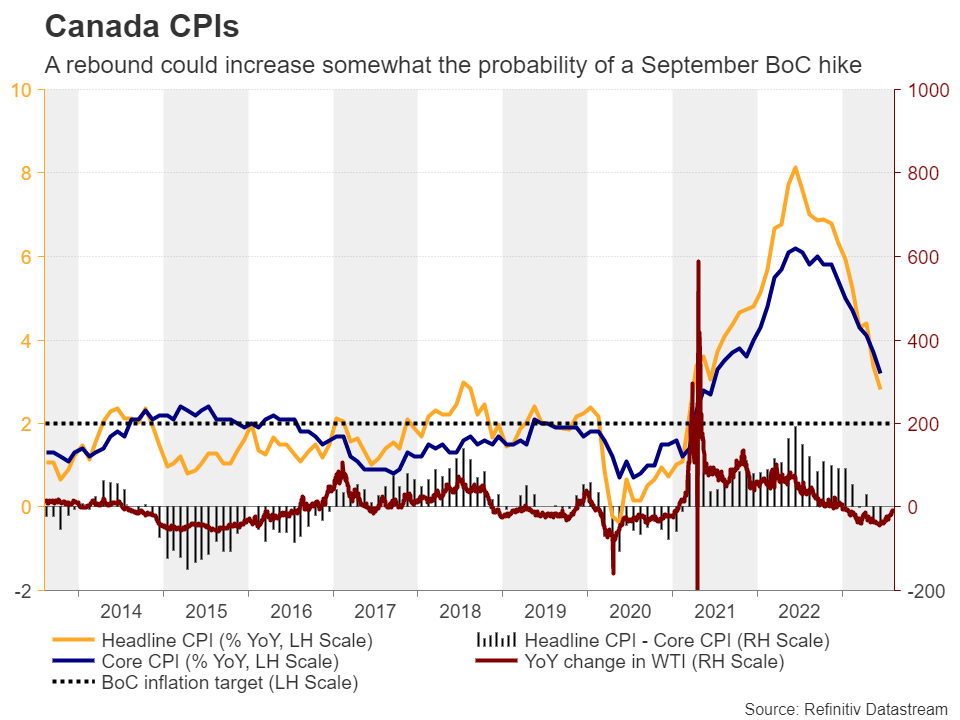

More data from Canada and Japan

The Canadian dollar has also been on the back foot lately, despite the strong recovery in oil prices. Perhaps the deteriorating risk appetite and a strong US dollar did not allow traders to consider buying the loonie.

They will however have an opportunity to reevaluate the outlook of this currency on Tuesday when Canada’s CPI data for July are coming out. With the year-on-year change in oil prices rebounding strongly lately, the headline CPI rate may be poised to rebound from 2.8% y/y. If the core rate increases notably as well, then the probability of another rate increase by the BoC at the September gathering may increase from its current level of around 20% and thereby add some support to the loonie. The opposite may be true in the case of an inflation slowdown.

The yen has been under pressure for the whole week as the slowdown in Japan’s wage growth may have weighed on expectations of further tightening by the BoJ. On Tuesday, the nation’s preliminary GDP numbers for Q2 are due to be released and the forecast points to a small acceleration to 0.8% qoq from 0.7%. That said, a potential miss in this data set may corroborate the view that Japanese officials may need to wait for a while longer, and thereby push the yen lower, especially if Friday’s CPIs reveal a slowdown.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.