Week ahead – ECB poised to cut again, US CPI to get final say on size of Fed cut [Video]

-

ECB is expected to ease again, but will it be another ‘hawkish cut’?

-

US CPI report will be the last inflation update before September FOMC.

-

UK monthly data flurry begins with employment and GDP numbers.

![Week ahead – ECB poised to cut again, US CPI to get final say on size of Fed cut [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/ECB/flag-of-the-european-community-eurotower-24637025_XtraLarge.jpg)

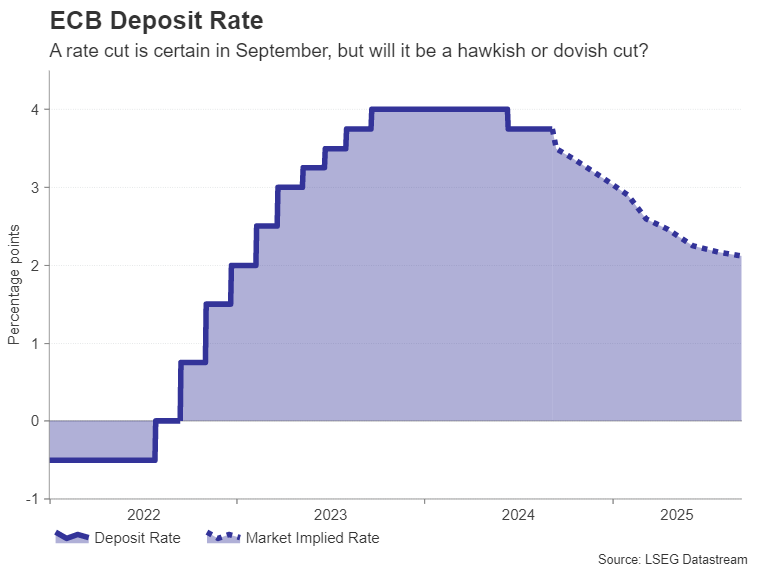

ECB to cut rates for second time

The European Central Bank’s carefully choreographed rate-cutting cycle got off to an awkward start in June after last-minute data upsets. For credibility’s sake, policymakers had only one choice – press ahead with the planned 25-basis-point rate reduction but present it as a ‘hawkish cut’.

Fortunately for the doves and struggling European businesses, the case for further policy easing has strengthened since the last gathering in July when rates were kept on hold. Headline inflation dipped to 2.2% y/y in August and the rebound in euro area growth has been tepid.

The current economic backdrop has potentially set the stage for downward revisions to the ECB’s quarterly inflation and GDP projections, which are due to be published on the day of the meeting on Thursday. More to the point, President Christine Lagarde may now feel that she can tone down the emphasis on “data-dependent and meeting-by-meeting approach” and confidently flag further cuts ahead.

There is one problem, however, and that is the uptick in services CPI in August, which rose to the highest since October 2023, reaching 4.2% y/y. Whilst this isn’t concerning enough to prevent the ECB from sounding more dovish at the September meeting, Lagarde will likely maintain some caution in her press briefing.

If Lagarde signals a rate-cut path that’s shallower than what investors have priced in, the euro could resume its uptrend, having taken a knock from a somewhat firmer US dollar.

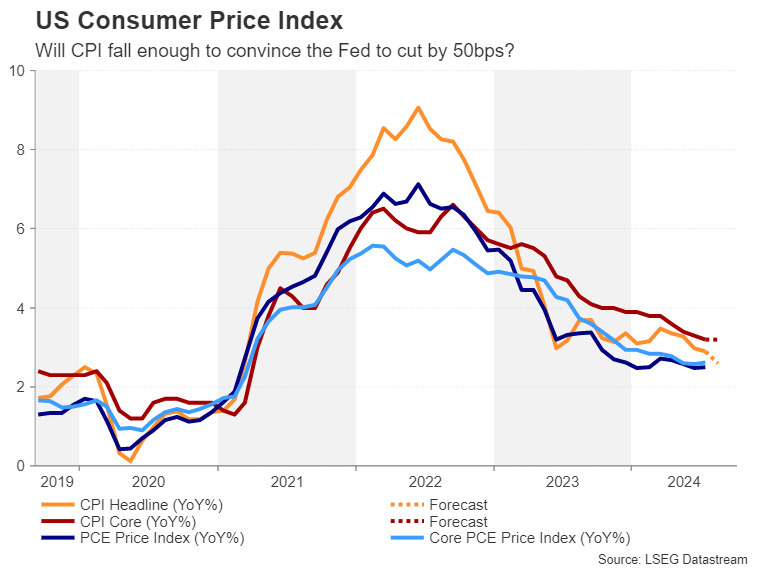

Will US CPI back case for 50-bps cut?

Talking of the dollar, it’s been navigating through choppy waters lately amid the ongoing uncertainty about whether the Fed will lower rates by 25 bps at its upcoming meeting or by 50 bps. The Fed’s much awaited policy shift finally came in August at the central banks’ annual symposium in Jackson Hole.

Chair Powell acknowledged the cracks that have started to appear in the labour market and in doing so, he opened the door to a possible 50-bps move in September. Much of the commentary since then hasn’t supported the need for aggressive action as the data has been mostly solid.

The big question is how much will the Fed prioritize its employment mandate over price stability when upside risks to inflation remain? The ISM’s prices paid gauges for both manufacturing and services edged up in August even as employment contracted for the former and barely grew for the latter.

Wednesday’s CPI report will be the last piece of the jigsaw ahead of the September decision and should provide some clarity as to what to expect. The headline CPI rate cooled to 2.9% y/y in July and is expected to fall again to 2.6% in August. The core rate, however, is forecast to have stayed unchanged at 3.2%.

If the above numbers are confirmed, the Fed is more likely to deliver a ‘dovish cut’ of 25 bps. But there would have to be a significant downside surprise for there to be a realistic chance of a 50-bps reduction.

Investors have priced in a close to 40% probability of a 50-bps cut so there is room for disappointment, with the dollar possibly turning higher if the CPI data is more or less in line with expectations or stronger.

Producer prices will follow on Thursday and Friday’s preliminary survey on consumer sentiment in September by the University of Michigan will be important too, particularly the one- and five-year inflation expectations.

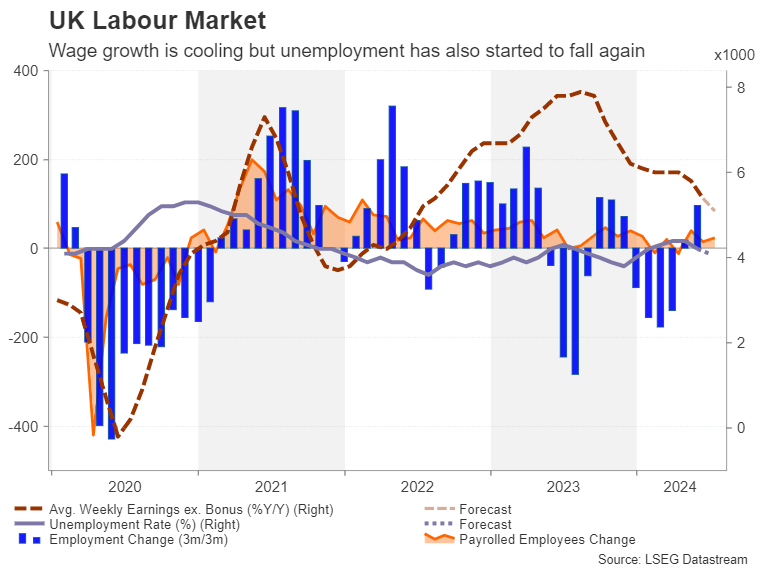

Pound eyes UK releases as BoE decision looms

The Bank of England is expected to buck the central bank trend in September and keep rates on hold when it meets on the 19th. The UK economy bounced back strongly in the first half of 2024 and with wage growth and services inflation still elevated, the BoE can afford to pause after cutting rates for the first time this cycle in August.

But the decision may yet end up being a much closer call than anticipated depending on the incoming slew of data ahead of the September meeting. On Tuesday, the employment report for July will be watched for further signs that the UK’s labour market is stabilising after significant job losses at the start of the year.

The unemployment rate declined 0.2 percentage points to 4.2% in June, but another big drop might not be so welcome as wage growth is finally headed towards levels that would be more consistent with inflation of 2.0%. A pickup in hiring could refuel wage pressures, hindering the BoE’s fight against inflation.

The spotlight on Wednesday will be on the July GDP readings, which include a breakdown of services and manufacturing sectors.

The odds for no change in September currently stand at around 75% so sterling could come under heavy pressure if next week’s releases disappoint and push up the probability of a 25-bps cut closer to 50%.

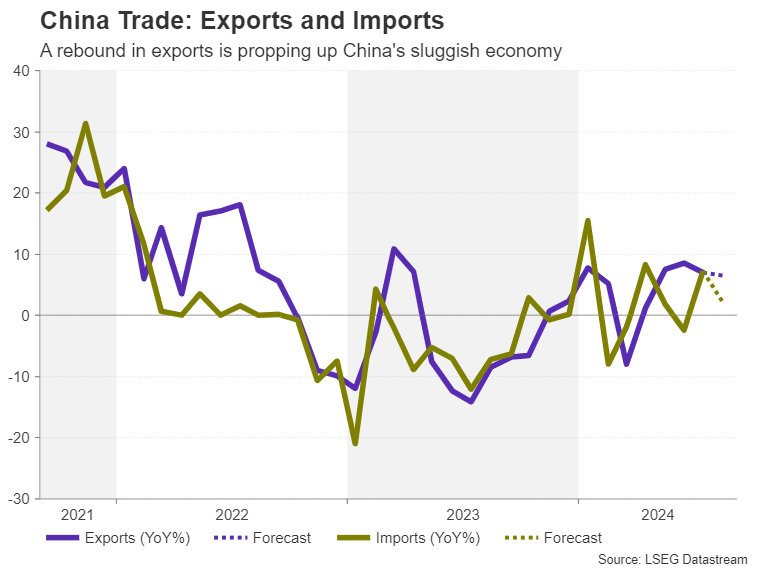

Spotlight on Asia at start of week

Amid lingering worries about China’s sluggish economy, CPI and PPI numbers on Monday followed by trade figures for August on Tuesday might attract some attention for risk-sensitive currencies such as the Australian dollar. There’s been a decent rebound in exports in recent months. Another strong print in August might provide some boost to risk appetite in the short term but do little in lifting the overall gloom about China’s economic outlook.

In Japan, it will be a busy week for data, the highlight of which will be Monday’s GDP revision. Second quarter GDP growth is expected to be revised higher from the initial estimate of 0.8% y/y. A higher-than-anticipated figure could boost expectations of another rate hike by the Bank of Japan this year, bolstering the yen’s latest rally.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl