-

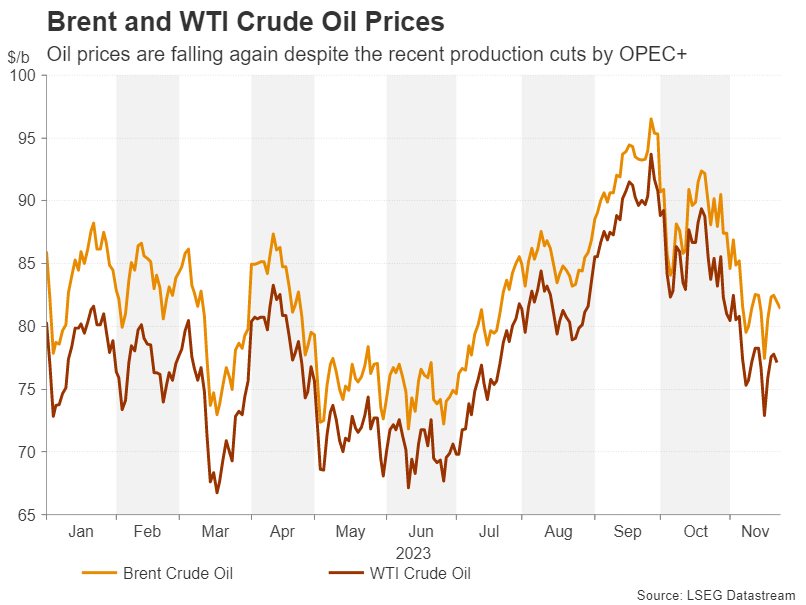

Oil’s fortunes hinge on OPEC+ meeting outcome on Thursday.

-

Eurozone flash inflation and US core PCE also due on Thursday.

-

RBNZ to likely hold rates on Wednesday.

-

Loonie faces GDP and employment tests in addition to OPEC+ decision.

Will OPEC+ agree to production cuts?

Amid weakening growth prospects for the major economies in 2024, expectations that the big oil producers will soon announce further production cuts had been the only thing keeping a floor under the price of oil lately. But that floor broke when OPEC unexpectedly announced that the meeting scheduled for Sunday, November 26, has been postponed to the following Thursday.

Investors have interpreted this as a sign that there are growing differences within the alliance about whether or not additional production cuts are necessary. The likely scenario is that Saudi Arabia, who is the keenest to prevent prices from spiralling further downwards, will find a way to negotiate some kind of a compromise.

The only problem is that even if that turns out to be the case and OPEC+ delivers a package aimed at tightening supply over the coming months, the reductions will almost certainly not be as deep as Saudi Arabia had originally hoped. Furthermore, any new cuts beyond those possibly to be announced on Thursday will now probably be off the table.

When also considering the rising output by countries outside of OPEC+, particularly the United States, it’s hard to see a positive outcome for oil prices. Even if there is a rebound, it will likely be a corrective one rather than an actual trend reversal.

Deflation risks if Oil slips below $80

There are implications too for the major currencies if OPEC+ fails to come up with substantial cuts. Elevated oil prices have been the main reason why central banks such as the Bank of England and European Central Bank have had to be so hawkish, and why even the Bank of Japan is now contemplating exiting negative rates.

But this is true to a much lesser extent for the Federal Reserve, as excess demand has been as much if not more of a problem for the US economy in the fight against high inflation.

Therefore, should oil prices drop and stay below $80 a barrel, sticky inflation would become much less of a threat for the ECB, BoE and BoJ than for the Fed, and monetary policy divergence could switch back in favour of the US dollar.

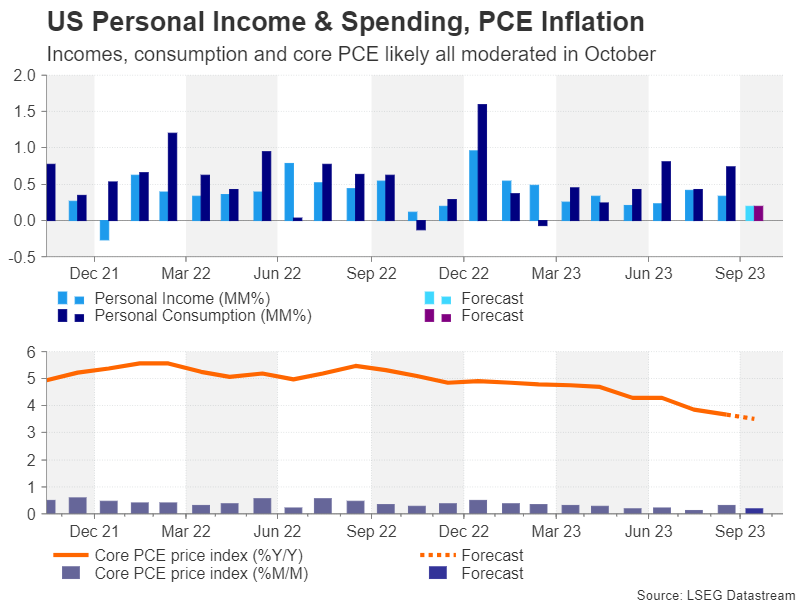

Core PCE to headline packed US calendar

Looking at next week’s agenda for the US, there may be some good and bad news for the greenback. The housing market will be in focus at the start of the week, with October new home sales out on Monday and the Case-Shiller 20-city home price index on Tuesday. Pending home sales will follow on Thursday.

On Wednesday, the third quarter GDP estimate is expected to be revised up slightly from 4.9% to a 5.0% annualized pace, while on Friday, the ISM manufacturing PMI will be important. The ISM manufacturing PMI has been in contractionary territory for the past year and although it is forecast to have edged up in November, it’s expected to remain below 50 at 47.7.

The real highlight, however, will be Thursday’s set of data, containing personal income and spending, as well as the core PCE price index. Both personal income and consumption are expected to have moderated in October, rising by just 0.2% m/m, suggesting that consumers started to tighten their belts at the start of the new quarter after going on a spending spree during the summer.

The all-important core PCE inflation gauge is projected to have slowed too, with forecasts pointing to a drop in the annual rate from 3.7% to 3.5% in October.

Assuming that there are no big surprises, the incoming data should support the view that inflation and the economy overall are cooling off. Markets are likely to take this as a sign that the Fed will have to begin cutting rates by the middle of 2024 if monetary policy isn’t to become too restrictive.

From the Fed’s perspective, however, there’s still some way to go before the 2% target is met and policymakers may attempt to steer investors in the right direction when a host of them hit the podium next week, including Chair Powell, who is scheduled to speak on Friday.

Hence, there are both upside and downside risks for the US dollar over the next seven days.

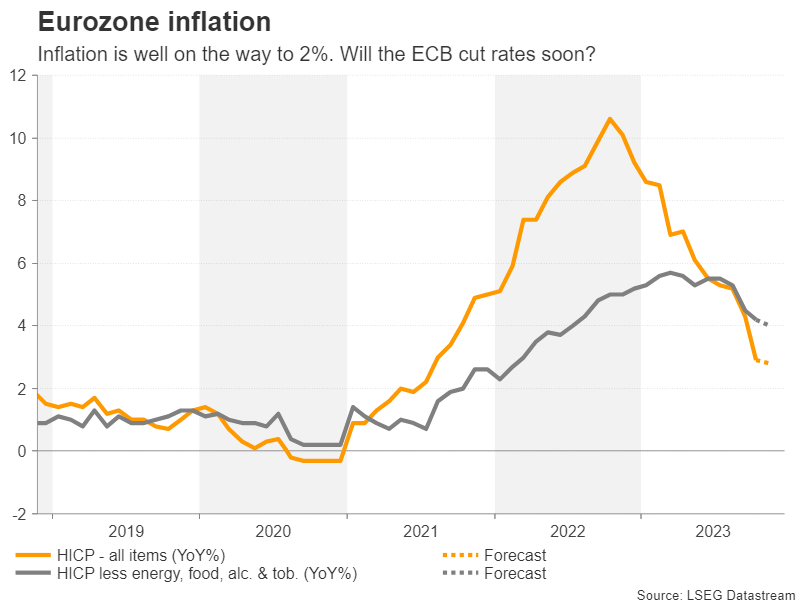

Further easing in inflation could pressure the Euro

For the euro, on the other hand, its latest uptrend could come under scrutiny from the Eurozone’s flash inflation readings due on Thursday. The Harmonised Index of Consumer Prices (HICP) is forecast to inch lower slightly in November from 2.9% to 2.8% - the lowest in more than two years. The core measure that strips out all volatile items is expected at 4.0% versus 4.2% in October.

With the Eurozone economy likely to have entered a technical recession in the fourth quarter and fears of a fresh energy crisis not materializing, some traders are betting that the ECB will cut rates before the Fed does next year. This raises question marks about whether the euro’s recovery can stretch beyond the critical $1.10 region.

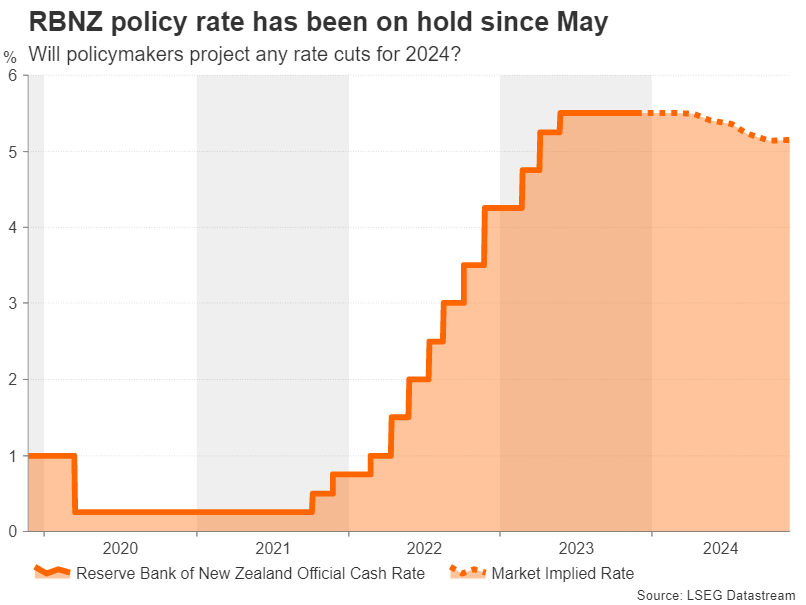

RBNZ could confirm end of rate hikes

The Reserve Bank of New Zealand meets on Wednesday and is widely anticipated to hold the official cash rate at 5.5%, having last raised it in May. Although inflation in New Zealand remains one of the highest among the advanced economies, it is falling and more importantly, tighter monetary policy is working in slowing the economy.

Unemployment is creeping higher, while consumption has been sluggish lately. This somewhat contradicts with the sharp pickup in business confidence over the past few months, although this may be linked more to the improving economic conditions in China and the increased hopes of a soft landing in the US than to the current domestic picture.

Nevertheless, policymakers will probably judge that no further tightening is needed, which then shifts the attention on how long rates will stay at current levels. The RBNZ will publish its updated quarterly projections on Wednesday and so much of the reaction in the New Zealand dollar will depend on whether there are any changes to the rate path.

Back in August, the RBNZ had predicted that rates will stay higher for longer, only being cut slightly towards the end of 2024. The kiwi could extend its rebound against the US dollar if the RBNZ no longer expects to cut rates at all in 2024.

Underperforming Loonie braces for a bumpy week

The coming week will be quite a crucial one for the Canadian dollar too as Q3 GDP numbers are due on the same day as the OPEC+ decision on Thursday, before the November employment report arrives on Friday.

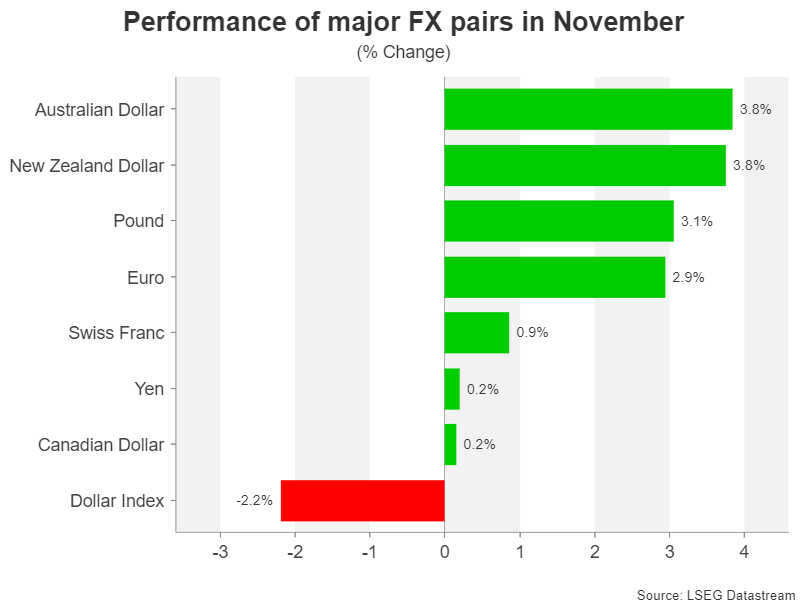

The loonie has been somewhat of a laggard among the major currencies in November, with its rebound looking the least convincing and the greenback’s broader uptrend from July remaining intact. The slide in oil prices since late September is mostly to blame for this.

But markets pricing in rate cuts for 2024 have also been a drag on the loonie. Only a couple of months ago, investors saw rates holding above 5.0% during the course of next year compared to at least three 25-bps cuts priced in currently.

Better-than-expected readings in GDP and jobs growth could help the loonie play catch up, but that would only be possible if OPEC+ agrees to extend the production cuts into 2024.

Aussie eyes CPI and Chinese PMI data

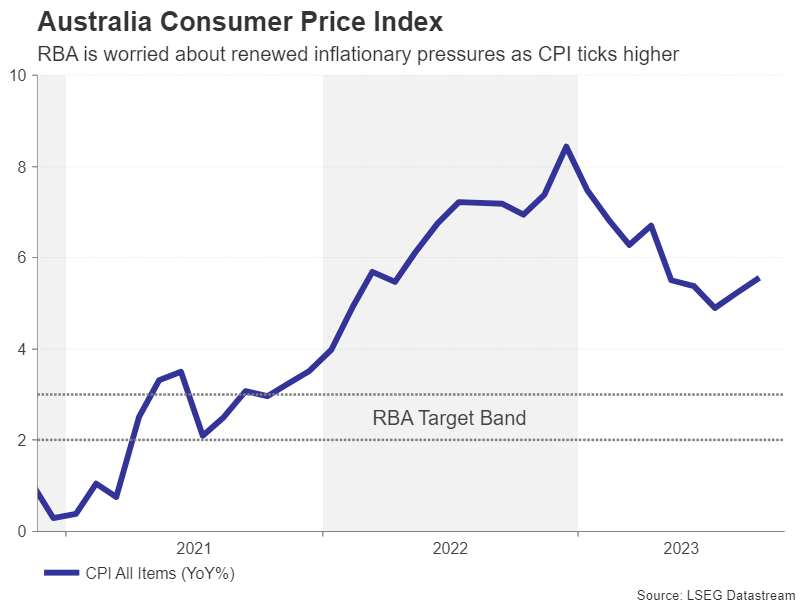

Not to be left out, the other of the commodity-linked currencies – the Australian dollar – will also be in the spotlight next week, with traders keeping an eye on both domestic and Chinese indicators. The aussie has enjoyed a strong rally over the past week as the Reserve Bank of Australia’s new chief, Michele Bullock, has continued to strike a hawkish tone amid renewed concerns about inflation, and so the monthly CPI prints out on Wednesday will undoubtedly grab a lot of attention.

Other Australian releases will include quarterly construction output and capital expenditure on Wednesday and Thursday, respectively, as well as retail sales on Tuesday. In addition, manufacturing PMIs out of China will be watched on Thursday and Friday amid ongoing angst among investors about the strength of the recovery in the world’s second largest economy and Australia’s largest trading partner.

Forex trading and trading in other leveraged products involves a significant level of risk and is not suitable for all investors.

Recommended Content

Editors’ Picks

EUR/USD clings to recovery gains above 1.0500 ahead of ECB policy announcements

EUR/USD holds the rebound above 1.0500 in the European session on Thursday amid a broad US Dollar retreat. However, the upside appears capped amid expectations for more ECB rate cuts in 2025. ECB policy announcements and Lagarde's press conference are on tap.

GBP/USD pulls back to 1.2750 as markets turn cautious

GBP/USD is pulling back to near 1.2750 in the European session on Thursday as traders turn cautious. The pair reverses earlier gains even as the US Dollar corrects downwards. The focus remains on the US PPI and Jobless Claims data.

Gold price sits near one-month high on Fed rate cut optimism and softer USD

Gold price seems to have stabilized following good two-way price swings and trades around the $2,720 area during the early European session, just below the highest level in more than a month touched earlier this Thursday.

European Central Bank set to cut interest rates again amid slow economic growth

The European Central Bank is expected to cut benchmark interest rates by 25 bps at the December policy meeting. ECB President Christine Lagarde’s presser will be closely scrutinized for fresh policy cues.

BTC faces setback from Microsoft’s rejection

Bitcoin price hovers around $98,400 on Wednesday after declining 4.47% since Monday. Microsoft shareholders rejected the proposal to add Bitcoin to the company’s balance sheet on Tuesday.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.