USD/JPY Weekly Forecast: Will the turn become a plunge?

- USD/JPY closes below 128.00 for the first time since April on Thursday.

- Higher Japanese inflation, fading US Treasury rates aid yen.

- Prime Minister Kishida comments on the weak yen and Japanese economy.

- FXStreet Forecast Poll predicts consolidation near 127.50.

After two months of unsurpassed weakness the Japanese yen has been lifted from its 20-year floor by a combination of economic, fundamental and technical factors that could herald a change in circumstances.

intro-637886531980401591.png)

The primary logic behind the 14% gain in the USD/JPY between March 7 and April 28 was the rise in US Treasury yields while returns on Japanese Government Bonds (JGB) were largely stable. Since trading above 3.0% in the early part of the month the US 10-year yield has drifted lower as recession fears have been mirrored in collapsing equity prices. The 10-year return closed at 2.893% on Thursday.

Federal Reserve Chair Jerome Powell has remained adamant that the central bank will fight inflation regardless of economic developments, but many in the markets doubt rate hikes could continue at their projected pace if the economy entered a recession.

Japanese inflation was markedly stronger in April than expected. National CPI was 2.5%, more than double the 1.2% rate in March and its highest in eight years. The consensus estimate was 1.5%. Core CPI came in at 0.8% on a -0.9% forecast and March’s -0.8% rate. It is possible that Bank of Japan (BOJ) might moderate its extremely accommodative monetary policy with inflation's strong showing.

Prime Minister Fumio Kishida somewhat unusually commented that rising raw material prices made worse by a weaker yen are making life difficult for households and businesses. His call for close ties with other central banks seemed to hint at coordination even if intervention to strengthen the yen is very unlikely. For intervention to have a chance of success it would have to be in conjunction with other major banks. The Bank of Japan (BoJ) would be unable to effect permanent change by itself.

China cut a key interest rate to help its lockdown ravaged economy which may aid Japan’s export sector and corporations doing business on the mainland.

Finally, several technical indicators suggest the USD/JPY may have reached a dead end. The MACD (Moving Average Convergence Divergence) has seen its negative divergence widen and the Relative Strength Index (RSI) has fallen for two weeks.

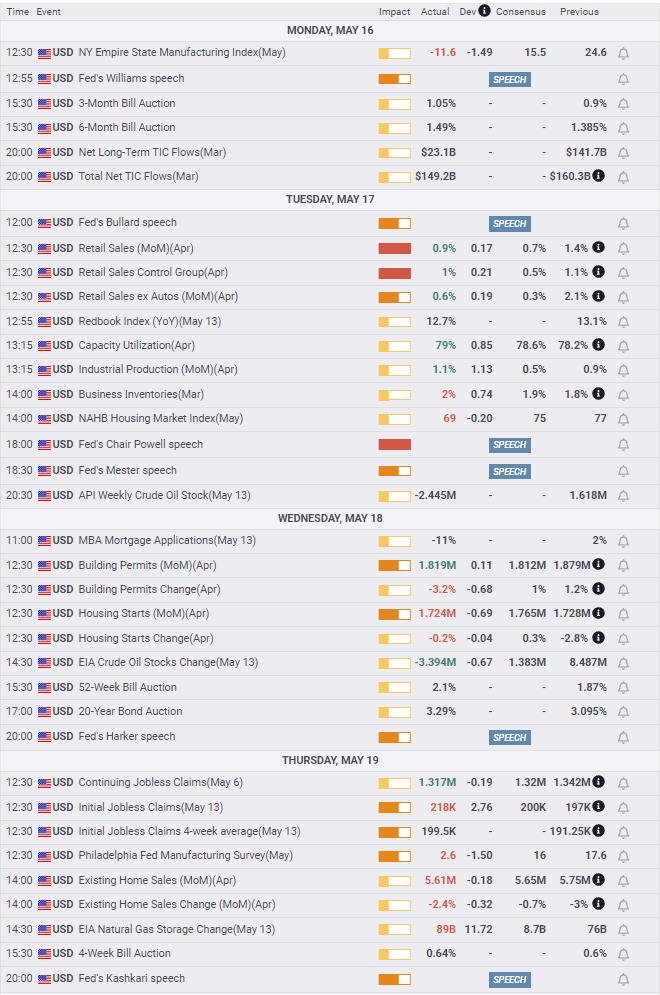

In the US, Retail Sales for April were better-than-expected and gave a temporary boost to stocks. Building Permits dropped sharply in April. Existing Home Sales, 90% of the US markets, fell to a 22-month low. Home purchases have been axed by rising mortgage rates which reached a 13-year high at 5.25% this week.

American equities fell for the eighth week in a row weighed down by poor profit reports from several major corporation and the dismal economic outlook from consumers

USD/JPY outlook

The US dollar has pulled back from multi-year highs against the euro, sterling, and all of the majors except the Canadian dollar. The Dollar Index has retreated from a more than two-decade high on May 12.

The run higher in the US dollar after the Russia invasion of Ukraine on February 24 is beginning to unwind as the stalemated war seems far less likely to produce any new shocks to the global economy.

Treasury yields in the US may have, at least temporarily, peaked and the next Federal Open Market Committee (FOMC) meeting is four weeks away on June 15. Treasury futures have the odds for a 50 basis point hike at 93.1% at that meeting, and an upper fed funds target of 3.0% or higher at 65.7% for the December 14 FOMC. Those odds have been relatively stable for a few weeks and are priced into the markets.

All told, the pressures for profit taking in the USD/JPY, currencies in general and the credit market will increase as markets move ahead. In the USD/JPY Fibonacci retracements of the March to May are untouched with the first 23.6% at 126.98 and the 38.2% level at 124.66.

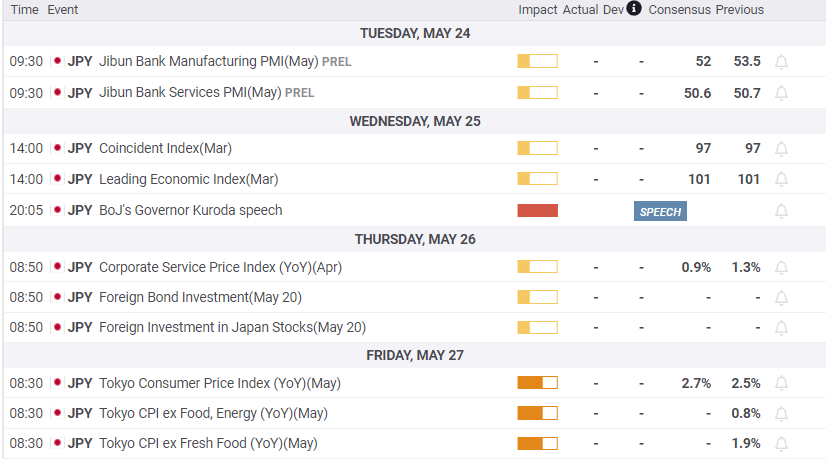

Japanese and US data in the coming week will provide no change in the picture. Tokyo CPI for May is expected to rise to 2.7% from 2.5% in April.

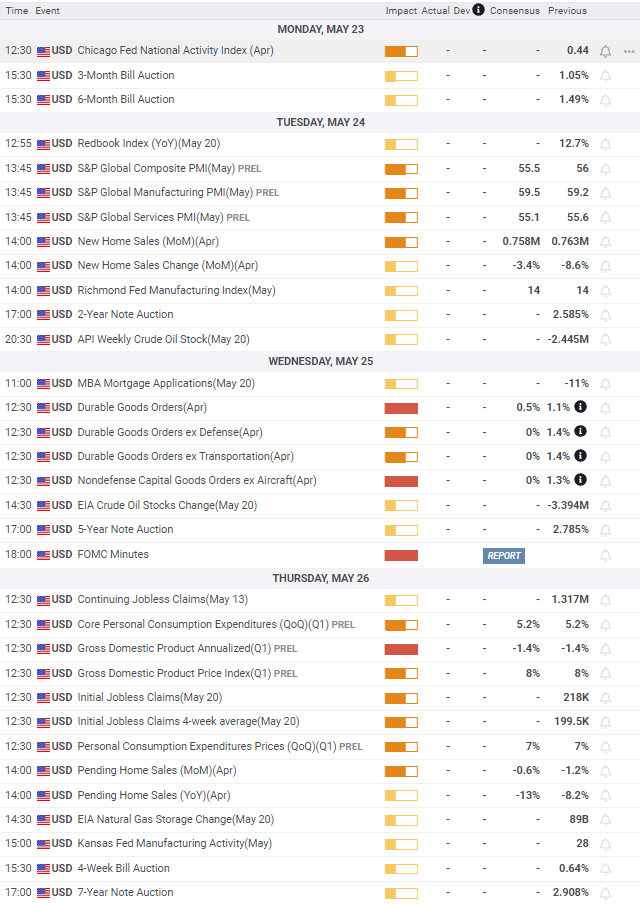

In the US, Durable Goods Orders for April should repeat the positive Retail Sales information. First quarter GDP receives its first revision, any surprise here could impact markets, large adjustments are rare but they do happen. Personal Spending for April will be interesting as the Bureau of Economic Analysis authors a real spending series with the figures corrected for inflation. It is not widely covered but will be far more telling for the state of the consumer and the economy than the nominal numbers of retail sales.

The outlook for the USD/JPY is lower as profit-taking competes with waning fundamental factors.

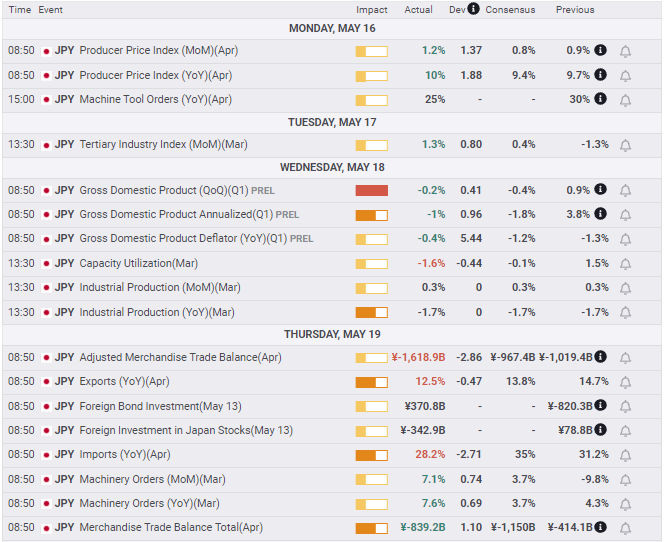

Japan statistics May 16-May 20

US statistics May 16–May 20

FXStreet

Japan statistics May 23–May 27

FXStreet

US statistics May 23–May 27

FXStreet

USD/JPY techincal outlook

tech 1-637886611688215746.png)

The widening divergence of the price line beneath the signal line in the MACD (Moving Average Convergence Divergence) is a negative for the USD/JPY. Likewise the descent of the Relative Strength Index (RSI) from overbought status at 77 in late April and 68 on May 6 to 49 on Friday while the USD/JPY has retained the majority of its Match to May gains, indicates likely losses ahead. Average True Range (ATR) registered the high possibility of volatility in traversing the range down to 125.00. The turn in the 21-day moving average (MA) is also a sign that short-term momentum has shifted lower.

tech 2-637886611896133802.png)

Resistance: 128.40, 129.00, 129.50, 130.00, 130.60

Support: 127.25, 127.00, 126.45, 125.85. 125.40

Moving Averages: 21-day 129.23, 50-day 125.68, 100-day 120.41, 200-day 116.44

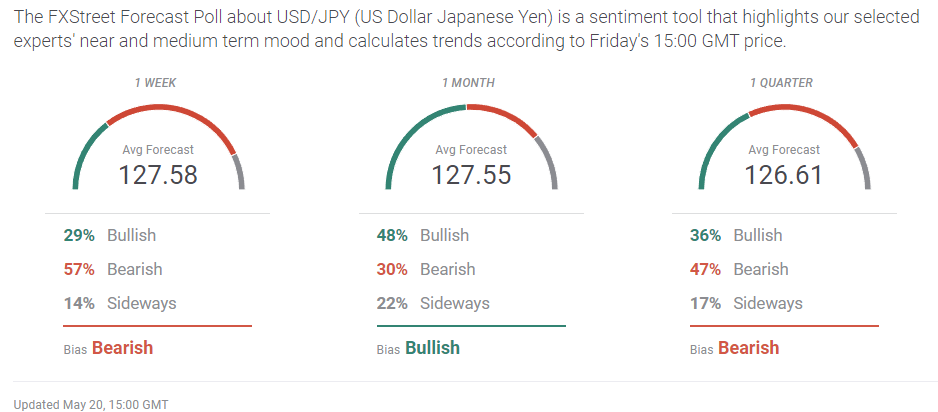

FXStreet Forecast Poll

The FXStreet Forecast Poll expects consolidation below 128.00 for the next month with a negative prognosis out to the quarter.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.