USD/JPY Weekly Forecast: US dollar remains the king of the safety-trade

- FOMC minutes point to taper momentum at the July meeting.

- Markets await possible clarification in Fed policy from this week's Jackson Hole symposium.

- Modest safety trade raises USD/JPY despite falling Treasury yields.

- Global risk-aversion moving currency markets to the US dollar.

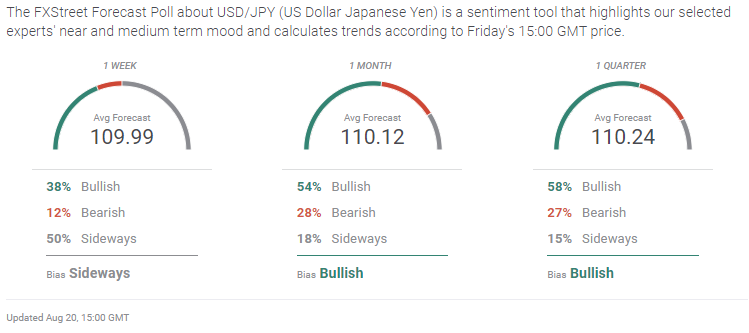

- FXStreet Forecast Poll sees USD/JPY gains out to one quarter.

The dollar churned higher this week propelled by the safe-haven trade and the confirmation that, as of its July 28 meeting, the Fed was intent on defining the terms of its long awaited bond taper. Questions about the direction of the US economy raised by the very weak July Retail Sales on Tuesday and last week’s plunge in August Consumer Sentiment will have to wait until more data is available.

Rising Covid-19 Delta cases in many US states, and countries around the world were the background and the logic behind the dollar’s gains. Except for Australia and New Zealand there were no new lockdowns but the assumption that the global economy is headed for weaker growth kept crude oil moving lower all week.

The Federal Reserve begins its annual three-day Jackson Hole symposium on Thursday August 26. Though the pending taper has been a much conjectured topic, in view of the recent economic data, Fed officials are likely to be reticent, leaving their options open in case US growth and job creation deteriorates.

The spectacle of the Biden administration's feckless withdrawal from Afghanistan, with an unknown number of Americans unaccounted for, and the country in the hands of the Taliban, added to the general unease on the international scene and, counterintuitively perhaps, assisted the dollar.

Treasury rates fell in the US as the credit market paid more attention to the economic data than the somewhat out-of-date Federal Open Market Committee (FOMC) minutes.

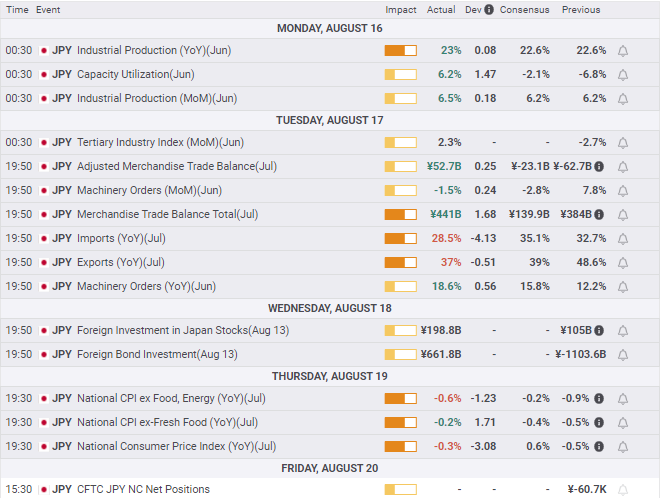

Japanese information was largely as expected without signaling any change in the economy. Industrial Production improved in June but not by a surprising amount. Import and Exports in July were the most telling statistics. Imports fell instead of rising as forecast and exports dropped more than expected, though both were large gainers on last year's figures. Neither indicate an accelerating economy. Deflation returned in July as National CPI was negative in all categories, the overall figure has been forecast to rise, and June's results were all revised steeply into the negative.

National CPI was positive for the second month in July, but after eight prior declines, and the core rate negative for the fourth month, deflation is still a major concern.

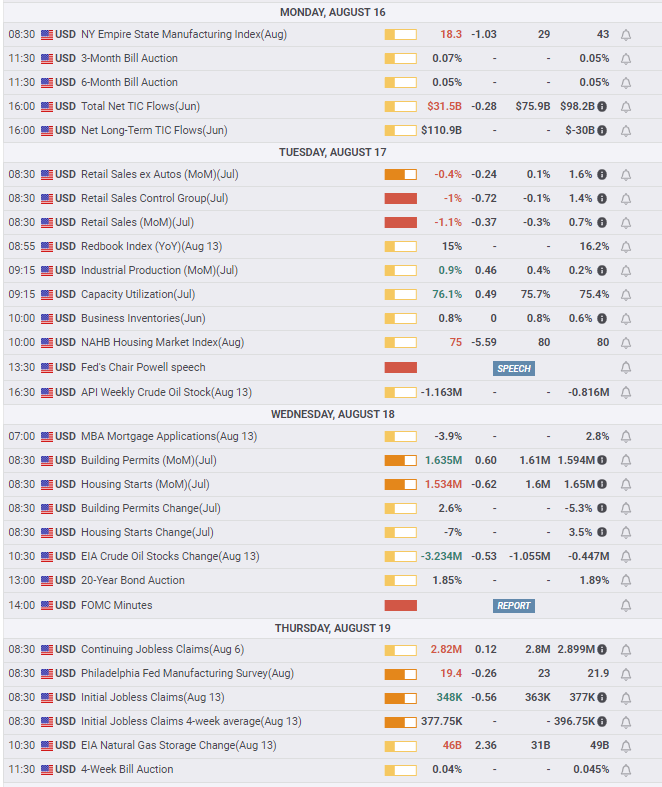

In the US, July Retail Sales were a major disappointment and after the sharp decline in Consumer Sentiment in August were a warning that inflation and the pandemic may be taking a toll on consumption. Industrial Production and Capacity Utilization were better than forecast and the home construction industry continued at a strong level. Initial Jobless Claims fell to a new pandemic low. In all, US data was consistent with an active economic recovery with a caveat on consumer spending that bears watching.

USD/JPY outlook

In the general flight to the US dollar this week the USD/JPY was the weakest performer rising modestly from its 109.60 open on Monday. In comparison, up to Friday’s open, the EUR/USD had lost more than a figure, and the sterling more than two. The USD/CAD was the big winner, rising almost four figures as crude oil fell to a three-month low.

Risk-aversion has been the motivator for currency markets with Covid-19 cases rising in the US and other countries and the botched American withdrawal from Afghanistan generating unease in capitals and markets around the world.

Treasury yields fell modestly on the week as the markets look to the Fed Jackson Hole symposium that begins on Thursday, August 26 for clues to monetary policy and the long-expected tapering of the Treasury bond program.

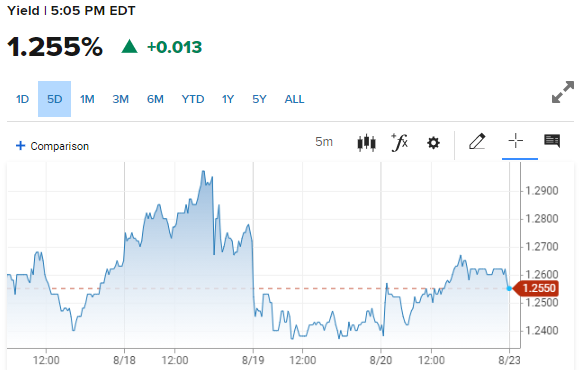

US 10-year Treasury yield

CNBC

The Japanese yen has historically served a secondary role, after the US dollar, as a safe-haven. Though that tendency has diminished in recent years, it is still evident in the stability of the USD/JPY despite the safety flows to the US dollar this week.

The upward pressure on the US dollar should bring the USD/JPY above 110.000 though the 109.00-110.50 range of the last six weeks is unlikely to be broken without further developments. Resistance at 110.50 is particularly strong having rejected numerous attempts to cross it.

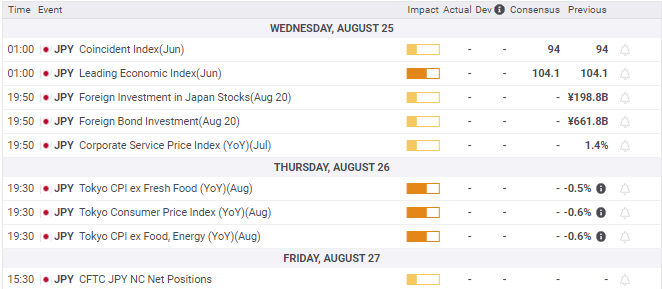

Japanese statistical focus will be on Tokyo CPI for August, especially after July's return to deflation in the national figures.

In the US, Durable Goods for July on Wednesday, should confirm the weakness in Retail Sales, and PCE Prices for July on Friday, the CPI results.

The Federal Reserve's annual Jackson Hole symposium, beginning on Thursday, is the main event. There is little market consensus over the tenor of possible remarks from Fed officials attending the conference. The gathering is not a Fed policy event and there are no official statements scheduled.

Japan statistics August 16–August 20

US statistics August 16–August 20

FXStreet

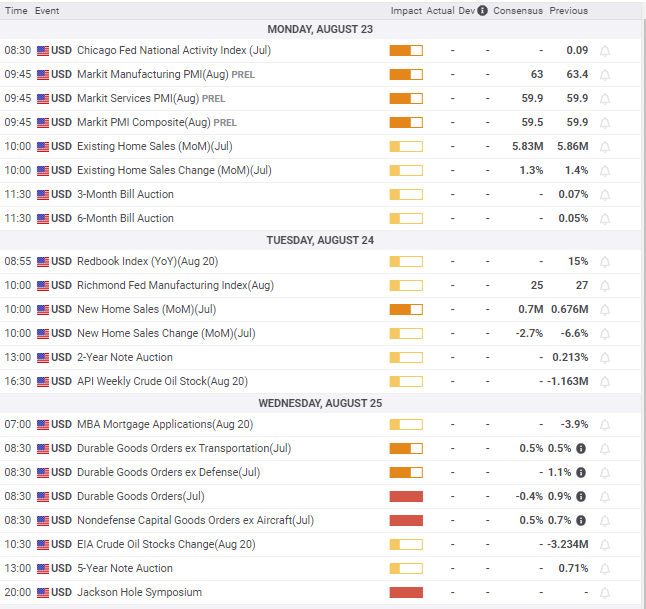

Japan statistics August 23–August 27

FXStreet

US statistics August 23–August 27

USD/JPY technical outlook

The six-week old channel between 109.00 and 110.50 dominates USD/JPY prospects. Its effect is evident in the MACD (Moving Average Convergence Divergence) and the Relative Strength Index (RSI) ending the week nearly neutral. True Range exhibits the lack of momentum, closing at its lowest point for the week.

-637650664852467278.png)

The clustering of three-of-four moving averages (MA) around the market level is a further indication of the balanced pulls on the USD/JPY. The 50-day MA at 110.18 marked the top on Thursday. The 21-day MA at 109.86 delineated the high on Friday and the 100-day MA at 109.65 nearly defined the low, 109.57. Only the resistance at 110.18 is likely to be of consequence. The averages at 109.86 and 109.65 are effective because the USD/JPY momentum is so weak.

-637650665033089946.png)

The bias in the USD/JPY is mildly higher mostly because of the overall dollar safety-trend in currencies, a tendency that could easily be trumped by Fed comments from Wyoming.

Support and resistance lines in close proximity and narrowly spaced are another residue of the recent stasis in the USD/JPY. Except for the range markers at 109.00 and 110.50, none are particularly strong and would fall to a concerted fundamentally based move.

Resistance: 109.86 (21-day MA) ,110.15, 110.18 (50-day MA), 110.30, 110.50, 110.70, 111.00

Support: 109.70, 109.65 (100-day MA), 109.50, 109.35, 109.00, 108.75

-637650673770967992.png)

FXStreet Forecast Poll

The FXStreet Forecast Poll's bullish outlook is restrained by technical impediments that will not stand if the global economic outlook worsens.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.