USD/JPY Price Forecast 2020: A journey from trade fears to high-stakes elections

- USD/JPY price is set to continue moving in response to US-Sino trade relations in 2020.

- The US Presidential elections will grow in importance as the year progresses.

- Central banks will likely attempt to step back, but may come under pressure to act.

- Iran and North Korea may impact the safe-haven yen as well.

“Bye bye bye” – N-Sync’s greatest hit from the 1990s can be used to say farewell’s the 21st century’s second decade. The global economy is in-sync once again – but political uncertainty remains elevated and will likely be enhanced in 2020.

2019 was dominated by trade talks as the primary driver for the safe-haven Japanese yen while the Federal Reserve’s shift from raising rates to cutting them weighed on the US dollar. Nevertheless, brighter prospects for the US economy – despite external headwinds – kept the currency pair in check. It is ending the year at the 109 handle it kicked off the year, completed a 700-pip journey.

In 2020, central banks on both sides of the Pacific will likely try to stay in the shadows, with their success in doing so depending on the government. The fate of global commerce will likely remain high on the agenda, but gradually make way for another political drama – the US Presidential elections.

USD/JPY Price Analysis 2019 – a year of better synchronization, trade drama

Fed reverses course

Jerome Powell, Chairman of the Federal Reserve, will remember 2019 as the year he reversed policy – cutting interest rates for the first time since 2008. At the beginning of the year, the Fed’s projection of future interest rates was still showing higher borrowing costs. Yet already in January, Powell signaled his reluctance to take the path of hiking rates. He then moved to sit on the fence in March, and by June, the Chairman already opened the door to cutting rates.

What caused the dovish shift? The Fed’s higher rates seemed to choke the domestic housing market early and inflation was nowhere to be seen. And while wage growth accelerated and surpassed the 3% mark in annual terms, there seemed to be no imminent need to stay ahead of raging price rises.

The historic cut came in July and while Powell’s message was mixed, he followed through by overseeing two more reductions later on. The “mid-cycle adjustment” ended with three cuts. For dollar/yen, lower rates somewhat weighed on the dollar, but also allowed the global economy – dependent on the greenback – to lift its head The Fed’s willingness to act by cutting rates and also ending its Quantitative Tightening program helped support global markets and diminished demand for the safe-haven yen. US real-estate also recovered. While the business cycle is now more in-sync all over the world, America leads to global growth.

The Washington-based institution’s moves were accompanied by dissent and criticism, but by year-end, the decision to sit on the fence and wait for more data was already accepted in harmony. Even President Donald Trump – who vehemently criticized the bank throughout the year – seemed to moderate his tone.

Deal or no deal?

Trump’s trade war with China has also reached a calm of sorts, but developments during the year were far more erratic and caused jitters. USD/JPY was often whipsawed on trade headlines.

While negotiators from the world’s largest economies failed to meet the early March deadline, reports were optimistic until early May, when China had second thoughts about certain aspects of the deal. Washington slapped Beijing with new tariffs and relations remained sour for around two months. During June, Powell cited uncertainty coming from commerce as one of the main drivers of opening the door to rate cuts. Trump met his Chinese counterpart Xi Jinping in late June and both leaders agreed on a trade truce.

New negotiations held only until mid-August when talks broke down and Trump announced substantially higher levies from September – only to regret some of them and push them back to December. As autumn leaves were falling, the economic giants agreed to settle for an accord in two phases, with Phase One serving as a platform for reducing tensions.

Despite upbeat comments, a deal was reached only at the last moment, and at the time of writing, its details are uncertain. Overall, it seems easier to agree on Chinese buying of US agrifoods and the removal of tariffs, but harder to come to terms with structural changes in China. Moreover, Beijing is angered by Washington’s criticism of its actions in Hong Kong and Xinjiang. And the most significant development is that both countries have begun to gradually move away from dependence on each other – the Great Decoupling – a topic that may rise to higher prominence in 2020.

Politics: From Nothing-burger to impeachment

In the US political scene, the Democrat-led House of Representatives moved forward with impeaching Trump – yet not in relation to Russian connections in the 2016 elections. Robert Mueller, the former FBI Director who was appointed Special Counsel, filed his report in which he said there was no collusion between the Trump campaign and Russia. However, he stated that his findings do not exonerate the president. A redacted version was made public and for Nancy Pelosi, the House Speaker, it was insufficient to move forward with impeachment.

Things changed in the summer when the Ukraine scandal broke out. Trump allegedly pressed the eastern European nation to dig up dirt on rival Joe Biden – even withholding vital military aid for this domestic political need. Pelosi pushed forward with an impeachment inquiry which convinced a small majority of Americans to support the investigation, but most Republicans remained loyal to their standard-bearer. The administration did not cooperate with the move that Trump labeled as a “witch hunt.” At the time of writing, the House is set to impeach the president but the Senate is highly unlikely to remove him from office.

USD/JPY and broader markets, which prefer stability, mostly shrugged off the drama, but politics will likely have a more significant role in 2020.

No drama in Japan, little impact from geopolitics

When reviewing dollar/yen in 2019, the focus is on the US. The Bank of Japan left its interest rate unchanged at -0.10% throughout the year and only made minor tweaks – pledging to hold borrowing costs at low levels for as much as needed. Haruhiko Kuroda, Governor of the BOJ, held the door open to doing more but seemed to have no new tools. The current negative rates already hurt banks’ profits and have done little to lift meager inflation. Close to year-end, the government laid down plans for fiscal stimulus, a move that may come to the forefront in 2020.

The safe-haven yen did react – albeit only temporarily – to flareups in the Middle East. An attack, perhaps by Iran, on Saudi oil installations, sent investors to the Japanese currency as oil priced leaped. Protests have rocked several countries in the oil-producing region but have failed to make their mark.

More surprisingly, deteriorating relations between the US and North Korea have failed to move the yen in the past. Negotiations on denuclearization remained stuck and the Pyongyang has resumed its missile tests and upped its rhetoric. Kim Jong-un, North Korea’s dictator seems willing to confront America once again. This geopolitical issue may have a greater impact on markets in 2020.

2020 - Trade to fade out, presidential elections to fade in

“Nothing happens on New Year’s Day” sang U2 and that may be relevant for the first months of 2020, but not the latter half.

Trade - Implementation is key

Sino-American relations will likely continue moving markets early in the year. Financial markets will likely seek assurances that the world’s largest economies are not on course to any deterioration.

Back in 2018, Trump tweeted that he is “tariff man” and that continues echoing. Most Americans justify his efforts to confront China on forced transfer of technology, intellectual property rights and its significance as a rising power. The world’s second-largest economy has moved away from basic manufacturing and now rivals America also in advanced fields such as artificial intelligence. Moreover, the People’s Liberation Army has strengthened and its maneuvers in the South China Sea are worrying the surrounding nations and the US.

And while many also support Trump’s means of dealing with China – tariffs on the flood of Chinese goods – markets find the erratic nature of these moves unnerving.

USD/JPY may have room to rise if no new levies are imposed during the year, and could even rise further if previous ones are removed. Yet most importantly, having a dose of certainty would help businesses return to healthy investment, taking the burden of growth off consumers’ shoulders.

Implementation of the Phase One accord is critical to stability early in the year. China has committed to buying American goods on a vast scale. The US has practically given up on trying to turn its rival into a market economy but only seems to seek Beijing to favor American goods.

As long as the implementation is smooth and nothing moves on the tariffs’ front, markets have room to rise, carrying dollar/yen with them. As the elections draw near, Trump will likely refrain from rocking the boat. Investors are unlikely to expect a broader “Phase Two” accord or any serious talks toward a wider deal before 2021.

However, markets will watch the Great Decoupling with concern. Signs that the world’s largest economies are moving away from each other may come in various forms. Monthly trade balance figures that show reduced trade may move USD/JPY to the downside.

Huawei – China’s controversial telecommunications giant – has already moved to free itself from its dependence on US providers following its stint in the spotlight and allegations of spying. US companies have looked to Vietnam for some supplies instead of China and may find other sources. If such interdependency is diminished, global growth could suffer in 2020. For the longer term, a lack of commercial dependency may push countries from a trade war to a real war – but that is improbable in 2020.

The more likely scenario is that the US and China maintain the current truce but gradually move away from each other rather than advance to a broader trade deal.

Fed: Seizing the sidelines at first

The Federal Reserve will likely stick to its neutral stance early in the year. The current rate is appropriate – as the Fed says – for Americans to continue shopping and for the housing market

Student debt is growing and remains a worry for policymakers, but while the issue may arise in importance around the elections, its size is not a threat to the US economy. The same applies to car loans. Clunkers have become endangered species in America, and consumers have piled up debt. Nevertheless, the scale is far from worrying. Mortgages comprise the vast majority of consumer debt, and they are likely to remain in control beyond 2020.

However, the Fed may find itself concerned about corporate debt. Long-term cheap lending rates have pushed companies to accumulate loans, with a significant chunk going to stock buyback – and not enough moving to investment. While data from late 2019 showed an increase in expenditure, companies’ activities could become a more substantial worry in 2020.

Should the Fed lower interest rates to ease the debt burden on firms and encourage investment? Or should it acknowledge that companies are investing in pushing the share prices higher and refrain from cutting rates?

Powell clarified that the bar for raising rates is higher than for lowering them, so firms with liabilities have little to worry about in 2020, but things may change later on.

Fed: Pressures resulting in QE in the second half?

The central bank may sail through the beginning of the year easily, but in addition to worrying about corporate debt, it may come under political pressure. Should the economy slow down, President Donald Trump could elevate his criticism against the bank and demand rate cuts. That would help his reelection chances. While Powell will likely resist and keep rates unchanged, he may be ready to resume the Federal Reserve’s bond-buying scheme.

The bank began squeezing its balance sheet in late 2017 in what Janet Yellen – then-Fed Chair – called “watching paint dry.” As part of the reversing course in 2019, Powell stopped this process of Quantitative Tightening and Fed now maintains its portfolio balanced. However, jitters in money markets have already pushed the central bank to intervene and supply liquidity.

While that does not constitute QE, additional jumps of the repo rate may cause second thoughts. If the Washington-based institution kicks off “QE4”, the dollar may plunge across the board, but perhaps not against the safe-haven yen.

A second term for Trump?

Americans go to the polls only in November, but electioneering is already in full swing. Trump’s alleged attempt to obtain dirt on rival Joe Biden began well over a year before the elections – and the former VP’s chances of winning are far from certain.

The impeachment trial in the Senate will likely kick off the year, but Senate Republicans are set for a swift procedure, ending in an acquittal. The president is ousted only if two-thirds of upper house members vote to remove him. The opposition Democratic party has only 47 out of 100 seats, so no fewer than 20 senators from the president’s party are needed – and having even one dissenter, such as Mitt Romney, will be news.

While traders will likely be fascinated by the political drama, markets will likely remain stable. The process will likely end in January or February, with the focus remaining on the Democratic primaries – learning who Trump’s challenger will be.

The opposition party is divided between the centrist flank – which markets prefer – and the left-leaning one. USD/JPY would likely rise if one of the moderates advances in the long contest and would fall if one of the populists makes headways.

Among the centrists, Biden is the top contender on the national level and would seem like a safe pair of hands. However, the aging politician is prone to gaffes and is lagging behind in funding. Pete Buttigieg, from Southbend, Indiana, is a rising star in the first state to hold a competition – Iowa. If he wins the caucuses in the Hawkeye State, he may enjoy momentum in polls – and in donations.

Another centrist that has no funding issues is Michael Bloomberg, former mayor of New York. The billionaire businessman decided to skip the initial primaries and caucuses and go directly fro the big prize – “Super Tuesday” – a long list of contests held in early March. As an outsider and a late entrant, Bloomberg’s chances are considered slim.

If any of these three take the lead, USD/JPY has room to rise.

On the left-leaning wing, senators Elisabeth Warren and Bernie Sanders stand out. Warren topped some national polls and competes for head to head with Biden. As a champion of consumers’ financial rights and sometimes seen as a “warrior” against banks, investors fear her. She laid out detailed healthcare plans which were criticized for being expensive. If her lead in polls turns into one in delegates, USD/JPY has room to fall.

Bernie Sanders is competing with her and is trailing behind. His run in 2016 pushed the party to the left and despite his age and health issues, he received an endorsement from Alexandra Ocasio Cortez (AOC), the young rising star at the party. While Sanders’ chances are slim, he may be pivotal to markets if he quits the race and throws his weight behind Warren.

Initial indications to who will confront Trump are expected in February, with a clear picture in March. If the race remains wide open, every additional contest throughout April, May, and June will move markets. Each state elects delegates who are divided proportionally according to voting. That may lengthen the process.

By June, a clear winner will emerge and the focus will shift to national polls. If Warren or Sanders are nominated, markets will likely favor Trump. Yet if Buttigieg or Biden win, investors would likely prefer the Democrats. A mostly market-friendly president with no plans for an erratic trade war is what markets could best hope for.

The main parties hold their conferences during the summer, where they will share ideas about their policies. That could also sharpen investors’ minds. A Democrat moderate may move to the left to appease the losing side in the primaries and bring the party together. A left-leaning leader may water down some of the more radical ideas in order to appeal to the center. However, the winner may also opt to move to their direction rather than ease their stance.

The Republican Party’s conference will likely be of less interest, as Trump’s record in power speaks for itself. That includes business-friendly tax cuts but unfriendly erratic trade wars.

Most Americans tune into the elections after Labor Day in September, and that is when national and battleground state polls may rock markets. Closer to the finish line, Senate races may also be of high interest. If Warren is the Democratic nominee but Republicans are on course to win the Senate, any radical proposal may be blocked. A disunited government may, therefore, moderate market movements.

Japan: Monetary threats and real fiscal action

The Bank of Japan is unlikely to move, but would probably like to keep on waving its stick and threaten more action. That may help in keeping the yen from revaluation – at least as long as markets believe it and do not see it as the boy who cried wolf.

And while the BOJ is likely to stay on the sidelines, the actions of the government may move the currency. Prime Minister Shinzo Abe announced another stimulus package in late 2019 and its implementation may boost the economy – and perhaps even inflation. That may inadvertently strengthen the yen.

And if economic growth remains tepid, Abe – who has significant power – may introduce another plan. Conversely, he may finally take more than baby steps with the “third arrow of Abenomics” – structural reforms. Monetary and fiscal stimuli have probably run their road. Japan has pioneered QE and may find itself once again at the forefront of economic innovation with new policies, perhaps already in 2020.

Geopolitics: North Korea first, Middle East later?

Worsening relations between North Korea and the US have been ignored by markets, but if the rogue regime conducts new missile and nuclear tests, the world may listen. The safe-haven yen will likely jump if fears rise – even if Japan is in Pyongyang’s firing line. The next escalation may come early in the year.

However, President Trump may try to avoid a full-blown crisis that will endanger his reelection chances. He sees the detente with North Korea as one of his achievements and is unlikely to let that fall apart. If Washington steers toward a quick resolution, the issue may only have a temporary impact. However, Kim Jong-un is aware of the political calendar and may press America harder.

The Middle East’s issues are far from over. Iran has upped its military game and Saudi Arabia seems to have taken a step back. The Middle Eastern “cold war” may turn hot if simmering discontent threatens the regimes in both countries and their allies. Oil-producing Algeria is also experiencing discontent and Libya remains a defunct state. If oil supply is reduced from these countries, the yen has room to rise.

Massive protests in Lebanon, Iraq, and Iran seem to be under control, but they may erupt again. If the Iranian regime or its allies in Iraq come under pressure, one way to divert attention from economic problems is to find an external enemy. If tensions result in the blockage of the Straits of Hormuz – where a substantial chunk of petrol flows to the world, safe-haven assets may leap.

Iran and the US seem reluctant to strike any new deal after the US pulled out of the JCPOA – the Iran nuclear deal – in 2018. Any concession from Trump to the nation with which his predecessor Barrack Obama got close to is unlikely. While nobody wants a war, a chain of uncontrollable events that leads to one cannot be ruled out.

Conclusion

Nobody has 20/20 vision for 2020, but assessing that US politics will grow in importance as the year progresses is a safe bet. Markets prefer a Democrats moderate or Trump over a left-leaning candidate. US-Sino relations will likely top the agenda early in the year with implementation and tariffs remaining the major market movers.

The Federal Reserve will do its best not to change interest rates and if economic growth continues at its current slow pace, there will be no need to succumb to political pressures and do so. However, resuming QE cannot be ruled out and corporate debt may turn into a growing worry.

The yen is set to remain the safe-haven of choice, with North Korea and a potential flare-up around Iran moving it in addition to global growth.

The big technical levels to watch

-637124434646158356.png)

In order to have a broad look at technical levels, the weekly chart comes in handy. Here are the levels to watch, from top to bottom:

114.60 capped USD/JPY in October 2018, November 2017, and also in May 2017 – making it a critical level of resistance. It is followed by 113.15, a peak in July 2018, and by 112.50, the 2019 high recorded in April.

111.75 worked as resistance and as support in mid-2017 and is followed by 110.90, the gap line from May 2019. The next line is 109.70, which provided support in March 2019 and also held dollar/yen down toward the end of the year. Moreover, it converges with the 100 and 200-week Simple Moving Averages.

108.50 provided support in late 2019 and worked as resistance around September. Another line from that time is 107.80 and it also held USD/JPY up in January. 106.50 was a support line in October.

105.75 is another support line dating back to September, and also in April. It is followed by 105, a psychologically significant level and also a support line from August, before the all-important 104.60 line. That final level worked as support in August 2019 and almost perfectly converges with the flash crash trough from January and a swing low from March 2018.

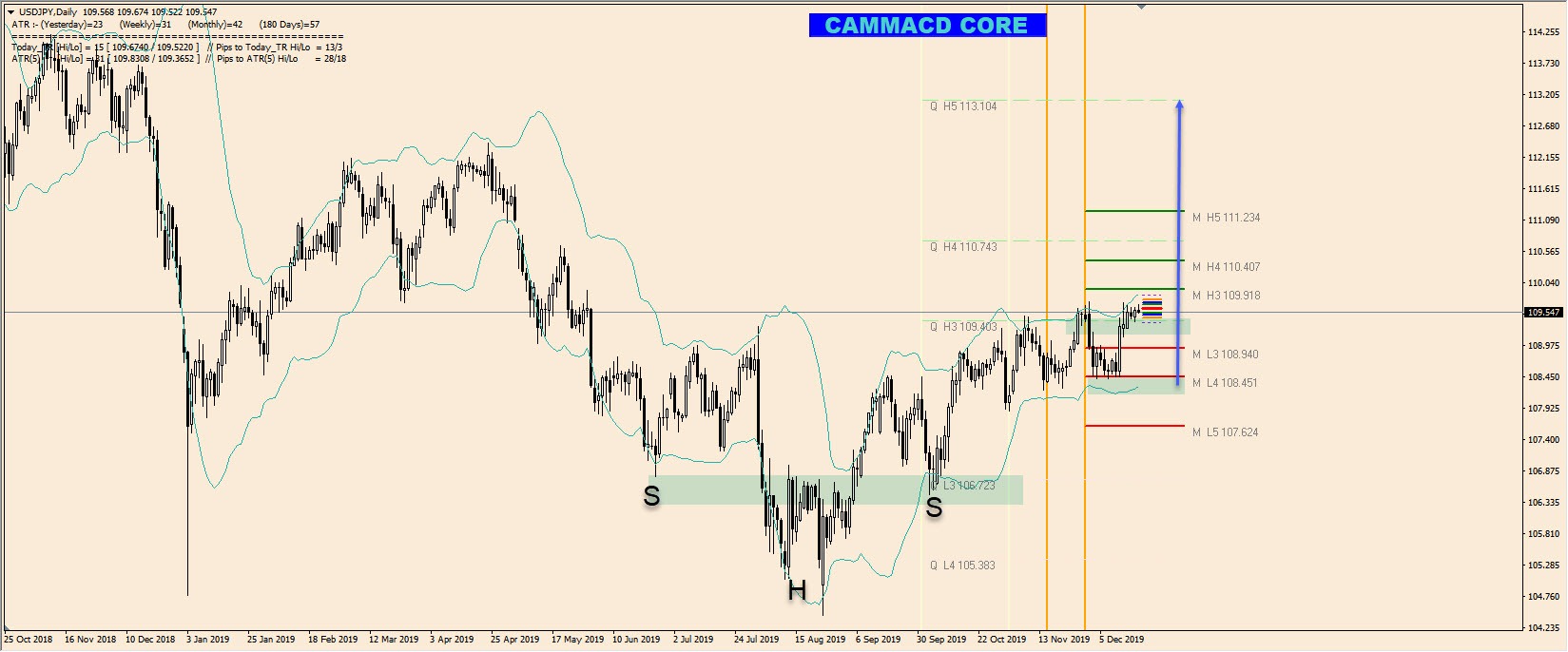

Nenad Kerkez provides his Camarilla Pivot Point Forecast seeing some bullish continuation with only a potential mid-term change later on the year:

USD/JPY Camarilla Pivot Point Forecast

The USD/JPY has formed a bullish SHS Pattern on the Daily TF. This is suggesting a further push up towards Q and M levels.

"Q" are Quarterly Camarilla Pivots and "M" are Monthly Camarilla Pivots. We need to use both if we apply the analysis on the Daily timeframe. Green highlight shows possible bounce spots and I expect bullish continuation from any of those zones. Targets are 110.74 and 111.23 followed by 113.10. Have in mind that the ATR(5) is app 32 pips per day so this accounts to a mid-term analysis. It might take some time for the price to get there, but the overall picture is bullish.

Only below Q L4 105.38, we will see a mid-term trend change. Camarilla Quarterly pivots change once in 3 months while monthly pivots change once in a month.

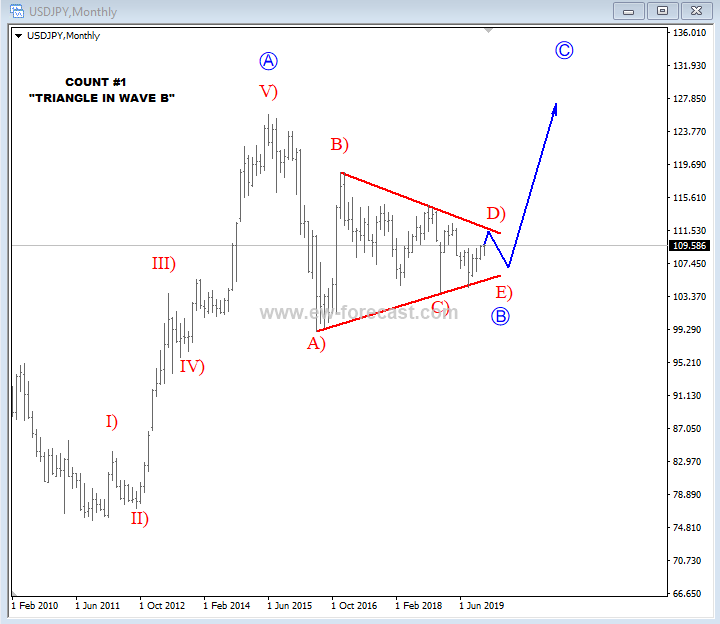

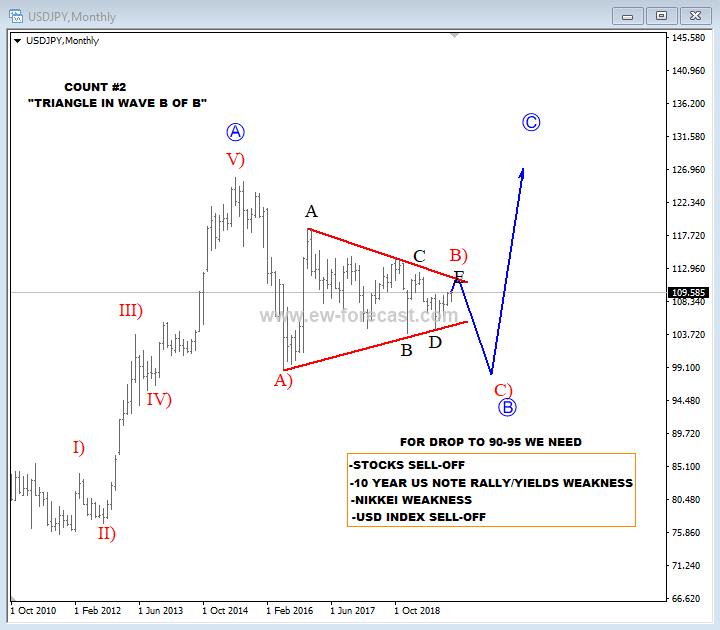

Gregor Horvat sees potential bullish waves on both of his Elliott Wave counts:

USD/JPY Elliot Wave Analysis (count 1 and 2)

USDJPY is trading sideways for 4 years which more and more looks like a triangle formation. Well, at this stage we are observing 2 counts; as a primary count we are tracking a bullish triangle in wave B that can still take some time, at least in the 1st quarter of 2020 to fully complete the final wave E) before a break out higher back to highs for wave C. But, in case of US Dollar and stock market sell-off, while bond market may rally in 2020, we also have to consider even a potential bearish triangle in wave B) of B that can push the price below 100 level to complete a corrective decline from the highs before the real bull run for wave C shows up.

Forecast Poll 2020

| Forecast | H1 - Jun 30th | H2 - Dec 31st |

|---|---|---|

| Bullish | 32.6% | 21.4% |

| Bearish | 58.1% | 64.3% |

| Sideways | 9.3% | 14.3% |

| Average Forecast Price | 108.68 | 107.31 |

| EXPERTS | H1 - Jun 30th | H2 - Dec 31st |

|---|---|---|

| Alexander Douedari | 106.00 Bearish | 106.00 Bearish |

| Andrew Lockwood | 113.00 Bullish | 115.00 Bullish |

| Andrew Pancholi | 114.40 Bullish | 111.48 Bullish |

| ANZ FX Strategy Team | 112.00 Bullish | 112.00 Bullish |

| Brad Alexander | 111.00 Bullish | 114.00 Bullish |

| BBVA Bancomer Team | 110.00 Sideways | 108.00 Bearish |

| BMO Capital Markets | 107.33 Bearish | 105.33 Bearish |

| BNP Paribas Team | 103.33 Bearish | 103.00 Bearish |

| BoA FX, Rates and Commodities Team | 108.00 Bearish | 103.67 Bearish |

| Chris Svorcik | 107.00 Bearish | 117.50 Bullish |

| Chris Weston | 107.00 Bearish | 104.00 Bearish |

| Christina Parthenidou | 112.50 Bullish | 109.30 Sideways |

| CIBC World Markets Team | 103.67 Bearish | 100.33 Bearish |

| CitiFX | 105.33 Bearish | 101.67 Bearish |

| Danske Research Team | 109.00 Sideways | 110.00 Sideways |

| Dmitriy Gurkovskiy | 125.00 Bullish | 135.00 Bullish |

| Dukascopy Bank Team | 105.00 Bearish | 102.00 Bearish |

| Eagle FX Team | 100.00 Bearish | 90.00 Bearish |

| ForexGDP Team | 115.00 Bullish | 102.00 Bearish |

| FX Trading Revolution Team | 107.00 Bearish | 108.00 Bearish |

| Goldman Sachs Global Investment Team | 107.00 Bearish | 105.00 Bearish |

| Gregor Horvat | 107.00 Bearish | 111.00 Bullish |

| ING Global Economics Team | 108.00 Bearish | 108.00 Bearish |

| Ipek Ozkardeskaya | 108.00 Bearish | 106.00 Bearish |

| Jamie Saettele | 105.00 Bearish | 100.00 Bearish |

| Jeff Langin | 113.50 Bullish | 109.00 Sideways |

| Jose Blasco | 111.00 Bullish | 108.00 Bearish |

| LMAX Exchange Team | 102.00 Bearish | 100.00 Bearish |

| NAB Global Market Research Team | 109.00 Sideways | 109.33 Sideways |

| National Bank of Canada Eco. & Strat. Team | 112.67 Bullish | 108.67 Sideways |

| Nenad Kerkez | 113.10 Bullish | 118.30 Bullish |

| OctaFx Analyst Team | 112.00 Bullish | 104.40 Bearish |

| Rabobank Financial Markets Research Team | 105.00 Bearish | 104.00 Bearish |

| RBC Economic Research Team | 112.00 Bullish | 110.00 Sideways |

| Societe Generale Analyst Team | 102.00 Bearish | 98.00 Bearish |

| Stelios Kontogoulas | 108.00 Bearish | 105.00 Bearish |

| Stephen Innes | 105.00 Bearish | 103.00 Bearish |

| TD Securities Research Team | 106.00 Bearish | 105.00 Bearish |

| Tomasz Wisniewski | 112.00 Bullish | 114.30 Bullish |

| UniCredit Research Team | 109.00 Sideways | 105.00 Bearish |

| UOB Group Team | 106.33 Bearish | - |

| Wells Fargo Research Team | 106.00 Bearish | 104.00 Bearish |

| Westpac Institutional Bank Team | 106.33 Bearish | 105.00 Bearish |

Risk on in Trump's election year will see a run on stocks and depress JPY. Higher bond yields to support USD.

US 10-year yields could fall to 1.25 % in 2020, so given the USD/JPY correlation to US yields, I expect USD/JPY to fall.

Related 2020 Forecast Articles

EUR/USD: Lean times soon to turn into flush times for euro dollar

GBP/USD: Pound may continue to fall on hard Brexit deadline

AUD/USD: May the aussie live in interesting times

USD/CAD: Canada and loonie are well positioned but not in control

Gold: XAU/USD bulls likely to remain in control

Crude Oil: WTI bulls to hold their horses despite tighter market, rosier economy

USD/INR: Domestic factors barely support a turnaround for Indian rupee

Bitcoin: BTC, the ultimate store of value

Ethereum: Calm on ETH/USD after the storm is over

Ripple's XRP: The glimpse of hope

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.