USD/CAD Weekly Forecast: The long decline ends

- USD/CAD breaks out of its 15-month descending channel.

- Fed economic, inflation and rate forecasts enliven markets.

- USD/CAD gains 2.3% on the week, best since March 2020.

- The FXStreet Forecast Poll predicts technical consolidation below 1.2400.

The USD/CAD had its best week since the pandemic panic last March sent the pair briefly above 1.4600.

In total, the USD/CAD added 2.3% from Monday to Friday, but the bulk of the move, 2%, came after the Federal Open Market Committee (FOMC) announcement on Wednesday.

The pair joined the general scamper to the US dollar in the aftermath of the Fed’s vastly improved prognosis for the US economy and tacit admission that dismantling the bond-purchase program is the next item on the policy agenda.

Resistance lines at 1.2265, 1.2315 and 1.2400 were easily traversed, and though the pair recoiled from 1.2480, the break of the 15-month pandemic down-channel on Wednesday was confirmed.

Contributing to the loonie decline has been a 4.2% drop in the Bloomberg Commodity Index (BCOM) since its June 10 high at 95.03. The index is ripe for profit-taking, having risen 15.7% this year and 51.1% since the lockdown bottom on April 19 last year at 60.24.

Most commodities are priced in US dollars, so as the dollar strengthens commodity prices fall per unit of value. The BCOM index is generally an early indicator of economic growth, rising in anticipation of an expansion and then temporizing or falling once growth is firmly underway.

MarketWatch

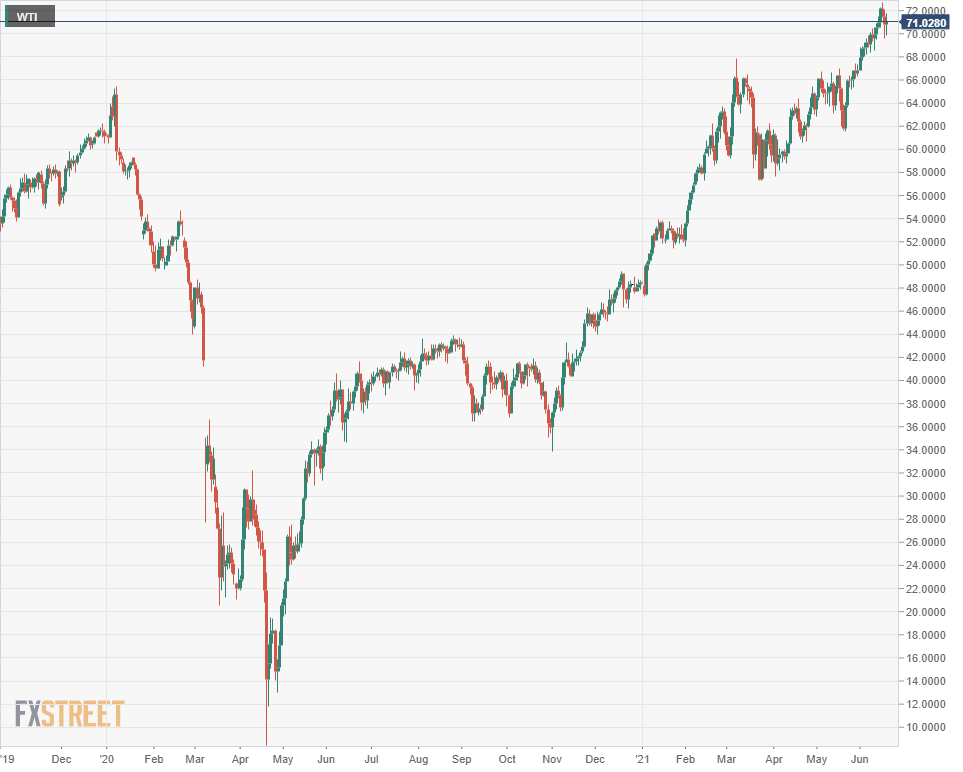

West Texas Intermediate (WTI) rose 0.6% on the week to $71.02 from Monday’s start at $70.58, despite the general increase in the dollar. The barrel price of WTI is up 47.6% from January 4 and 96.4% from its open on October 30 last year. Unlike most commodities whose product use cycle involves ordering far in advance, oil demand is closer to its more flexible supply, and prices tend to rise as an economic expansion proceeds.

The euro lost 131 points on the day, closing at 1.1995, its first finish below 1.2000 since April 16. The sterling, aussie and kiwi dropped to multi-week lows. The USD/CHF did the reverse, and the US dollar added to its gains on Thursday and Friday.

The lone exception to the dollar run was the USD/JPY which rose on Wednesday and then faded Thursday and Friday. The primary reason was that the dollar had already gained 6.7% this year against the yen while rising just 0.7% versus the euro, losing 3.4% against the sterling and 4.6% to the Canadian dollar.

The Fed’s acknowledgement of a strengthening US economy and inflation is a major policy shift, even if the timing may not be clear until the bank’s annual August conclave at Jackson Hole, Wyoming.

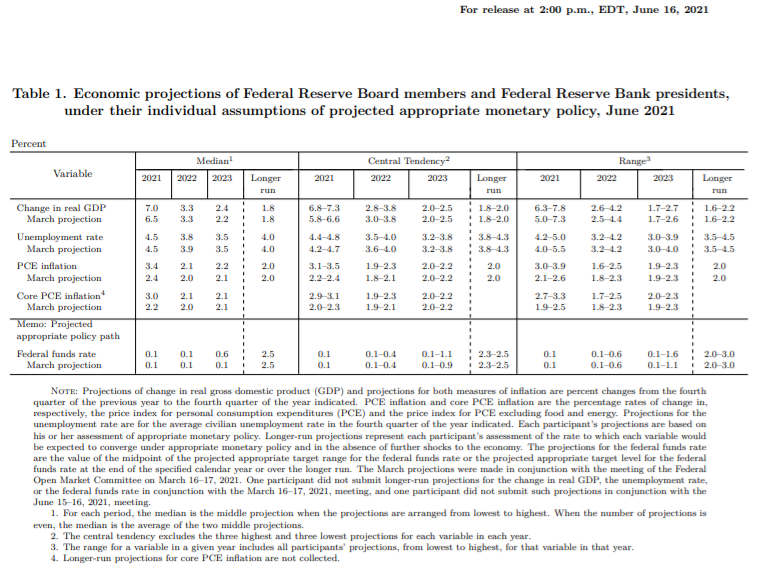

In the Fed's new Projection Materials, headline PCE inflation at the end of 2021 rose one percentage point to 3.4%. The core PCE rate that the Fed targets at 2% climbed to 3% from 2.2%. Economic growth in 2021 is now posited at 7% instead of 6.5%.

The estimate for the fed funds rate at the end of 2023, which had been unaltered in March at 0.1%, moved to 0.6%. Federal Reserve rate increases, unless under emergency conditions, come in increments of 0.25%, implying two hikes that year.

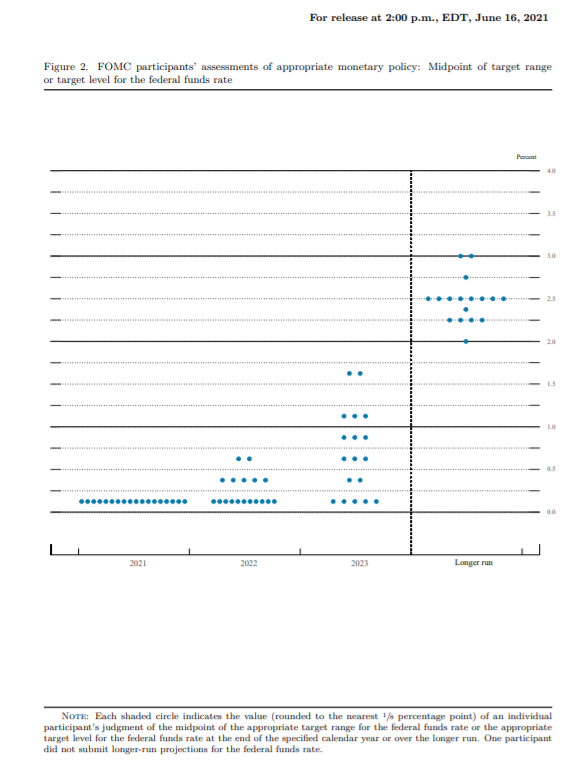

In the ‘dot plot’, which charts the individual projections of the FOMC participants, all 18 saw rates unchanged this year. In 2022, 11 members had rates remaining stable, five saw one hike, and two suggested two rate increases. For 2023 only five had rates unaltered, two members foresaw one hike, and three each had two, three and four increases.

Treasury rates rose sharply on Wednesday, with the 10-year yield adding 7 basis points to 1.569%. By Friday's close the 10-year return was at 1.44%, off 7 basis points on the day and its lowest yield since March 3.

US 10-year Treasury yield

CNBC

In another sign that the credit markets believe the Fed has changed policy, the yield on the 2-year Treasury closed at 0.205% on Wednesday, its highest in over a year and the first finish above 0.2%. Yield gains continued on Thursday with a 0.213% finish and a move to 0.254% on Friday.

CNBC

The short end of the yield curve, particularly the 2-year, had been the main focus of the Fed’s bond-buying program and had barely moved in over a year, while the 10-year return had climbed 83 basis points to 1.746% from December 31 to March 31.

American equities suffered their worst week since January as the prospects of higher rates moved from the theoretical to the factual.

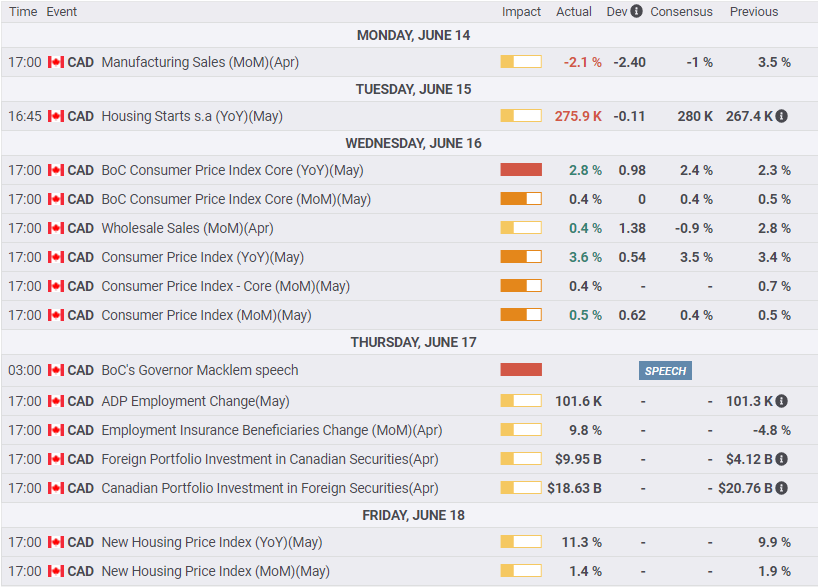

Canadian data was unexceptional. Housing Starts in May continued their strong performance. Consumer prices rose marginally in May, but annual rates were considerable below those in the US. There was no market impact.

In other economic data, US Retail Sales in May dropped 1.3% on a -0.8% forecast though the prior month was revised to 0.9% from flat. Industrial Production rose more than expected in May, but April’s gains faded to almost nothing. Initial Jobless Claims for the June 11 week rose unexpectedly above 400,000.

These statistics underlined the difficulty of providing accurate information quickly in the unusual circumstances of the current economy.

The Federal Reserve has changed its rate policy. It may take until the end of the summer for details and specific timing to emerge.

Currency adjustment will happen much faster.

USD/CAD outlook

Fundamental and technical prospects for the USD/CAD are again aligned, bias has clearly shifted higher.

The long decline is over, and the speed of the rise will largely be determined by the technical formations encountered. As the USD/CAD moves to the various resistance levels, the conditions for a stop-loss led short squeeze will repeatedly arise.

While the official announcement of a reduction in the Fed bond-buying program, let alone the complete end of intervention, may take until the end of the year or beyond, its practical impact has been immediate.

The rebound from resistance at 1.2480 on Friday will be repeated at different levels over the next weeks, but the upward direction of the USD/CAD is unlikely to change.

Economic data will play a small part in the week ahead.

Canada’s Retail Sales figures are for April and out-of-date. The US information from Durable Goods Orders and Personal Income and Spending are variations on prior releases. The Michigan Consumer Sentiment Index for June will be interesting but of no trading import. Initial Jobless Claims no longer move markets.

Canada’s economy remains under a series of limited lockdowns and the opening of the US border to tourist travel has been delayed until at least late July. The contrast to the wholly opened US economy may be as much of a psychological drag on the loonie as the actual economic restrictions.

Canada statistics June 14–June 18

US statistics June 14–June 18

FXStreet

Canada statistics June 21–June 25

FXStreet

US statistics June 21–June 25

USD/CAD technical outlook

Momentum indicators are strongly positive. The MACD, Relative Strength Index (RSI) and True Range are buy signals. The USD/CAD is almost two figures below the first (23.6%) Fibonacci level of the March 2020 to last week decline and the ascent to that level should come rapidly.

The 100-day moving average (MA) was crossed on Friday, which is another indicator of further gains. The 21-day MA has turned higher providing support just under the line at 1.2145.

Resistance: 1.2480, 1.2520, 1.2575, 1.2610, 1.2640, 1.2680

Support: 1.2400, 1.2315, 1.2265, 1.2145

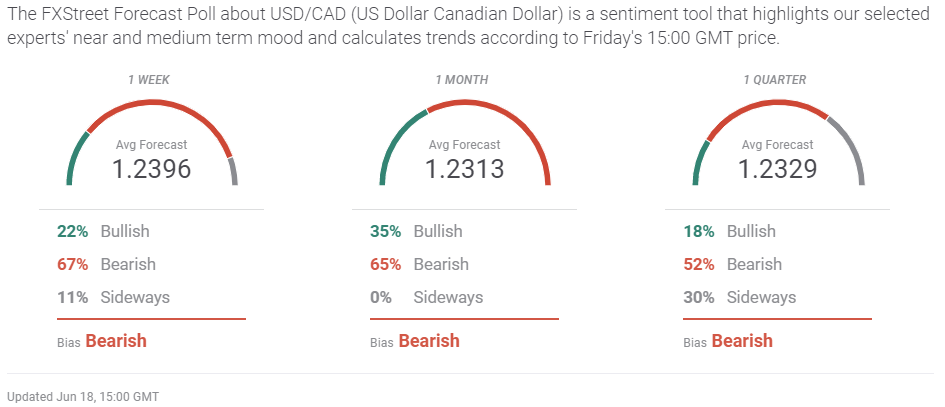

FXStreet Forecast Poll

The technical assessment of the FXStreet Forecast Poll ignores the fundamental change in the US dollar interest rate picture.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.