USD/CAD Weekly Forecast: Fundamental and technical alignment

- US Consumer Price Index drives Treasury rates and thedollar higher.

- WTI’s weekly close at $79.74 is the lowest since October 8.

- US-Canada 10-year bond spread narrows by 3 basis points.

- FXStreet Forecast Poll is positive for the USD/CAD.

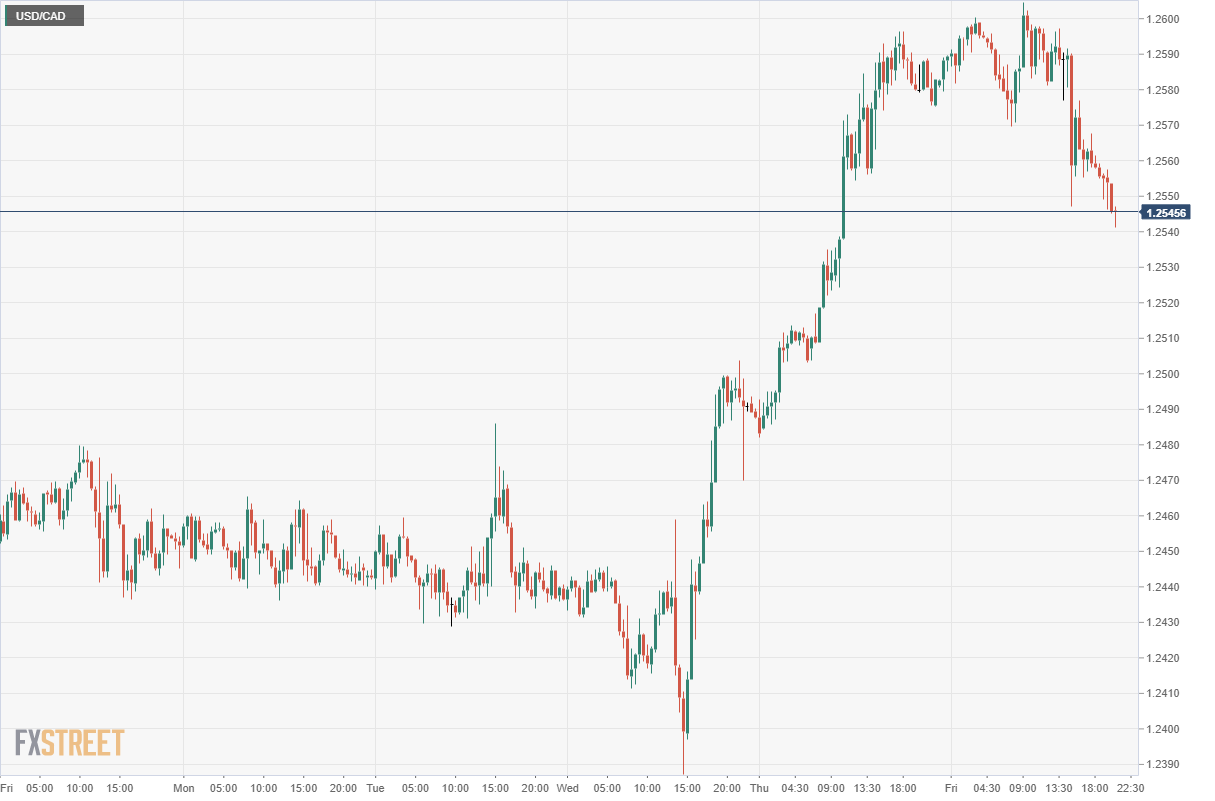

There was no place in the currency market to hide after Wednesday’s shocking vault in US inflation sent the greenback surging in every major pair. The USD/CAD closed at 1.2589 on Thursday and if it surrendered a modest amount on Friday it still finished at 1.2546, a four-week high.

American consumer prices soared 0.9% in October, more than double the 0.4% forecast and the 6.2% rate over the prior 12 months was the highest in 30 years.

Yields in the US Treasury market bolted after the release, gaining in every bond duration. The commercial benchmark 10-year Treasury added 11 basis points on Wednesday and another on Friday after Thursday’s Veterans Day closure, ending the week at 1.57%.

US 10-year Treasury yield

CNBC

Crude oil continued to wane, concluding its third weekly loss in a row at $79.74 and its lowest Friday finish since October 8

WTI weekly

American Treasury yields have returned to the center of the economic picture.

When the Federal Open Market Committee (FOMC) inaugurated its bond taper at the November 3 meeting with a $15 billion reduction in monthly purchases, only November and December were specified recipients. The continuation of the cuts into 2022 would, the FOMC statement said, depend on the progress of the US economy. Until recently that advancement had been defined by the labor market recovery.

Soaring inflation has reordered market priorities. The Federal Reserve’s policy goals can be expected to follow. The Consumer Price Index (CPI) has more than doubled in eight months from 2.6% in March to 6.2% as above.

The Fed’s elected inflation measure, the Core Personal Consumption Expenditure (PCE) Price Index, from the Bureau of Economic Analysis (BEA), a division of the Commerce Department, will not be issued until November 24. Due to its differing composition, the PCE has historically produced a lower overall inflation rate than the older CPI gauge.

There is no doubt that PCE will show the same acceleration in consumer prices as did CPI. The September PCE readings at 4.4% for the headline measure and 3.6% for core were already the highest on record for this series.

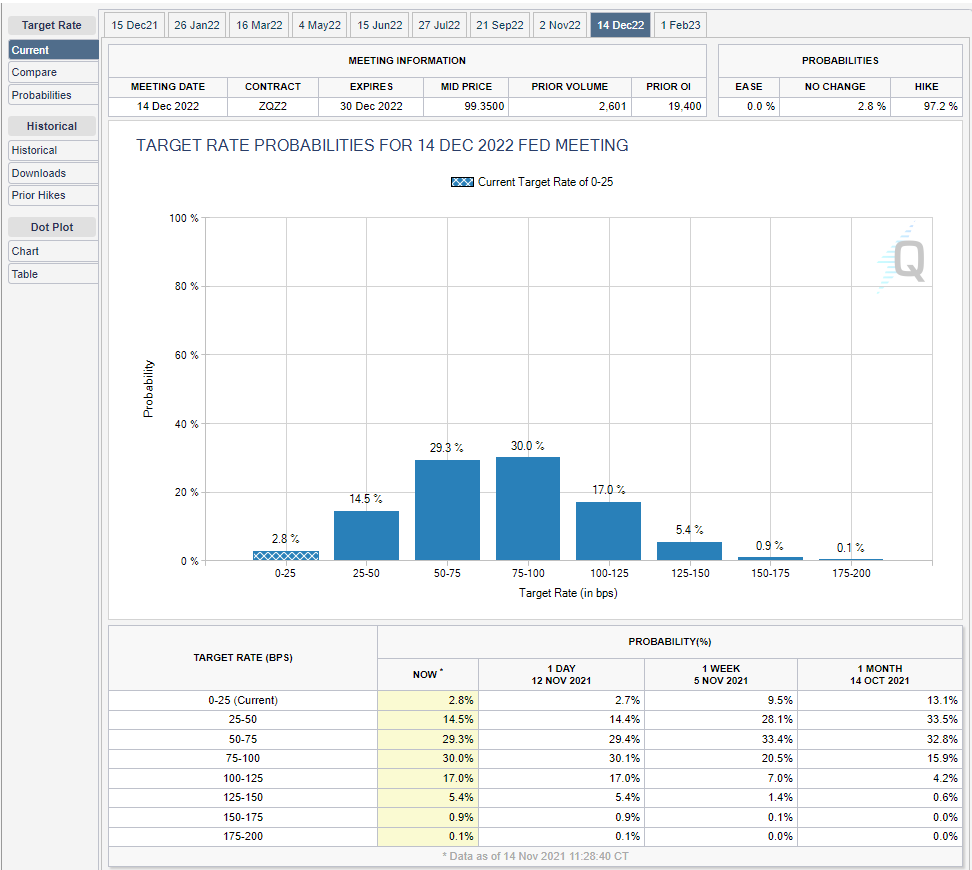

Credit markets have concluded that a 30-year high for inflation, with many more months of increases ahead, leaves the Fed with little policy choice. The Fed’s September Projection Materials predicted just one 0.25% fed funds increase next year. The Treasury market is far more aggressive. The Chicago Board Options Exchange, (CBOE) FedWatch Tool, based on fed funds futures, has one increase in June, one in September and one in December. It is quite likely that the Fed’s own updated estimates due at the December 15 FOMC will join the accelerated rate outlook.

CBOE

The rise in American Treasury yields narrowed the spread between the US 10-year return and its Canadian counterpart to 2.8 basis points on the week. The comparison finished at 1.570% for the US bond and 1.675% for Canada.

There was no Canadian economic data of note. Bank of Canada (BOC) Governor Tiff Macklem spoke at a virtual conference on diversity and inclusiveness organized jointly by the BOC, Federal Reserve, Bank of England and the European Central Bank. There was no market impact.

The US inflation data on Wednesday, as above, was the market driver. Not only was CPI at a three-decade high in October but PPI stayed at its own all-time records of 8.6% and 6.8% core in October, promising more consumer price increases in the months ahead.

Fading US consumer confidence intensifies the Fed's inflation dilemma

US Consumer Price Index: Falling real wages and the Fed's credibility problem

Initial Jobless Claims dropped to 267,000 in the first week of November, a level not far from the success of the second half of 2019 before the pandemic.

Consumer Sentiment in the Michigan Index fell to 66.8 in November, a 10-year low, from 71.7 in October. A rise to 72.4 had been forecast. Consumers hate inflation and rising prices add the threat of a sharp pullback in spending to the lengthening list of economic concerns.

The Job Openings and Labor Turnover Survey (JOLTS) maintained its near-record number of open positions in September. It is not the US job market that is depressing consumer attitudes.

American consumer prices rose at a 10.8% annualized rate in October. The Fed’s rhetorical assurances are now quite passe. Inflation is the central policy and market question.

USD/CAD outlook

The USD/CAD response to rising American interest rates and the general US dollar reaction will be the dominant theme as long as Treasury yields continue higher. The surge in Treasury yields in the first quarter, which saw the 10-year top-out at 1.746% on March 31 was undercut and reversed by two factors. First, the US recovery hit a number of rough spots in employment as the year progressed. Second, the Fed conducted a rhetorical campaign against higher Treasury rates, assuring markets that any inflation was transitory. The combination brought the 10-year yield back to 1.172% by August 2.

For the US economy labor market concerns have been overtaken by inflation. The Fed is likely to welcome the rise in Treasury yields as it constitutes a potential brake on inflation long before the central bank will be able to hike the fed funds rate, which at the moment, could not come before the second half of next year.

Inflation and its impact on consumer spending is a far greater threat to the economic recovery than rising interest rates.

Canadian CPI for October on Wednesday might bring the Bank of Canada back into the inflation fray, which could, potentially, negate some of the recent US sovereign rate gains. September’s Retail Sales will have little effect as US sales for October will already have been released.

Markets will focus on US Retail Sales for October on Tuesday. The consensus estimate is 0.7% as in September. Any weakness here, especially with the drop in November’s Consumer Sentiment, will add urgency to the Fed’s inflation fight and support US yields.

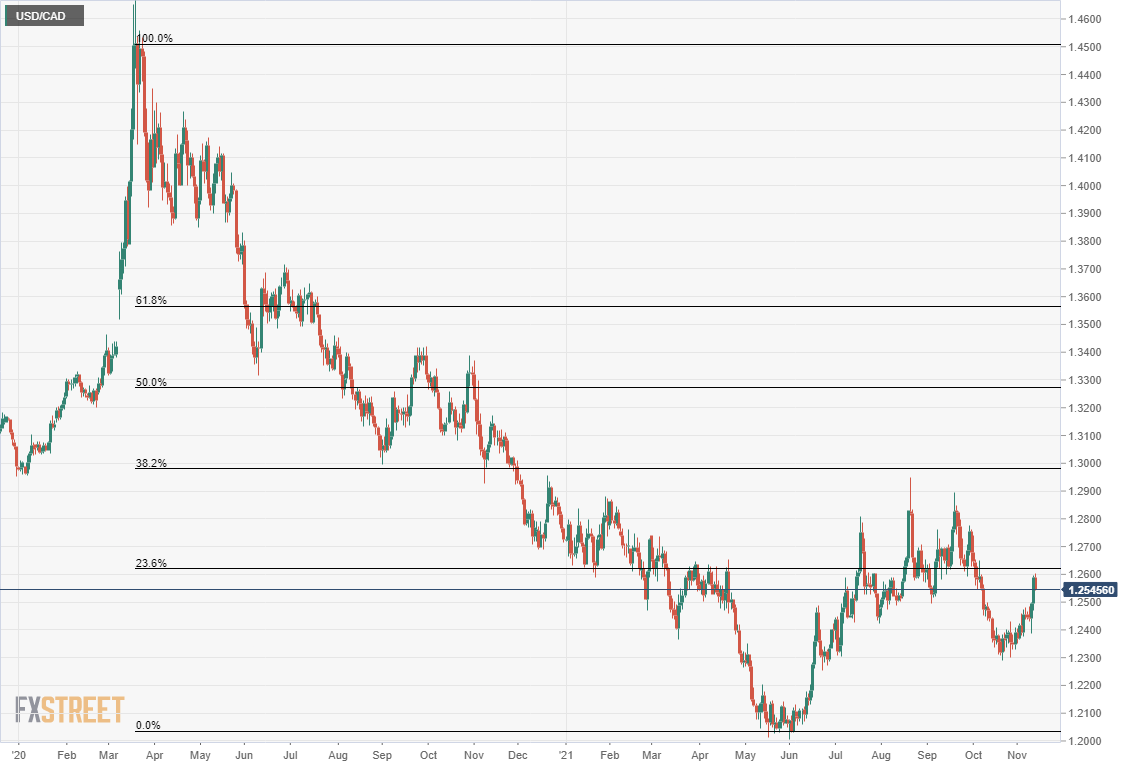

Technically, the rebound from the March 2020 to June 2021 decline has not taken place. The July to September bounce reached only the 23.6% Fibonacci retracement line and then retreated. Friday’s USD/CAD close at 1.2546 is below that first retracement at 1.2620. The second 38.2% line at 1.2981 is more than four figures distant.

Given the fundamental and technical situations, the bias in the USD/CAD is higher.

Canada statistics November 8–November 12

US statistics November 8–November 12

FXStreet

Canada November 15–November 19

US statistics November 15–November 19

USD/CAD Technical Outlook: Technical strength in the near-term

The MACD (Moving Average Convergence Divergence) signal line crossed the main line on October 29. That remains the buy alert, abetted by the increasing upward divergence of the main line from the signal line. The Relative Strength Index (RSI) positive aspect was not seriously affected by Friday's decline. It is also a purchase sign.

The 50-day moving average (MA) at 1.2539 and the 100-day MA at 1.2543 are a strong band of support just below Friday's close of 1.2546. The 200-day MA at 1.2474 and the 21-day at 1.2410 offer support at intervals beneath the current market.

Resistance: 1.2620 (23.6% Fibonacci), 1.2700, 1.2760, 1.2800

Support: 1.2540 (100-day MA 1.2543, 50-day MA 1.2539) 1.2475 (200-day MA 1.2474) 1.2410 ( 21-day MA), 1.2350, 1.2300

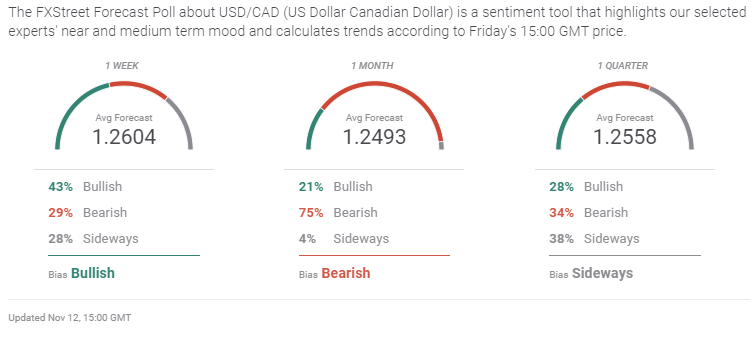

FXStreet Forecast Poll

The FXStreet Forecast Poll near-term view combines technical and fundamental support.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.