USD/CAD Price Forecast 2020: Canada and loonie are well positioned but not in control

- Canadian economy performed well despite slowing world and US growth.

- US-China trade war dominated business attitudes and USD/CAD price trading in the second half of 2019.

- The Bank of Canada's firm rate stance did little to benefit the loonie.

- A successful US-China trade deal will lift the Canadian economy.

The Canadian Dollar’s fortunes in 2019 were dominated by the trans-Pacific trade war between the United States and China, a dispute in which Canada’s resource economy has a large interest but virtually no say.

Presidents Trump and Xi have agreed on a phase-one trade deal that alters the discussion from antagonism to accommodation and aims to foster a relationship between the two economic titans that will lead to a more comprehensive arrangement in the future.

China will increase purchases of US agricultural goods and make structural changes to intellectual property and technology issues and Washington will forgo a scheduled 15% tariff on $160 billion in Chinese consumer goods and reduce other duties in phases. The agreement is expected to be signed by the two leaders in February.

The US-China trade deal joins Brexit, secured by Boris Johnson’s victory in the general election, and the United States-Mexico-Canada Agreement (USMCA), which Congressional Democrats have agreed to pass after delaying for a year, as developments having the potential to free the US and Canadian economies from the concerns that have crimped growth for the past year.

How the two economies respond to the political and trade improvements, particularly will the business sector resume investment, will go a long way to determining the economic outlook for the year. There should be sure indications by the end of the first quarter.

The Federal Reserve and the Bank of Canada are awaiting the data promising to be patient and if necessary to act as warranted.

Canadian economy in 2019

Except for a decline in business optimism, the Canadian economy performed well in 2019.

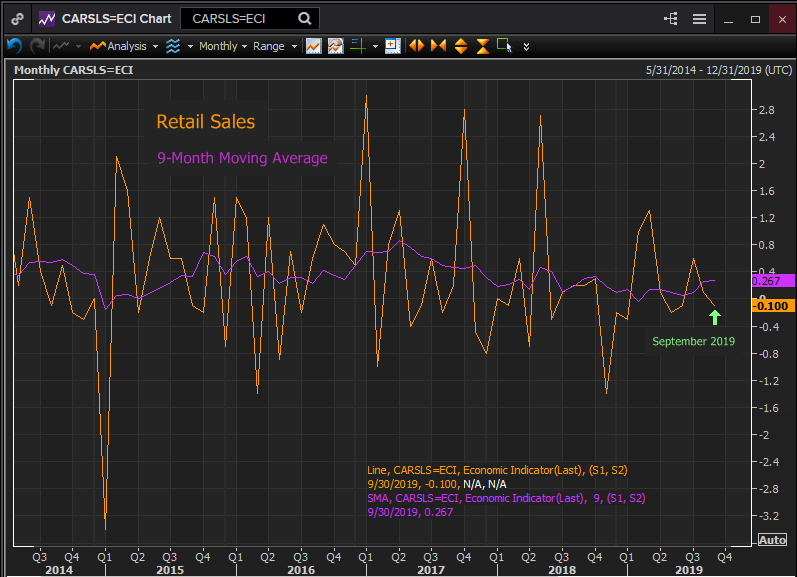

Annualized economic growth in the first three quarters averaged 1.77% a slight advance over the 1.65% pace in 2018. Retail Sales have averaged 0.267% monthly through September this year compared with 0.117% per month in 2018.

Reuters

The labor market improved. Job creation was more than one-third higher in 2019, averaging 25900 a month through November – and that includes a loss of 71,200 that month in the largest single-month drop since the financial crisis. In 2018, the Canadian economy created 16300 new positions each month. Unemployment reached its lowest point in 45 years in May of this year at 5.4%. The monthly average through November of 5.664% was slightly better than 2018’s average of 5.825%.

Reuters

Business sentiment was on a slide in throughout most of 2019. The Ivey Business conditions index averaged 60.375 for all of 2018. In November of 2019, the average for the year was 54.136 and that covers a jump to 60 in the final month.

The Markit Manufacturing PMI registered 55.575 for the year in December 2018. By April, it had dipped below 50 – into contraction at 49.7 – and for the year scored 50.636 in November.

The prime drag on business outlook, as in the United States, was the trade war with China, which had seen increasing tariffs and fractured negotiations for much of the year.

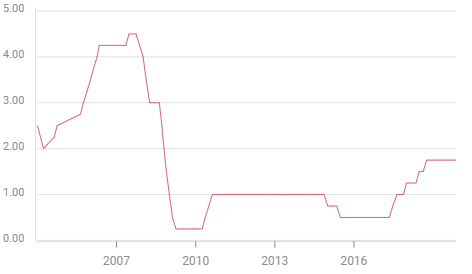

Bank of Canada avoids rate cuts

The Bank of Canada and Governor Stephen Poloz were secure enough about the strength of the economy to avoid the 75 basis points of rate cuts that came from the Reserve Bank of New Zealand, the Reserve Bank of Australia and the Federal Reserve from May to October.

Bank of Canada Interest Rates

These reductions left the BOC with the highest base rate in the developed world at 1.75%. The Fed’s official funds rate is actually a target range (1.5%-1.75%) and the effective rate is normally below the upper target. The BOC’s last rate adjustment was a 0.25% increase in October 2018 to the current 1.75%.

After the policy decision on December 4th, the bank statement said “there is nascent evidence that the global economy is stabilizing, with growth still expected to edge higher over the next couple of years. Financial markets have been supported by central bank actions and waning recession concerns, while being buffeted by news on the trade front. Indeed, ongoing trade conflicts and related uncertainty are still weighing on global economic activity and remain the biggest source of risk to the outlook.”

With the Federal Reserve on hold and projecting no change through the end of 2020 and the Canadian economy performing well, the BOC governors would need an extraordinary economic reason to re-open the interest rate discussion.

Canada: Election and re-election

Prime Minister Justin Trudeau’s Liberals held on to power in the October Federal elections while losing the popular vote to the Conservatives. Finishing with 157 seats, 13 seats short of a majority but far ahead of the Conservatives at 121, Trudeau’s minority government will depend on votes from the New Democratic Party’s 24 members, or the Bloc Quebecois’ 32.

Prime Minister Trudeau's priorities for his second term – climate change, expanding healthcare and gun control – do not have a specific economic focus though he also promised lower taxes and expanded trade.

Liberal governance will fall only when major legislation, such as a budget fails to pass Parliament.

The Trudeau government’s first real test is likely to come in February or March when it presents its first minority budget.

USMCA replaces NAFTA

The United States-Mexico-Canada Agreement (USMCA) which replaces the 25-year old North American Free Trade Agreement (NAFTA) aims to modernize trading between the three countries.

Mexico has already ratified the deal. The Democrats in the US Congress have ended their year-long objection and American approval could come soon. Canadian legislators, however, are not due back from their winter break until January 27th. The Trudeau government requires the support of the Conservative opposition, the minority New Democrats or Bloc Quebecois for passage.

Prime Minister Trudeau has said he was reasonably confident that his government would find the votes needed to approve the treaty.

Shrinking oil price volatility

Crude oil had a volatile first half and a restrained second. West Texas Intermediate (WTI) opened on January 2nd at $45.94, the low for the year and then executed a four-month climb to the 12-month high at $66.17 on April 23rd. By mid-June, WTI was back to $52.0 and until early October traded in a range up to $60.0 and back.

The US-China phase one trade first announced on October 13th provided WTI with new impetus and crude rose steadily reaching $61.18 on the 18th of December. That was the highest for the commodity since late May, excepting the two-day surge and collapse in mid-September around the Iranian attack on a Saudi oil refinery.

China-US trade: Threats had more impact than tariff imposition

Easily the most volatile political and meaningful economic topic on the global stage, the alternating hot-and-cold relationship between the two economic superpowers has roiled markets for close to two years.

Throughout that period, despite the imposition of tariffs and the occasional harsh rhetoric, the underlying market assumption has been that the two sides would eventually find an agreement.

Equities have been the strongest believers in this scenario and the stock averages have climbed steadily higher this year. The US S&P 500, the broadest major average, has added 7.8% in the two months since the US and China announced their phase one deal on October 13th and is 27.3% higher on the year. The Toronto Stock Exchange (S&P/TSX) is up 18.1% on the year.

The trade war has had a damaging impact on manufacturing in Canada as in the United States. The factory sectors have been in or near recession in both countries for much of 2019. But the overall economies, driven by a vibrant consumption and a strong labor economy have maintained positive GDP rates.

In one important measure, the threat of an all-out US-China trade has had more impact than the actual trade imposition. Businesses have largely stopped spending and investing, preferring to wait on the denouement of the trade conflict. Their logic is simple. Whatever the delay, projects can always be completed in the future, but investment spending that has no market because the global economy has dropped into a trade war recession can never be recouped. The fear of a global recession may be exaggerated but the rationality of the hesitation is accurate.

Conclusion: Whither the Canadian economy?

And that brings us to the largest question for 2020, the Canadian economy and indeed global growth. Will the US-China trade accord, and to a lesser degree Brexit, unleash business spending and propel a new round of economic expansion?

The economic fundamentals in Canada as in the United States are healthy. The consumer economy backed by a robust labor market has kept the economy growing. But an unremitted trade conflict between the US and China that had broken all lines of communication would inevitably damage consumer outlook and begin a downward spiral. That threat, however unlikely has kept business investment locked in bank accounts.

Anticipation of the beneficial effects of the accord has pushed WTI to a six month high and that is a good sign for the resource-heavy Canadian economy.

China is the world’s largest consumer of many raw materials. The mainland’s recessionary manufacturing sector and 6.2% official GDP in the first three quarters of 2019 have lowered global demand and prices.

The Bloomberg Commodity Index ((BCOM:IND) has been declining for the better part of two years. This year’s high of 82.71 was in April and the low was 76.07 in late August. In the past three weeks, the index has gained 4% to 80.15 (12/18/19).

The Canadian economy is well situated to profit from a surge of growth in China, the US and around the world.

Whether that growth takes place is a function of the US-China trade agreement and the tenor of the continuing relationship. Even after this accord many of the tariffs imposed over the last two years will remain in place. The trade, ownership and technology practices of Chinese companies for the past two decades will not vanish overnight, nor will optimism of US and Canadian executives return with two signatures.

If China and the United States maintain a cordial relationship in the months after the agreement is signed and talks continue toward a second deal, the global economy may prosper. There should be definite indications by the end of the first quarter.

Conclusion: Whither the USD/CAD

The USD/CAD opened 2019 on January 1st at 1.3648 courtesy of the three-figure ascent in the final two weeks of the old year. That spike fostered by the limited liquidity at year-end was quickly reversed in the first week and we may take 1.3276 the open on January 9th as the real start of trading for 2019.

Given that start, the trading level as of this writing at 1.3116 (12/19/19) represents a great deal of movement throughout the year with no discernible direction.

Neither the three Fed rate cuts from July to October, bringing the US base rate upper target from 2.5% to 1.75%, while the BOC stayed put nor the weakened government of Prime Minister Justin Trudeau after the federal election in October produced a standard currency reaction.

After the Federal Reserve began cutting rates on July 31st, the Dollar Canada (USD/CAD) rose almost three figures in the following six weeks. Subsequent to the October 21st Canadian elections the Canadian dollar fell for five weeks from 1.3135 to 1.3307 and then rose for two, ending within 20 points of where it started art 1.3115 (12/19/19).

The lack of trend over the year and the restricted ranges of the last six months can be laid at the feet of the US-China trade dispute. Like so much else in the global economy, a breakdown in the relationship between the two largest economies would drive markets and currencies in the direction of safety. USD/CAD would have soared as traders and investors looked for security in the assumed to be oncoming recession. The likelihood of such an outcome did not detract from its stultifying effect on trading.

With the pending trade agreement, the USD/CAD direction will be again be determined by the relative strengths of the two economies and the impact on the interest rate policies of the respective central banks. In that, the US probably has a modest advantage as its economy has been more directly affected by the trade war and so has more to recover.

Slated against that support for the USD/CAD is the continuing withdrawal of the safety trade to the US dollar as the tensions between Washington and Beijing slowly ebb. That move is likely to have greater impact on the USD/CAD in the first quarter as the US economy will take several months to register the impact of the trade agreement.

USD/CAD technical analysis

The restricted range over the past six months has left the support and resistance lines essentially unchanged through the latter part of the year.

The 21, 100 and 200-day moving averages are all trending lower. The 21-day turned south in early December. The 100-day has been trending lower since the first week of September and the 200-day since late June. The relative strength index has moved to oversold in the second week of December.

The 200-day moving average is of the most importance in positioning for a lower trend.

The breakout from the upward channel initiated in late October and breached on December 4th is now conclusive, as the USD/CAD has moved further and lower from its initial break.

The slight downward tilt of the pennant from early October is another indicator that the first attempt to move outside of the ranges of the last six months could be lower.

Major support and resistance levels for the USD/CAD are where they have been for the past two months.

The first support line is at 1.3050 with a band to 1.3018, the low in October 2018. There is another strip at 1.2900-1.2880 the reach of several lows late from August to mid-October 2018. Below that are the lows in October and May 2018, 1.2800-1.2760. Finally, there is a support line at 1.2550, the two-year low from April 2018.

Above the current level of 1.3117 (12/19/19), there is mild resistance at 1.3200. Beyond that, there is the strip at 1.3330-1.3350 high in the second half.

Between 1.3475 and 1.3500 are a series of levels that marked the top from late April to early June. Though pierced numerous times the Dollar Canada only closed above the upper limit at the very beginning and the very end of the period.

The next resistance is minor at 1.3525 just above the May high close.

The December 2018 high at 1.3685 is not a resistance level as it was a product of the limited year-end liquidity that occurs each December as the major currency market players close their books.

Technical support and resistance lines are indicators of historical price action. They provide signs of trading interest at their designated levels but offer little impediment to any fundamentally based move.

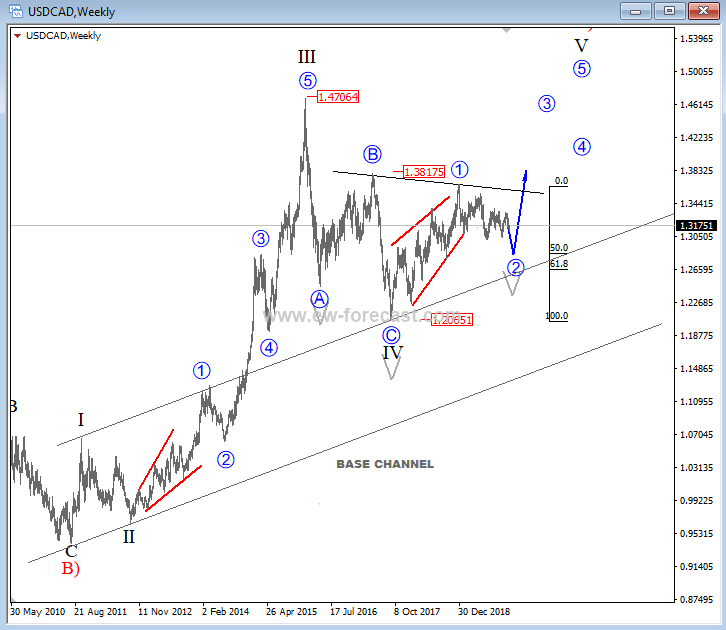

Gregor Horvat sees potential gains for the USD/CAD pair on his Elliott Wave counts:

USD/CAD Elliot Wave Analysis

USDCAD was trading mostly sideways in 2019, mainly because of a correction on Crude oil. But, this may change soon, ideally in 2020 where we can finally see some gains after that corrective sideways price action, especially if we are right about a potential decline on Crude oil. So, on Loonie we are still observing a bullish scenario that can send the price higher, which is also anticipated from an H&S perspective once the neckline around 1.37/1.38 is taken out.

USD/CAD Forecast Poll 2020

| Forecast | H1 - Jun 30th | H2 - Dec 31st |

|---|---|---|

| Bullish | 32.3% | 36.4% |

| Bearish | 38.2% | 48.5% |

| Sideways | 29.4% | 15.1% |

| Average Forecast Price | 1.3102 | 1.3089 |

| EXPERTS | H1 - Jun 30th | H2 - Dec 31st |

|---|---|---|

| Alexander Douedari | 1.3500 Bullish | 1.3800 Bullish |

| Andrew Lockwood | 1.3500 Bullish | 1.3500 Bullish |

| Andrew Pancholi | 1.3207 Bullish | 1.2934 Bearish |

| BBVA Bancomer Team | 1.3100 Sideways | 1.2900 Bearish |

| BoA FX, Rates and Commodities Team | 1.3200 Sideways | 1.3100 Sideways |

| Brad Alexander | 1.2900 Bearish | 1.2500 Bearish |

| Chris Weston | 1.3100 Sideways | 1.3400 Bullish |

| Christina Parthenidou | 1.3650 Bullish | 1.3400 Bullish |

| CIBC World Markets Team | 1.3400 Bullish | 1.3700 Bullish |

| CitiFX | 1.2900 Bearish | 1.2600 Bearish |

| Danske Research Team | 1.2900 Bearish | 1.2700 Bearish |

| Dmitriy Gurkovskiy | 1.2500 Bearish | 1.4500 Bullish |

| Dukascopy Bank Team | 1.3100 Sideways | 1.2700 Bearish |

| Eagle FX Team | 1.2500 Bearish | 1.1900 Bearish |

| ForexGDP Team | 1.2800 Bearish | 1.2300 Bearish |

| FX Trading Revolution Team | 1.2900 Bearish | 1.2600 Bearish |

| Goldman Sachs Global Investment Team | 1.3100 Sideways | 1.3000 Bearish |

| Gregor Horvat | 1.3500 Bullish | 1.4000 Bullish |

| ING Global Economics Team | 1.2900 Bearish | 1.2500 Bearish |

| Ipek Ozkardeskaya | 1.3200 Sideways | 1.3000 Bearish |

| Jamie Saettele | 1.2900 Bearish | 1.2500 Bearish |

| Jeff Langin | 1.3200 Sideways | 1.3200 Sideways |

| Jose Blasco | 1.3400 Bullish | 1.3700 Bullish |

| NAB Global Market Research Team | 1.3000 Bearish | 1.3100 Sideways |

| National Bank of Canada Eco. & Strat. Team | 1.3300 Bullish | - |

| OctaFx Analyst Team | 1.3015 Bearish | 1.3340 Bullish |

| Rabobank Financial Markets Research Team | 1.3400 Bullish | 1.3600 Bullish |

| RBC Economic Research Team | 1.3000 Bearish | 1.3200 Sideways |

| Societe Generale Analyst Team | 1.3100 Sideways | 1.2900 Bearish |

| Stelios Kontogoulas | 1.3400 Bullish | 1.3800 Bullish |

| Stephen Innes | 1.2500 Bearish | 1.2300 Bearish |

| TD Securities Research Team | 1.3200 Sideways | 1.3100 Sideways |

| UniCredit Research Team | 1.3300 Bullish | 1.3600 Bullish |

| Wells Fargo Research Team | 1.3100 Sideways | 1.2900 Bearish |

The USD/CAD reached a low of 1.3015 in July 2017. This was the lowest level since October 2018. The highest level for the pair in 2019 was 1.3570. There will be several catalysts for the pair in 2020. First, the USMCA, which was negotiated between the United States, Canada, and Mexico. The US side has already reached a deal in support of the deal. This means that the USMCA could be ratified in the coming year. Another catalyst could be central banks. The Fed has pointed that it won’t hike rates in 2020. The BoC, which was relatively passive in 2019, could also hike at least once in 2020. The pair may drop to 1.3015, which is an important support level by June. The pair may also move upwards to the 50% Fibonacci Retracement level of 1.3340 by year end.

We see improved economic signs into 2020 with the USMCA and stable WTI prices but a rate cut in early 2020 may oppose this. We see a stable US economy into 2020 and no interest rate cuts until 2021 and a resolution to the pointless US/China trade war. Assuming a Biden or Bloomberg win in the November elections, we see USD strength into 2021.

Related 2020 Forecast Articles

EUR/USD: Lean times soon to turn into flush times for euro dollar

GBP/USD: Pound may continue to fall on hard Brexit deadline

USD/JPY: A journey from trade fears to high-stakes elections

AUD/USD: May the aussie live in interesting times

Gold: XAU/USD bulls likely to remain in control

Crude Oil: WTI bulls to hold their horses despite tighter market, rosier economy

USD/INR: Domestic factors barely support a turnaround for Indian rupee

Bitcoin: BTC, the ultimate store of value

Ethereum: Calm on ETH/USD after the storm is over

Ripple's XRP: The glimpse of hope

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.