USD ahead of key data releases this week

Despite the Easter Monday lull, this week promises to be eventful for the USD. Key data releases and speeches could trigger significant volatility, impacting the American Dollar's direction.

Daily Dollar Index Chart - Source: ActivTrader

The Dollar Index has gained roughly 3.16% year-to-date, following a 5.22% decline in the final two months of 2023. Upcoming shifts in US monetary policy, particularly in relation to those of major economies like the Eurozone, UK, Canada, and Australia, will be crucial factors determining whether the greenback strengthens (Dollar Index rising) or weakens (Dollar Index falling) against its counterparts.

Let’s take a closer look at what to watch out for this week.

Monday 1st: US ISM Manufacturing PMI at 2:00 PM GMT

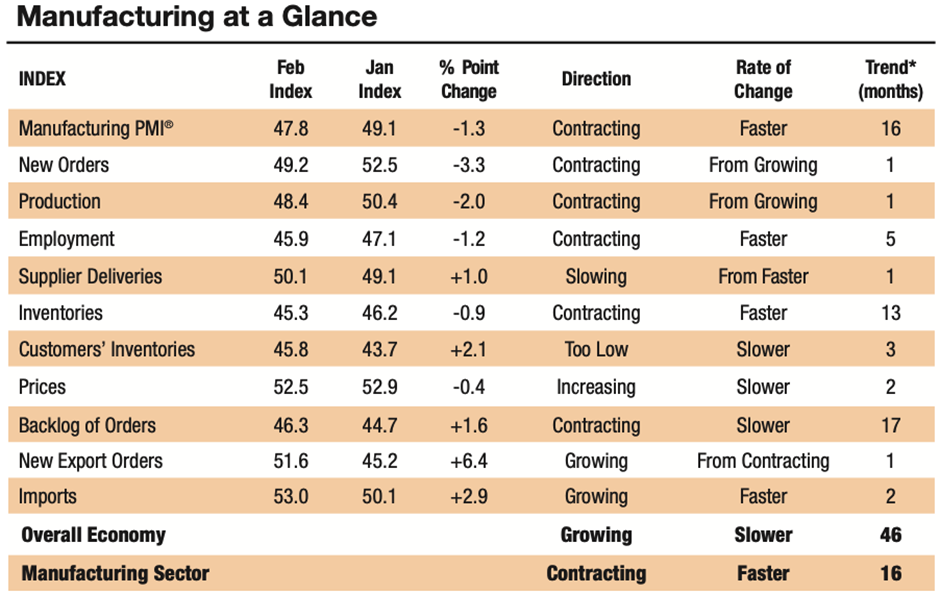

The February ISM Manufacturing PMI painted a relatively pessimistic picture of the US manufacturing sector.

The index dipped to 47.8, indicating a contraction since November 2022. Compared to January 2023, the report revealed a further slowdown, mostly in demand and production levels. Even though the overall US economy wasn't officially in recession, this extended contraction in manufacturing could suggest potential trouble ahead if things do not improve in the coming months.

Of course, some bright spots exist within specific manufacturing industries not captured by this broad survey, such as manufacturing industries like Fabricated Metal Products, Chemical Products, and Transportation Equipment, which all registered growth in February.

For the month of March, the market is expecting a slight improvement to 48 expected, which is still below the 50 level separating contraction to expansion.

Source: Institute For Supply Management (ISM)

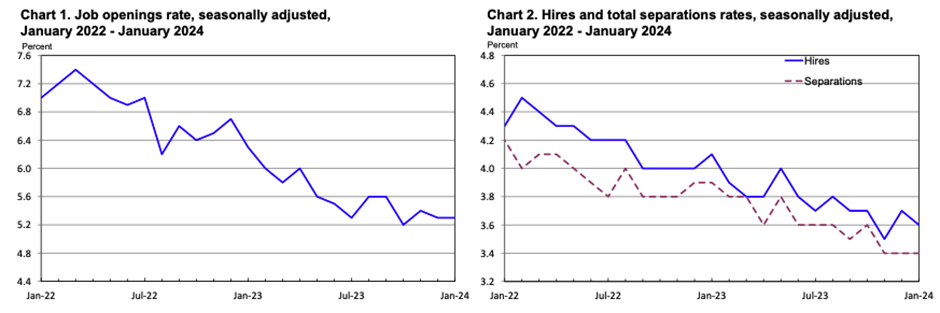

Tuesday 2nd: Job openings and labor turnover survey at 2:00 PM GMT

US job openings in January 2024 edged lower at around 8.7 million from 8.9 million. While this does still indicate continued strong employer demand for workers and a healthy labor market, this figure also marks a decrease from both the 2023 annual average (9.4 million) and the peak of 12.2 million openings recorded in March 2022, which suggests a potential moderation in hiring activity. For the month of February, market participants are expecting a dip to 8.84 million.

Source: Bureau of Labor Statistics

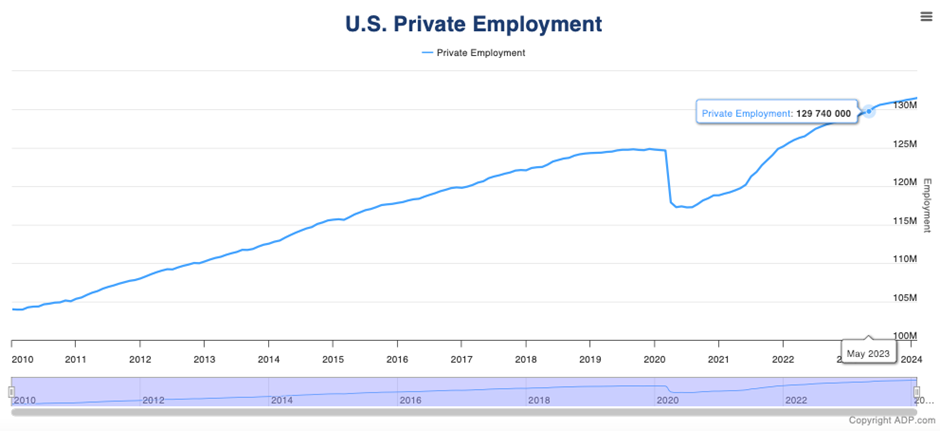

Wednesday 3rd: ADP Nonfarm Employment Change at 12:15 PM GMT

The ADP Non-Farm Employment Change is a monthly economic data release that tracks the level of non-farm private employment in the United States, published by Automatic Data Processing (ADP).

It usually provides a preview of the overall health of the U.S. labor market, specifically within the private sector and traders often closely monitor it because it’s a leading indicator for the official government jobs report, released a few days later by the Bureau of Labor Statistics (BLS).

The ADP report for February delivered positive news for the US labor market. Private businesses added a net total of 140,000 jobs, with the service-providing sector leading the way with a gain of 110,000 jobs and the goods-producing industries adding 30,000 positions.

The report further revealed interesting insights into job creation by company size. Medium-sized establishments (50-499 employees) were significant contributors, adding 69,000 jobs, while large establishments (500+ employees) followed closely behind with 61,000 new hires. Looking ahead, market participants expect the ADP report to show continued job growth for March, with an employment change of 149,000 expected for last month.

Source: ADP National Employment Report

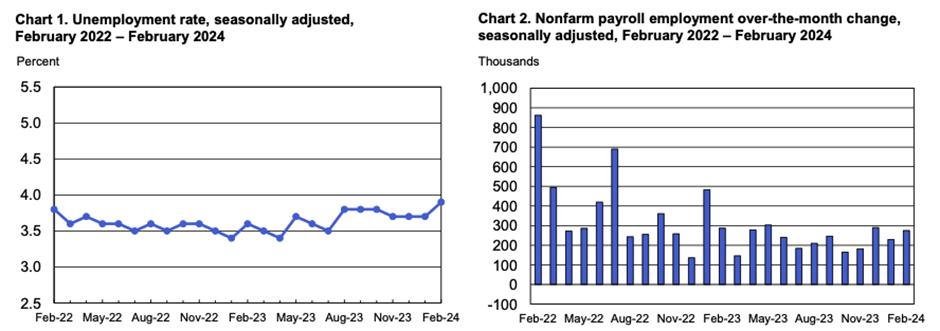

Friday 5th: Nonfarm Payroll at 12:30 PM GMT

One of the most eagerly awaited updates for Forex traders, particularly those with a keen eye on the American Dollar, is the Non-Farm Payroll (NFP) report. This report is indeed a key economic indicator released by the U.S. Bureau of Labor Statistics on the first Friday of each month that provides data on the total number of paid American workers, excluding employees from certain sectors such as farming, government, private household, and nonprofit organizations.

It is highly anticipated because it offers insights into the strength and direction of the American labor market, as well as inflationary pressures, which helps Fed officials in their decision to modify their monetary policy trajectory.

After a robust showing of 275,000 jobs added in February, market projections indicate anticipation for the NFP to have maintained momentum, hovering around the 200,000 mark last month, with estimates at approximately 205,000.

However, unexpected shifts in the unemployment rate occurred, as it climbed unexpectedly to 3.9% in March, marking its highest level in over a year. Analysts predict that there will likely be no significant changes in this respect.

Source: BLS

Other news and speeches to follow this week

Unemployment claims on Thursday 4th, 2024, expected to reach 214,000 after 210,000 last month, will be published at 12:30 PM GMT, which might trigger market volatility, as unemployment claims are often seen as a leading indicator of economic health.

Employment, spending, confidence, and growth are all tightly linked. When unemployment claims rise, it suggests fewer people are working, which translates to less spending. This can lead to a decline in consumer confidence, which further dampens spending and slows economic growth. Conversely, a significant drop in claims could suggest a strengthening job market and an improved US growth.

Adding to the potential for volatility, Fed officials will deliver various speeches this week. The markets will be attuned to the tone, with more hawkish stances than expected (advocating for tighter monetary policy) likely to strengthen the US Dollar or more dovish stances than expected (advocating for looser policy) potentially weakening the American currency.

Here are the speeches to follow this week in local time:

-

6:50 p.m. - Governor Lisa D. Cook on Monday.

-

10:10 a.m. - Governor Michelle W. Bowman on Tuesday.

-

9:45 a.m. - Governor Michelle W. Bowman on Wednesday.

-

12:10 p.m. - Chair Jerome H. Powell on Wednesday.

-

4:30 p.m. - Governor Adriana D. Kugler on Wednesday.

-

7:30 p.m. - Governor Adriana D. Kugler on Thursday.

-

12:15 p.m. - Governor Michelle W. Bowman on Friday.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Author

Carolane de Palmas

ActivTrades

Carolane graduated with a Masters in Corporate Finance & Financial Markets and got the AMF Certification (Financial Markets Regulator in France). Afterward, she became an independent trader, investing mostly in European and American stocks/indices.