- US economic growth and Fed policy depend on consumer spending.

- Inflation has poleaxed consumer sentiment and threatens consumption.

- American wages are failing to keep pace with 8.5% inflation.

- Producer prices soar 1.4% and 11.2% in March, both records.

In normal times the consumer can be counted on to keep the US economy humming. Over the last year household spending has come under increasing threat from rampaging prices. It is an open and crucial question how long the inflation-battered US consumer can continue to fund the current economic expansion.

Retail Sales are forecast to rise 0.6% in March, doubling the February gain. Sales ex-Autos are expected to climb 1% after a 0.2% increase in February. The Control Group category, which mimics the consumption component of GDP, is projected to rise 0.2% after falling 1.2% in February.

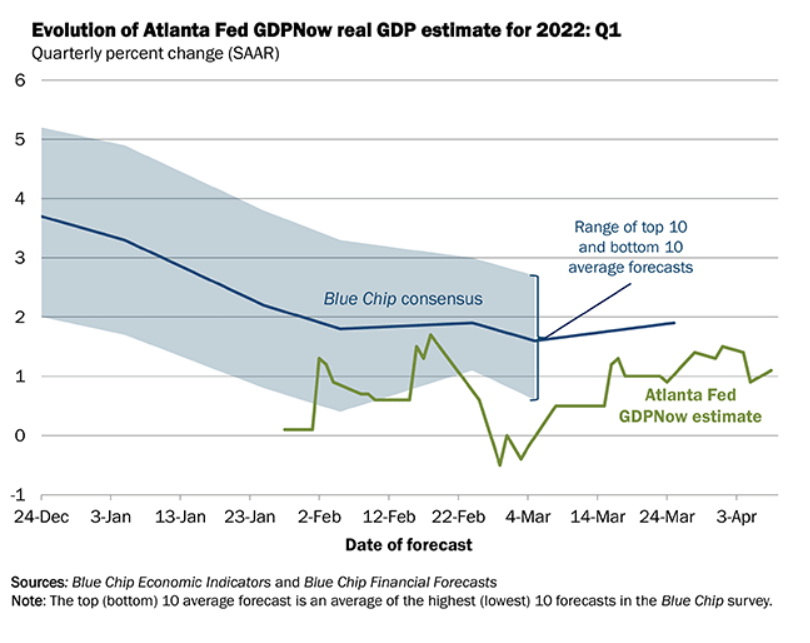

The Federal Reserve has embarked on a rate tightening regime that could, by year end, bring the fed funds rate to 2.5% or higher from its current 0.5%. That program is wholly contingent on an expanding US economy. The Atlanta Fed’s GDPNow program estimates first quarter growth at 1.1%, with a new calculation due after Thursday’s sales figures. There is very little leeway in US growth. If the economy contracts in the quarter just ended, it is difficult to see how the Fed hikes 0.5% on May 4 as widely predicted.

Sales have averaged 2.6% in the two months of the first quarter reported. That excellent gain is due to the 4.9% increase in January that followed a 0.5% overall decline in the last quarter of 2021. Given the huge jump in January sales, the quarter is likely to remain positive for consumption and GDP even if the March figures take an unexpected plunge.

Let's take a look at the sales indications for March.

Retail Sales: Positive indicators

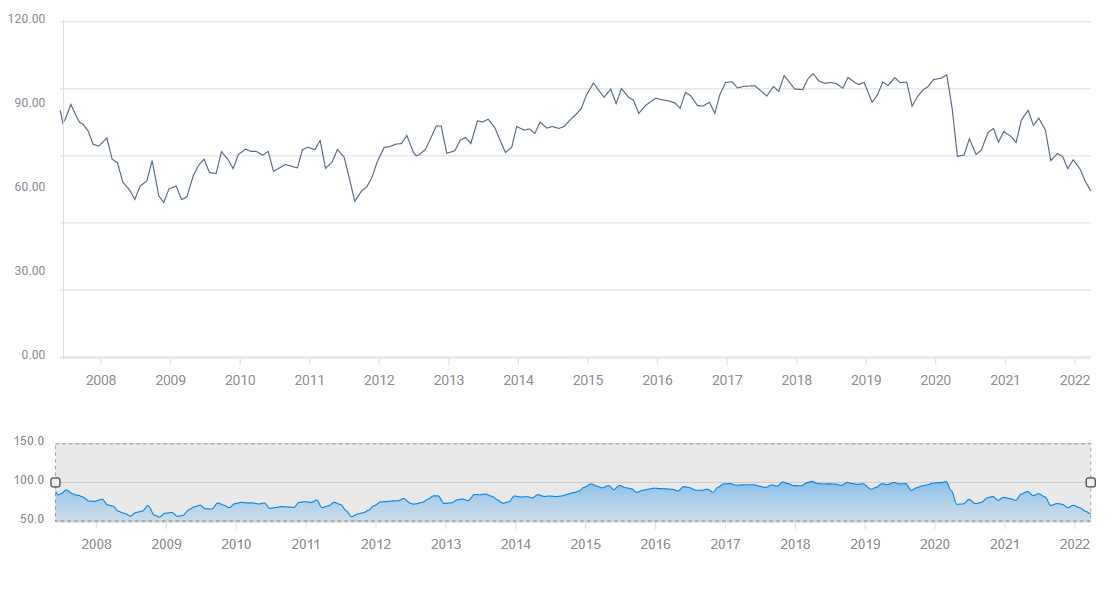

The best hope for strong consumption is Americans' tendency to spend regardless of external circumstances. Consumers say they are very unhappy. The Michigan Survey has been near recessionary lows for eight, soon to be nine months, and it has not had a noticeable impact on spending.

Michigan Consumer Sentiment

Behind the resilience is the robust job market. Payrolls have averaged 596,000 for six months and 482,000 for 12. The unemployment rate was 3.6% in March, a level in former times considered beyond full employment. Initial Jobless Claims were 166,000 in the latest week, the second lowest total in the 55-year series. Available positions in the Job Openings and Labor Turnover Survey (JOLTS) have averaged almost 11 million for nine months, an all-time record. Anyone in the US who wants to work can find a job.

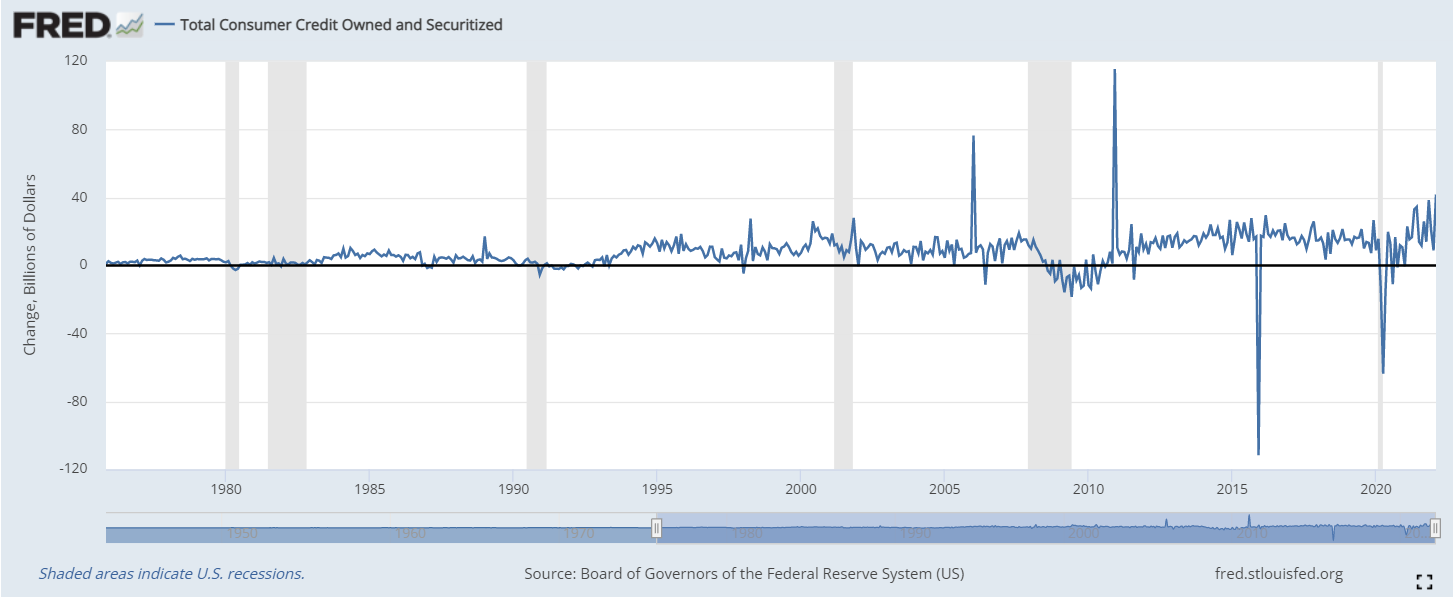

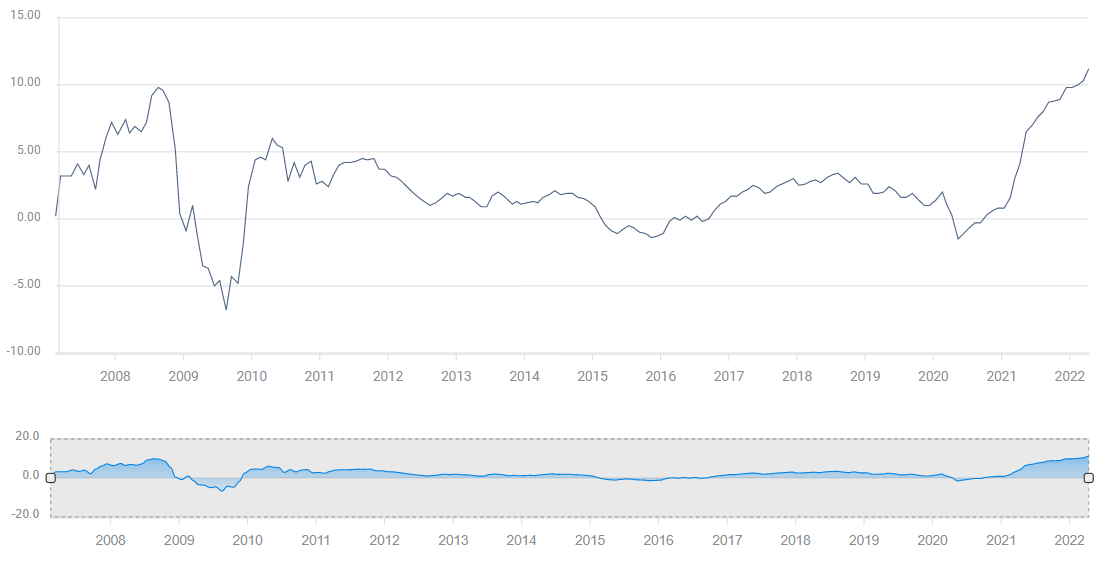

Consumer credit expanded $41.8 billion in February, far more than the $6.8 billion expected and the third highest monthly total in a statistic that goes back to 1943. The extravagance can be interpreted in two ways. The willingness to assume more debt might be due to the confidence generated by the job market, or it might be an expedient necessary to shore up the inflation erosion of purchasing power.

Consumer Credit

Retail Sales: Negative indications

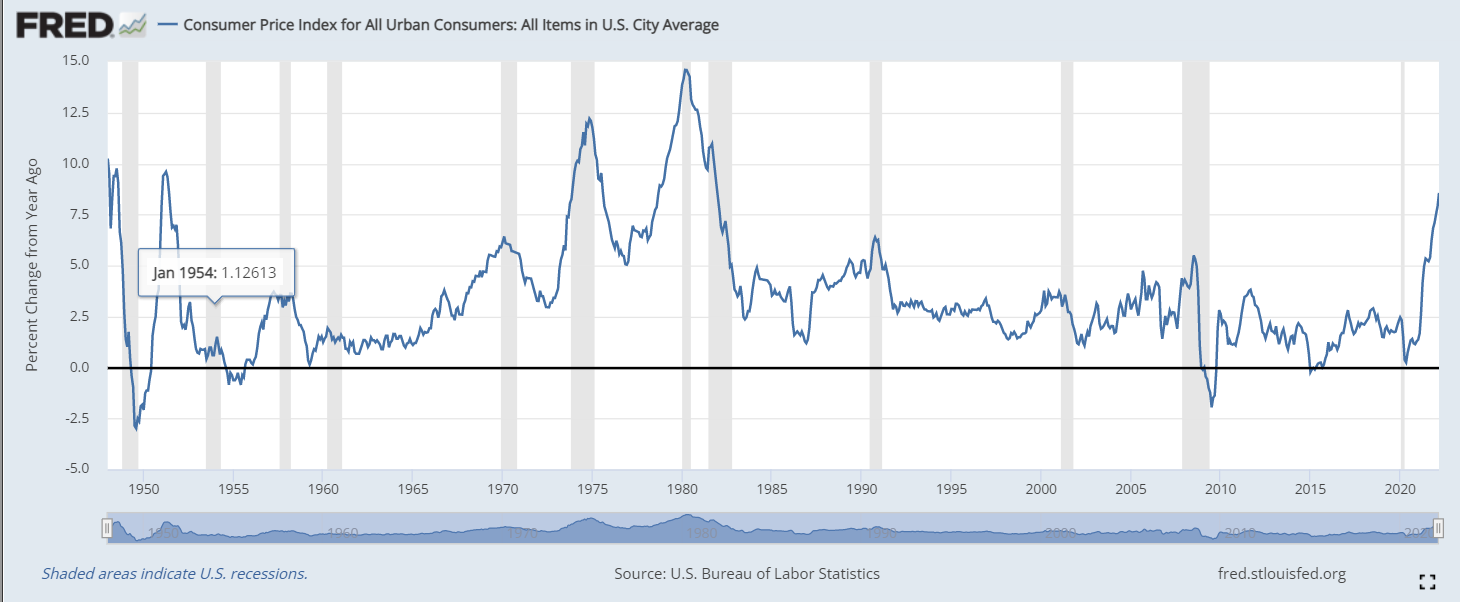

Inflation is the main culprit. It is responsible for the dismal consumer sentiment reading, but more importantly, it has long-since overtaken wage increases and is draining consumer finances every month. In March annual real inflation-adjusted income dropped 2.7%, despite a 5.6% increase in Average Hourly Earnings. It was the 12th straight month of decline. That is a financial impact consumers will find impossible to ignore.

Although headline CPI rose 8.5% annually in March, many necessities saw much greater increases. Overall food expenses jumped 8.8% but home grocery costs climbed 10%, another record. Meat, poultry, fish and eggs were up 13.7%, beef 16%, dairy and related products 10.3%. Cereal and bakery products are up 9.4%, fruits and vegetables 8.5%.

CPI

Gasoline was 18.1% higher in March and up 48% for the year. Fuel oil vaulted an astonishing 70.1% in 12 months, natural gas was up 21.6% and domestic electric charges jumped 11.1%.

When the basic cost of living rises so much and so quickly, CPI was 1.4% last January, adjustments to household budgets are inevitable. At first, families will maintain spending by dipping into saving and extending credit, hoping that inflation subsides. Eventually, adjustments will begin in discretionary purchases and that will continue until expenses are in line with income. Has that process begun?

Consumer inflation has been 5% or higher for 11 months and there is no end in sight to the elevation.

The annual Producer Price Index (PPI) soared 11.2% in March, up 1.4% in the month, from 10.3% in February. The core rate jumped 9.2% from 8.7%. These are the highest PPI readings in the 12 year series. Increases of this magnitude, especially in the current environment, are sure to be passed on to consumers. Inflation may not be peaking, it may not even be finished accelerating.

PPI

Market conclusion

Retail Sales and consumption in general are the economic keys to the next two quarters. If consumers defy both their own outlook and their shrinking wallets and maintain a modest if not expansionary attitude, the US economy should be able to avoid recession and the Federal Reserve will continue its rate increases.

If consumer spending stagnates or falls, business expansion will follow and US economic growth will be in serious question. As noted above, at 1.1% in the Atlanta Fed estimate, there is no room for weak Retail Sales.

Markets will react in a straight line with the strength of the sales figures. Better than expected results support Treasury rates and the dollar. Equities should be able to ignore the prospect of higher interest rates as strong sales mean an expanding economy.

Weak or negative sales raise a host of problems about the second quarter but the immediate reaction will be lower Treasury yields, a lower dollar and fading equities. For the stock market, the prospect of a recession is more daunting than higher interest rates.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD: Momentum favours further gains

In line with the broad recovery in the risk-linked complex, AUD/USD left behind a two-day negative streak and resumed its uptrend towards the 0.6400 region, always on the back of the resurgence of quite a strong downside pressure hitting the US Dollar on Thursday.

EUR/USD: Extra advances appear in the pipeline Premium

EUR/USD followed the widespread improved sentiment in the risk-linked galaxy and managed to set aside two daily drops in a row and refocus on the upper end of its recent range around the 1.1400 zone on Thursday.

Gold sticks to the bullish stance near $3,330

On Thursday, gold regained lost ground after two consecutive days of declines, with XAU/USD climbing back toward $3,300 per troy ounce following an earlier rally to roughly $3,370. The metal drew safe-haven buying as renewed fears of a US–China trade flare-up weighed on broader markets.

Crypto Today: SUI and Trump token in profit, BTC price fails $95K test amid rumours of lower China tariff

The cryptocurrency market capitalization dips below $3 trillion on Thursday, retreating 3.5% from the 50-day peak of $3.2 trillion recorded earlier this week.

Five fundamentals for the week: Traders confront the trade war, important surveys, key Fed speech Premium

Will the US strike a trade deal with Japan? That would be positive progress. However, recent developments are not that positive, and there's only one certainty: headlines will dominate markets. Fresh US economic data is also of interest.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.