- Retail sales forecast to be unchanged in January.

- Control group and ex-automobiles categories to moderate.

- Labor market and consumer sentiment remain strong backers.

The US Census Bureau will release the advance report on Monthly Sales for Retail and Food Services for January on Friday, February 14th at 13:30 GMT, 8:30 EST.

Forecast

Retail sales are predicted to rise 0.3% in January as in December. The retail sales control group, the Bureau of Economic Analysis’ (BEA) GDP component, is expected to slip to 0.3% from 0.5% in December. Sales ex-autos are projected to increase 0.3% following Decembers 0.7% gain.

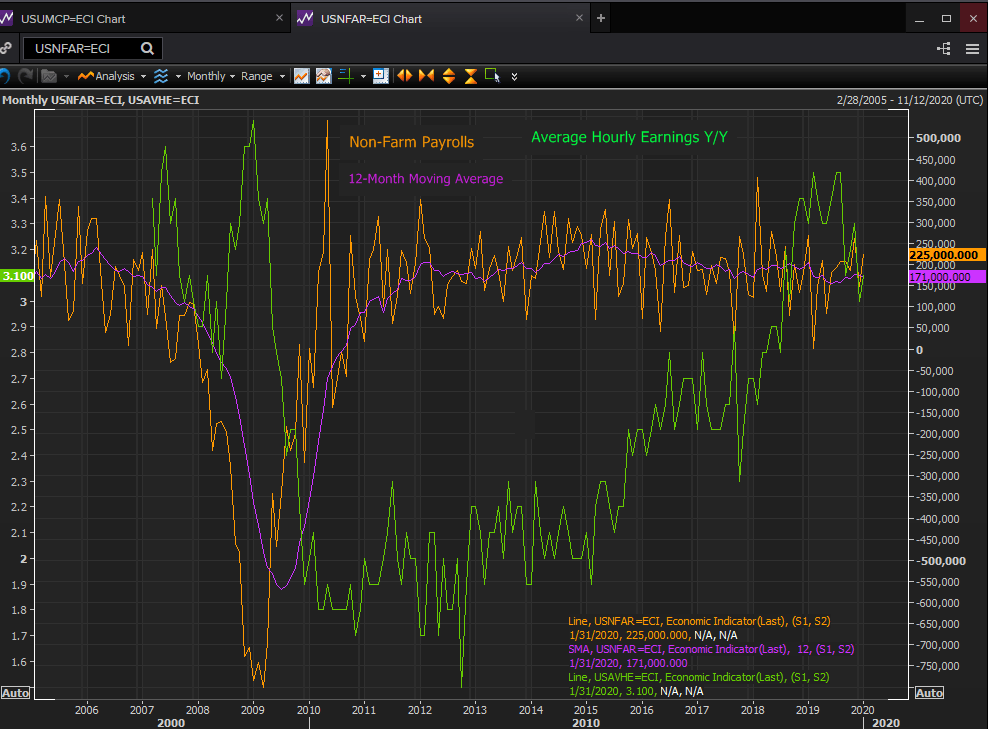

Wages and the labor market

It’s a truism that if the US consumers have income they will spend it. The US economy has provide plentiful proof over the last three years that this remains accurate.

Annual average wage increase have been at 3% or higher for 18 months through January.

Non-farm payrolls averaged 175,000 new jobs each month in the year to December. If this was a decline from 235,000 in at the start of 2019 it is more than enough to supply the natural labor force expansion of 125,000-150,000 new workers each month with positions.

This surplus of employment is the main reason that wage gains are stable near their best levels of the decade despite the unexploited labor pool represented by the improved but historically low 63.4% participation rate.

Reuters

Personal income

This measure of income from the Bureau of Economic Analysis counts almost all sources of incoming funds including wages, salaries, interest payments, dividends, workmen's compensation, pensions , social security and other transfer payments. It rose 0.2% in December.

The 12-month moving average has tailed off this year to 0.317% in December from 0.375% in January and from 2018’s four year high of 0.508% in July and August, but it remains a constant addition to family and individual income.

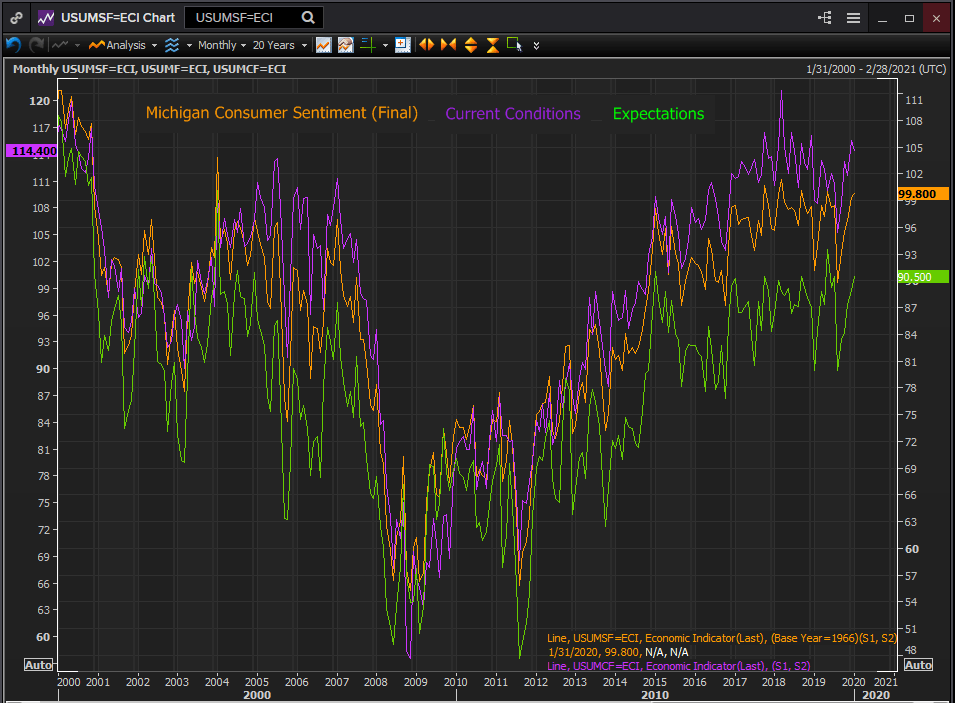

Consumer sentiment

Michigan consumer sentiment has made a complete recovery from its August 2019 plunge. At 99.8 in the overall index, 90.5 in the expectations index and 114.4 in the current conditions score in January, the outlook of the US consumer is near the top of the past three years which places among the highest reading of the past two decades.

Reuters

The preliminary figures for February due on the 14th are expected to remain buoyant at 99.5 overall, 115 for current conditions and 90.3 in expectations.

Whatever is going on in Washington, China and the rest of the world, close to home America is remarkably sanguine.

Retail sales

Consumption over the past year, aside from the anomalous reading of -2% in December 2019 and 1.4% in January 2019 that were due to reporting problems around the government shutdown in January, has been stable.

The 11-month moving average for retail sales in December (excluding the above mentioned months) was 0.4%, a bit higher than where it was in November 2018. The same average in the ex-autos category was 0.364% in December, almost equal to the November 2018 score of 0.373%. Finally the retail control group that informs the BEA’s GDP calculation for consumption was 0.327% in December and 0.368% in December 2018.

Despite all the political wrangling and bitterness in DC, the US-China trade dispute, the recession in manufacturing and assorted international and now health crises, US consumers has stayed close to their happy employment roots.

Conclusion and the dollar

The main factors enabling retail sales, employment, wages and consumer sentiment have remained strong through the second half of the year and into January.

The pickup in hiring in the New Year may owe something to the China trade deal and the next few months may show lower numbers due to the mainland health crisis, but the trend is stable and is the biggest consideration in expanding consumption.

Wages continue to outpace inflation and provide higher amounts of disposable income. Consumer sentiment reflects these conditions and suggests a willingness to spend the profits of employment. There is no reason for this to change in January.

The dollar has gained 3% against the euro since the beginning of the year. Initially a product of the positive ramifications for the US economy of the China trade deal, the move since early February is a safety reaction to the corona virus crisis in China. The much weaker improvement versus the yen, less than 1%, is likely due to the Japanese currency’s safe-haven status in Asian markets.

A good retail sales result for January will reinforce the notion that the US economy is still the most successful of the major industrial nations. The dollar can only benefit.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

EUR/USD remains depressed near 1.1350

The US Dollar now grabs momentum and motivates EUR/USD to return to the 1.1350 zone on Thursday, as investors continue to digest the ECB’s decision to lower its policy rates by 25 basis points, as widely estimated. It is worth noting that most markets will be closed on April 18, Good Friday.

GBP/USD maintains the consolidation around 1.3260

The upside momentum in the British pound remains well and sound on Thursday, underpinning the eighth consecutive daily advance in GBP/USD, which now trades in a consolidative fashion near 1.326. Cable’s strong performance comes despite the marked rebound in the US Dollar.

Gold breaks below $3,300, daily troughs

Further improvement in the sentiment surrounding the risk-associated universe put Gold prices to the test on Thursday. Indeed, the troy ounce of the precious metal faces increasing downside pressure and breaches the key $3,300 mark to hit new daily lows.

Crypto market cap fell more than 18% in Q1, wiping out $633.5 billion after Trump’s inauguration top

CoinGecko’s Q1 Crypto Industry Report highlights that the total crypto market capitalization fell by 18.6% in the first quarter, wiping out $633.5 billion after topping on January 18, just a couple of days ahead of US President Donald Trump’s inauguration.

Future-proofing portfolios: A playbook for tariff and recession risks

It does seem like we will be talking tariffs for a while. And if tariffs stay — in some shape or form — even after negotiations, we’ll likely be talking about recession too. Higher input costs, persistent inflation, and tighter monetary policy are already weighing on global growth.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.