US Retail Sales and the prospect of a hawkish shock from the Fed

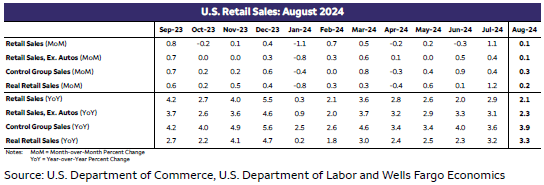

The last major piece of economic data before the FOMC decision on Wednesday saw retail sales come in mostly in line with expectations. Headline sales data rose by 0.1% last month, marginally better than the -0.1% decline expected. Core retail sales, excluding autos and gas, rose 0.2% and the control group rose by 0.3%, as expected. Anyone looking for a weak print that solidified hopes for a 50bp rate cut tomorrow must have been disappointed. There is no evidence that the US consumer is weakening, and Bloomberg’s second measure of consumer spending, which breaks down consumer spend by sector, shows an increase in spending across multiple categories including: food and beverages, especially grocery stores, and general merchandise. Some components of healthcare spending also rose, including cosmetics.

This data highlights the tough decision facing the Fed as it tries to avoid a recession and get inflation back to the target rate. There are undeniably still signs of inflation in the US economy, yet the market is still pricing in a 65% chance of a Fed rate cut tomorrow.

Why the Fed meeting may deliver a hawkish 50bp rate cut

This data was not particularly market-moving, the dollar has jumped higher, and 2-year yields are back at the highs of the day around 3.59%. We may see the dollar continue to recover on the back of the retail sales report. USD/JPY is testing resistance above 141.10, as it recovers from Monday’s sell off. Although we don’t think that the retail sales data changes the dial for this week’s Fed meeting, it does plant the seed of doubt about how dovish the Fed will be on Wednesday and current pricing in the Fed Funds Futures market start to look a bit excessive. There is currently 118 basis points of cuts priced in for the Fed by the end of this year. That would mean most meetings between now and the end of the year would be a super-sized rate cut. We don’t think that the Fed is that dovish, and instead we would urge traders to prepare for a ‘hawkish’ shock from the Fed at this week’s meeting.

Will the Fed front-load rate cuts?

Even if the Fed does cut rates by 50bp, a ‘hawkish cut’ that suggests that the Fed is front-loading rate cuts only to hold back later, could see a reversal in market pricing including a stronger dollar, higher Treasury yields and weaker stocks. This would especially damage sentiment towards consumer stocks in our view, but it may boost financial stocks and tech stocks, as well as increasing overall market volatility.

Could the Fed fall back in line with the BoE and ECB?

A lot of the focus on global central bank decisions has been on the dominance of the Fed flying the flag for aggressive rate cuts. However, the Fed has not pre committed to anything. What if the Fed is not leading the way, and instead the more measured stance of the Bank of England is actually the model for central bank decisions going forward? Currently the market is not expecting the BOE to cut rates this week, and there are only 54bps of rate cuts priced in for the BOE for the rest of this year. This seems more reasonable than the excessive pricing of US rate cuts. Thus, we could see expectations for Fed rate cuts fall more in line with the BOE if the Fed sounds concerned about inflation at tomorrow’s meeting.

German economic woes and the ‘Teflon’ Dax

Elsewhere, the German economy remains in the doldrums. The ZEW survey of investor sentiment fell sharply in September on both the current measure and future expectations. This survey fell to its lowest level since early 2024, and dashes hopes that Europe’s largest economy is making a recovery. Although the ECB is cutting interest rates, there has been turmoil in corporate Germany in recent weeks. Unicredit bought up more than 9% of Commerzbank in an unexpected move, and it is trying to extend its ownership of the German bank. Added to that, Germany’s car manufacturers are facing crisis after crisis. Not only are electric car sales falling sharply in Germany, but VW is threatening to shut down German car plants for the first time and BMW is facing a massive recall of vehicles due to a problem with its brake mechanism. While investors’ confidence levels may have been dashed by the these corporate issues, the Dax continues to rally and is less than 140 points away from the record high from 2nd September. The Dax is starting to look like a ‘Teflon’ index that can bounce back from most things. The Mdax index of German mid-caps, which is more domestically focused, has also been rallying in recent weeks, and is back to its highest level since June. Although it is underperforming the mid-cap rally in the US, as you can see in the chart below, the Mdax has remained fairly resilient during this period of economic and corporate turmoil in Germany.

Mdax (white line) and Russell 2000, normalised to show how they move together

Source: XTB and Bloomberg

There has been little change in ECB rate cut expectations in recent weeks. The market is still expecting the ECB to cut 6 times by July next year, and there are 63bps of cuts priced in for the rest of this year.

To conclude, the US retail sales data has only marginally reduced expectations for a 50bp Fed rate cut tomorrow to 65% from 67%. However, we think that the prospect of a hawkish shock from the Fed is rising. Ultimately, we will be watching to see if the Fed, currently an outlier with a huge number of rate cuts priced in by the market, falls more in line with the ECB and the BOE’s rate cut expectations after tomorrow’s meeting.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.