US producers and consumers

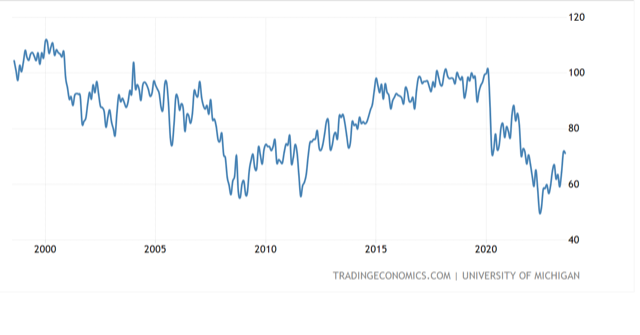

US Consumer Confidence, the University of Michigan Index, fell slightly to 71.2 in August.

US consumer confidence

Generally though, US consumers have been attempting a fightback from the terrible GFC levels recently seen. Nevertheless, consumers could still be characterised as generally depressed. The current level is only equal to the worst of the Covid lockdowns period.

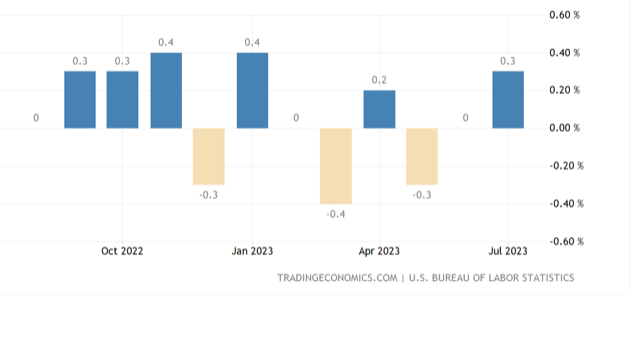

Meanwhile, some worries on the inflation front again. Producer Prices re-accelerated to 0.3% in July.

US producer prices

To be fair, it is a series that jumps around a bit, though the Fed will be watching closely. Within the data, and this is very telling in terms of how the Fed would be reflecting on things, the services component leapt 0.5%. This is the biggest services increase in a year. Exactly, what one of the Fed’s major concerns has been.

We should not get another Fed rate hike. The US and global economy are simply too weak to allow. We hope. What the Producer Prices data on Friday does tell us however, is that the tightening bias will remain and a little strenuously.

Stocks on Friday, really were very heavy again. As is often the case however, Monday morning Asia futures trading is as if nothing is wrong. It is just another week and to keep buying it would first appear. This kind of buying can persist all day thorough Asia. Even if in a bear market overall, and that is exactly what US stocks are threatening to become right now.

That some of the big tech stocks are seriously losing traction should not be underestimated. I still come back to those foundational manufacturing levels which look very ugly across all of the three leading economic zones of the world.

It really is a fight between liquidity optimism and concerning fundamentals at the moment. The fight is not yet decided.

This immediate consolidation phase could tell the story for the next 6-18 months of trading direction. Hence, I continue to suggest a heightened sense of focus in terms of managing your equity portfolio at this point.

While the China slow-down has been apparent to most of us for some time, it does seem to be getting greater attention in terms of headlines on the day.

We have not changed our long term decade view that China will see more subdued long term growth in the 2% o 5% range. Akin to, but still above, Western levels of economic activity. This is due to much larger economic cycles and realities than just the slowing global demand for exports or property bubble deflation. It has everything to do with the shift from agrarian to consumer economy having largely matured.

A mature ‘world’s second largest economy’ simply cannot be expected to proceed at the breakneck speed of the previous decades.

Author

Clifford Bennett

Independent Analyst

With over 35 years of economic and market trading experience, Clifford Bennett (aka Big Call Bennett) is an internationally renowned predictor of the global financial markets, earning titles such as the “World’s most a