US Presidential Election: Last Debate and Final Stretch

The third and last debate between the two main candidates in the final stretch before the US presidential election is set to take place in Las Vegas on Wednesday night. It’s rather fitting that the near-culmination of the two rivals’ bitter back-and-forth feuding should occur in a city known best for its gambling industry – it’s largely a matter of chance as to what will be in store for the nation and the world in this heavily-anticipated bashing contest.

In the current run-up to the November 8th election, it appears that Donald Trump, the candidate that has fallen increasingly behind his opponent Hillary Clinton, has been dealt virtually irreparable damage to his campaign. Arguably, this has mostly been a result of Trump’s own doing – stemming from his own words and actions, both past and present. But this historical presidential campaign and election process thus far has not been lacking in surprises – not in the least bit. Though the clock is ticking ever faster, particularly for Trump, there’s still plenty of time for more surprises to come. With that being said, however, this may be Trump’s last opportunity to turn the tide.

From reports on the Clinton campaign in recent days, it seems that Hillary will not be taking any chances despite her rather comfortable lead in various polls and Electoral College projections. She has been engaged in days of intensive debate preparation since the weekend. Clinton’s strategy will likely be to stick to her own key policy issues and try to allow Trump to dig an even deeper hole for himself.

As for Trump, his latest angle has been to proclaim that the media, the entire voting process, and even his own Republican Party are all steeped in a conspiracy against him and his campaign. What Trump will actually say and the primary strategy he will take during tonight’s debate is very much of a toss-up at this point. One Trump tactic, however, is virtually assured for the Las Vegas debate – he will continue to attack Clinton vehemently on her past political record, her personal email server controversy, as well as recently hacked emails surrounding the Clinton campaign – all of which may well do further damage to her already-suffering credibility.

Current Standings

As it currently stands, most projections show that Hillary Clinton already commands more than the requisite 270 Electoral College votes needed to win the presidency if the election is held today. Of course, there are still several major battleground and toss-up states that are very difficult to project at this point, but polls have continued to show Clinton extend her lead in many of those states as well. Key swing states still include Florida, North Carolina, Ohio, Arizona and Nevada.

As the presidency is currently leaning rather heavily towards Clinton with less than three weeks to go to Election Day, Trump will need a solid performance on Wednesday night’s debate in order to keep his chances alive.

Financial Market Impacts

The financial markets have taken recent developments in stride. Though there has recently been some volatility in the equity markets, stocks continue to remain not far off their recent record highs. As markets generally are highly averse to uncertainty, the status quo reassurance of a Hillary Clinton win will likely be much more amenable to the markets when viewed in contrast with the unpredictability of a potential Trump presidency.

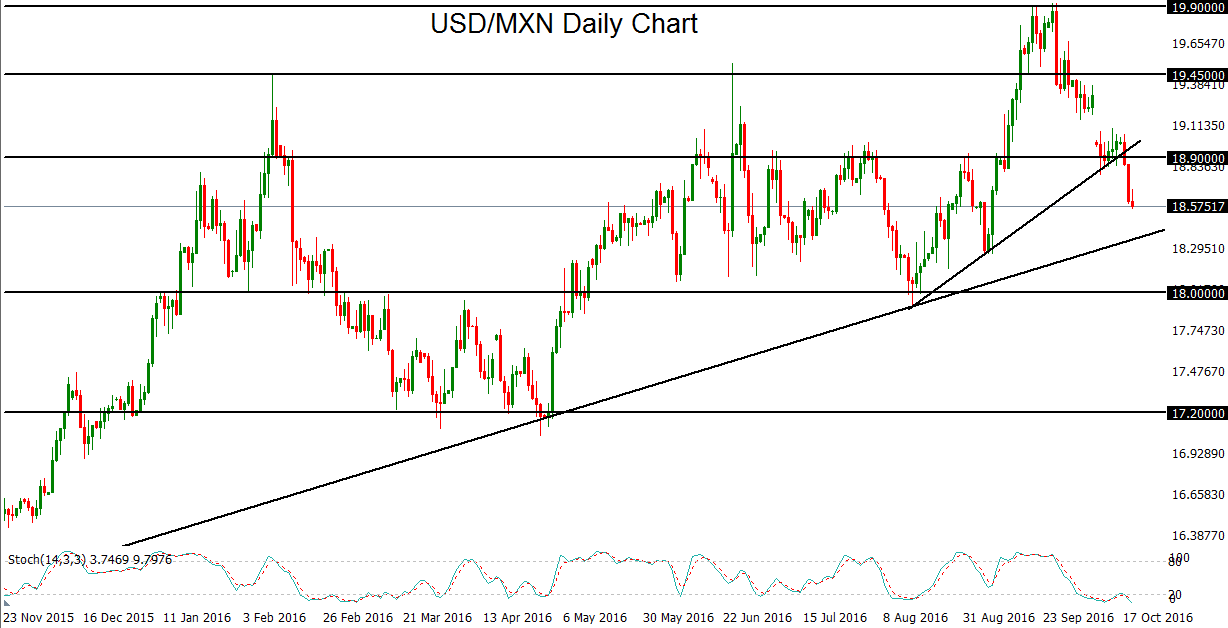

One notable market that has reacted rather prominently, and predictably, to the election process thus far has been the USD/MXN currency pair. This pair has recently been deemed the “Trump Trade” due to Trump’s policies and attitudes towards Mexico. It has been no secret that Trump’s heavily protectionist trade policies, not to mention his stance on immigration, have targeted Mexico in particular. Besides proposing to build a wall between the US and Mexico, Trump has also repeatedly expressed his staunch opposition to the North American Free Trade Agreement (NAFTA) and has proposed broad restrictions on both Chinese and Mexican imports. The result has been increasing speculation that if Trump is seen to win the presidency, the Mexican peso could suffer dramatically against the US dollar. However, the opposite is also likely to be true. That is, if Trump loses, the peso could rebound strongly. We have already seen this occur for USD/MXN, as it has fallen precipitously (denoting a rise in the peso against the dollar) in recent weeks as Trump’s presidential prospects have continued to diminish. If Clinton continues to widen her lead, the sharp decline for USD/MXN is likely to continue.

As for the US dollar itself, it has been on the rise in recent weeks, partly on the more likely prospect of a business-as-usual, status quo president in Hillary Clinton, although much of the dollar’s recent rise can be attributed to high expectations for a Federal Reserve rate hike this year. Safe haven assets like gold, in contrast, have fallen sharply due to the expected Fed move, a rise in the dollar, as well as lower risk of the uncertainty that would likely accompany a Trump victory.

Overall, the two candidates represent virtually polar opposites when it comes to many of their respective economic policies and issues of concern. Trump is a billionaire real estate mogul billed as the ultimate outsider aiming to shake up the US political establishment, which could potentially cause extensive market volatility along the way. Clinton is a classic Washington insider with deep ties to the current administration and the political status quo, and is seen as a relatively safer alternative for the financial markets, at least initially.

Going forward, as their key economic policies differ in so many ways, Trump and Clinton should each have a substantial, but very different, impact on various key financial markets in the event of victory.

Equity Markets

In the current run-up to the early November elections, we have already seen some volatility in the equity markets, partly due to concerns that the outsider, Donald Trump, who remains largely an unknown quantity when it comes to political leadership, will likely be exceptionally unpredictable and potentially precarious in his handling of global and domestic economic issues. But Trump's more business-friendly support of substantially lower corporate tax rates and financial de-regulation could help to provide a boost to investments and stock markets, at least in the initial phase of a Trump administration. With that being said, however, the likely possibility of setbacks in international trade due to his staunch protectionist trade policies and an increasing deficit under Trump due to his sweeping tax cut proposals could eventually have a significantly negative effect on the US economy and equity markets.

At the same time, although Hillary Clinton imparts a more business-as-usual sentiment on the financial markets due to her tacit agreement with most of the status quo economic policies of the current Obama administration, Clinton's increasingly fervent stance against major financial and corporate institutions, and in support of high corporate tax rates and significantly extended financial regulations, could ultimately weigh heavily on growth, investments, and key equity markets.

Currencies

As for the US dollar, Trump has repeatedly stated in public his position that the US Federal Reserve and Fed Chair Janet Yellen have been politically-motivated in keeping interest rates low. He has essentially accused the Fed of attempting to create false appearances of a healthy economy and stock market to embellish the Obama Administration. Trump has deemed the rising US equity markets as a “false stock market” that has been propped up by an overly accommodative Fed. This stance against what he sees as politically-driven dovishness provides a hint that if Trump gains the highest office in the land, he may be keen on instituting a more hawkish Fed. In that scenario, the possibility of higher interest rates going forward could lead to a stronger US dollar. In addition, Trump’s rhetoric on international trade issues has deemed his policy position as heavily protectionist. At least initially, this stance could lead to a further boost for the US dollar, especially against emerging market currencies like the Mexican peso and Chinese yuan.

As mentioned, Clinton is seen as the status quo candidate, unlike Trump. This status quo also extends to the very lengthy period of extremely accommodative monetary policy from the Federal Reserve. A Clinton administration is likely to continue favoring a “lower-for-longer” interest rate approach to US monetary policy, in contrast to Trump’s comparative hawkishness. If this is indeed the case, the Fed’s status quo will likely be maintained and the future outlook for Fed interest rate increases could continue to be slow. This scenario is apt to weigh further on the US dollar. Additionally, a Clinton win would obviously preclude a Trump presidency, which would be good news for emerging markets targeted by Trump’s protectionist trade policies, including China and Mexico, as mentioned above. In that event, those emerging market currencies would likely rebound further against the US dollar, which could place additional pressure on the greenback.

One currency that could benefit from a Trump victory, just as the Mexican peso and Chinese yuan may suffer, is the Russian ruble. Aside from being an exceptionally high-yielding currency, the ruble could also benefit from Trump’s well-known affinity towards Russian President Vladimir Putin. In a Trump presidency, if Russia benefits and Mexico suffers, as could be expected, the ruble could rise as the peso falls.

Gold

Where the dollar goes, gold tends to go in the roughly opposite direction. This is partly due to the fact that gold is a USD-denominated asset, and consequently has a strong degree of inverse correlation with the dollar. Additionally, lower interest rates tend to support gold prices while higher interest rates tend to pressure gold prices. This is due to the fact that gold is a non-interest-bearing, non-dividend-paying asset that tends to shine when yields are low, and become tarnished when yields rise.

The prospects of a progressively more hawkish Fed under a Trump administration has the potential to result in climbing interest rates and a strengthening US dollar. Together, these two forces could further pressure gold lower and potentially put an end to its recent recovery.

In contrast, a more dovish Clinton administration fostering a “lower-for-longer” interest rate outlook would likely boost the appeal and price of gold. Additionally, in the event of any downturn in equity markets due to the entry of a new administration, gold could also rise due to its traditional role as a safe-haven asset.

Energy

Trump has repeatedly stressed his position on energy issues. Specifically, he has spoken extensively about decreasing regulations on US energy production and increasing the country’s energy-producing capacity. If this indeed comes to be, higher oil production could likely add further to the current crude oil oversupply situation, thereby weighing even more on oil prices.

In a Clinton administration, however, crude oil prices could likely get a significant boost, as one of Clinton’s key objectives is a considerable shift towards developing renewable energy resources, most notably solar energy. As a result, US crude oil production would likely drop dramatically, cutting into the global oil supply and supporting crude oil prices.

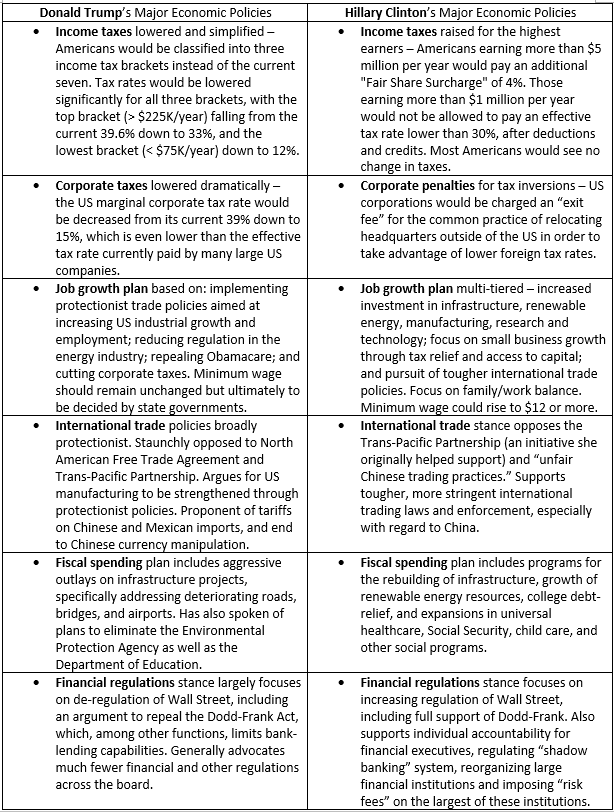

Comparison of Trump’s and Clinton’s Major Economic Policies

Author

James Chen, CMT

Investopedia

James Chen, Chartered Market Technician (CMT), has been a financial market trader and analyst for nearly two decades.