US PCE inflation preview: Gold remains key asset to watch

- Annual Core PCE inflation is expected to rise to 2.9% in April.

- Investors will keep a close eye on US Treasury bond yields.

- Gold looks vulnerable to a deep correction on a strong PCE print.

The US Bureau of Economic Analysis (BEA) will release the Personal Consumption Expenditures (PCE) Price Index data on Friday, May 27. Investors see the PCE inflation retreating to 0.2% on a monthly basis from 0.5% in March and anticipate it edging lower to 2.2% annually from 2.3%. Additionally, the publication will include the monthly change in Personal Spending and Personal income as well.

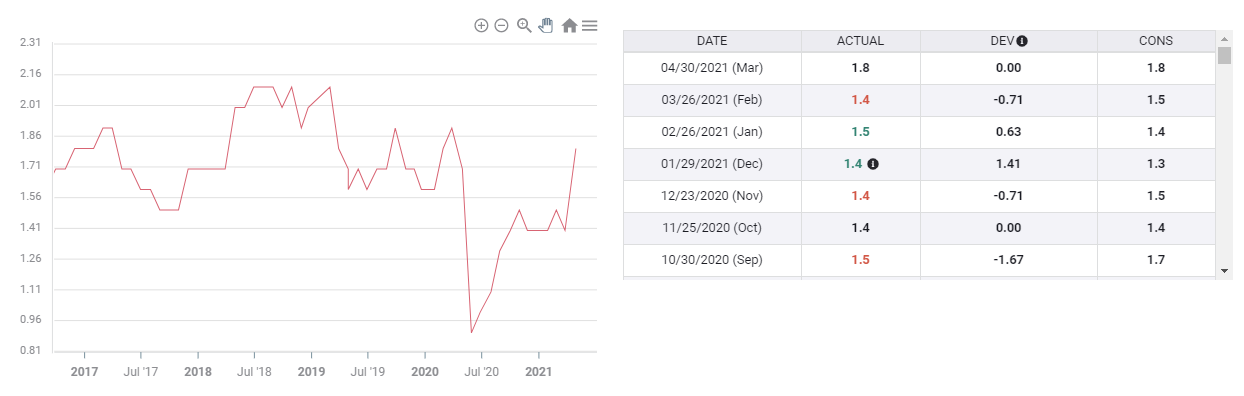

More importantly, the US Federal Reserve’s preferred gauge of inflation, the Core PCE Price Index that excludes volatile food and energy prices, is expected to jump to 2.9% on a yearly basis from 1.8%.

Annual Core PCE Price Index

Inflation expectations continue to impact US T-bond yields

Earlier this month, the US Bureau of Labor Statistics reported that the annual Consumer Price Index (CPI) jumped to 4.2% in April from 2.6% in March. This sharp increase in CPI inflation provided a boost to the greenback and the US Dollar Index rose 0.7% on the day of publication, May 12. On the same day, the benchmark 10-year US Treasury bond yield gained nearly 5%.

Similarly, a higher-than-expected reading in PCE inflation, especially the core version on a yearly basis, could help the USD outperform its rivals as it would cause investors to start pricing a hawkish shift in the Federal Reserve’s forward guidance. On the other hand, the greenback is likely to weaken if the print’s divergence from the market consensus is not significant.

Although policymakers have been downplaying concerns over price pressures, the latest FOMC Minutes revealed that some participants were concerned about inflation rising to ‘unwelcome levels’ before providing sufficient evidence to induce a policy reaction. Meanwhile, Federal Reserve's Vice Chairman Richard Clarida told Yahoo Finance earlier in the week that April’s CPI print was a ‘very unpleasant surprise’ but reiterated that the Fed has tools to bring inflation down if needed. Furthermore, Fed’s Vice Chairman for Supervision Randal Quarles argued that inflation could meet the bar for tapering later this year.

Eyes on gold

Gold, which is generally seen as a hedge against inflation, remains as one of the most sensitive assets to fluctuations in US Treasury bond yields and changes in inflation expectations. After the CPI report, the XAU/USD pair lost more than 1% but didn’t have a difficult time staging a fresh rally. On Wednesday, gold touched its highest level since early January at $1,912 but ended up closing the day in the negative territory a little below $1,900 as the 10-year US T-bond yield gained traction and snapped a four-day losing streak.

Despite Wednesday’s retreat, the Relative Strength Index (RSI) indicator on the daily chart stays above 70, showing that gold is still overbought. The technical outlook suggests that a decline in gold prices on a strong PCE inflation reading is likely to be more severe than an increase supported by a weak PCE print. Moreover, investors could look for an opportunity to book their profits as gold is already up more than 6% in May.

On the downside, the initial support is located at $1,870 (static level). A daily close below that level could pave the way for a deeper correction toward $1,850 (Fibonacci 61.8% retracement of the January-March downtrend).

Strong resistance seems to have formed at $1,900 (psychological level). If gold manages to turn that level into support, $1,912 (May 26 high) could be seen as the next target ahead of $1,930 (static level).

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.