- Consumer Sentiment forecast to reach 90.4 in May, recovering two-thirds of its decline.

- Payrolls, jobless claims, JOLTS show a booming job market .

- Inflation may be a growing concern for consumers.

- Markets have focused on hard numbers, Retail Sales, CPI and NFP.

- Dollar is vulnerable to poor Consumer Sentiment figures.

American consumers should be happy. Jobs are plentiful, wages are rising, the pandemic is wanin, and for the unemployed federal supplementary benefits have been extended to September.

Retail Sales in the first quarter demonstrated an abundant willingness to spend.

Yet there are disquieting conditions too.

Annual US inflation has tripled since January. Parts and labor shortages are making some goods scarce, gasoline prices are nearly 50% higher in six months and the uncertainty created by the pandemic, which is unquelled in much of the world, lingers in school closures and social restrictions in many places. .

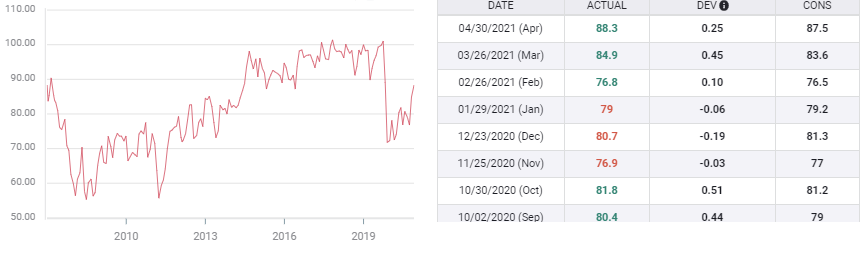

The Michigan Consumer Sentiment Index is expected to rise to 90.4 in May, which would be the third pandemic high in a row, following 84.9 in March and 88.3 in April. Sentiment was 101 last February before the government ordered lockdowns struck the economy in March and April

Michigan Consumer Sentiment

FXStreet

Labor market

There were a record 8.123 million jobs available in March, far more than the 7.5 million anticipated and a sharp increase from the 7.526 million open in February, as reported in Tuesday’s Job Openings and Labor Turnover survey (JOLTS) from the US Labor Department.

JOLTS

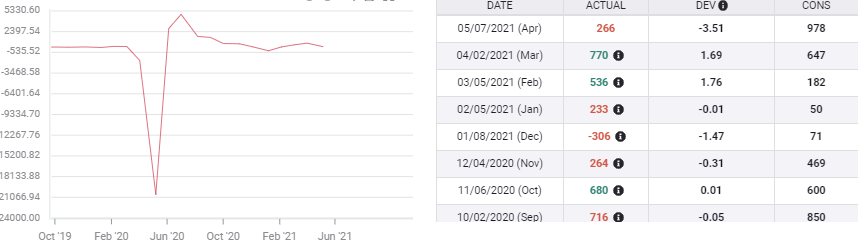

Despite the largest number of unfilled positions in the 21 years of the JOLTS survey, a number that likely increased in April, that month’s seasonally adjusted Nonfarm Payrolls (NFP) added only 266,000 workers, barely a quarter of the one million expected. The unadjusted figures showed 1.089 million new hires.

NFP

FXStreet

This number of job vacancies is consistent with an economy that expanded at 6.4% in the first quarter and that the Atlanta Fed estimates has accelerated to 11% in second.

Several factors may be behind the reluctance of workers to resume employment including, remaining fears over the virus, child-care responsibilities in the states and cities that have not opened their schools and jobless benefits that for some may be as much or more than they could earn.

Initial Jobless Claims dropped to a new pandemic low of 473,000 in the May 7 week as the end of most business restrictions left companies scrambling to fill roles left vacant during the pandemic.

Wages are also rising as firms bid for scarce workers. Annual Hourly Wages climbed 0.7% in April after falling 0.1% in March, no change had been expected. Annual wages rose 0.3%, they had been forecast to decline 0.4%, following March’s 4.2% gain.

Retail sales

Sales averaged 4.8% a month in the first quarter, the strongest consumer performance in over two decades. Washington stimulus payments of $600 in January and $1400 in March provided the wherewithal for the large boost in consumption, but the active job market gave consumers the confidence to spend the largess.

April Retail Sales, released on Friday, are expected to rise 1% after the March burst of 9.8%.

Retail Sales

Inflation

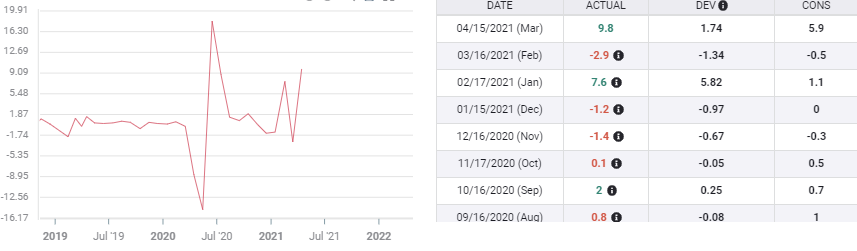

The Consumer Price Index (CPI) has tripled in four months from 1.4% annually in January to 4.2% in April. That is the highest yearly rate in 13 years.

Gasoline, that essential ingredient for the dispersed US population, rose above $3 a gallon on a nationwide average for the first time in seven years in May. Prices for a gallon of gas have jumped 32% this year and 41% since last November 9.

Part of the overall inflation surge this year is due to the comparison with last April’s index, which had plunged in the lockdown spending collapse. But that is not the sole reason behind the galloping price increases.

Commodity and raw material prices have gone up sharply with production unable to meet the demand in many cases. The Bloomberg Commodity Index (BCOM) has gained 17.5% this year, with the steepest gain in the past month as US and global manufacturing firms have sought to ramp up output to meet consumer demand.

BCOM

Price pressures earlier in the production process remain intense, promising that rising manufacturing costs will be passed on to retailers.

The Producer Price Index rose 0.6% in April, double its forecast and following a 1% gain in March. The annual index shot up 6.2%, its largest jump since 2008 and a 365% increase on January’s 1.7% rate.

Conclusion

The Federal Reserve contention that the current price increases are a temporary phenomenon has merit, and the annual gains will drop back once last year’s trough in the index is passed. Likewise the resource and component shortages will pass as the global economy normalizes but even when they do prices are very unlikely to return to the pre-pandemic levels.

For the consumer, looking at a year or more of elevated and rising prices, the derivation is moot.

Inflation is a tax on income and if it persists, it will sap the consumer spending essential to a successful US recovery.

Markets are focused on inflation, if consumer sentiment is lackluster, the dollar and equities will take the hit.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD languishes near multi-year lows below 0.6250 after dovish RBA Minutes

AUD/USD remains depressed below 0.6250 early Tuesday after the December RBA Minutes reiterated that upside inflation risks had diminished, which reaffirms bets for a rate cut in early 2025. This, along with concerns about China's fragile economic recovery and US-China trade war, undermines the Aussie and weighs on the pair.

USD/JPY eases toward 157.00 after Japanese verbal intervention

USD/JPY has come under renewed selling pressure, easing toward 157.00 after Japanese Finance Minister Kato's verbal intervention. The pair erased early gains, induced by the October BoJ meeting Minutes. However, the downside could be limited as the US Dollar hold the previous rebound.

Gold remains stuck between two key barriers amid thin trading

Gold price is attempting another run higher while defending the $2,600 threshold early Tuesday. In doing so, Gold price replicates the recovery moves seen in Monday’s trading, which eventually fizzled out on a broad US Dollar comeback in tandem with US Treasury bond yields.

Solana dominates Bitcoin, Ethereum in price performance and trading volume: Glassnode

Solana is up 6% on Monday following a Glassnode report indicating that SOL has seen more capital increase than Bitcoin and Ethereum. Despite the large gains suggesting a relatively heated market, SOL could still stretch its growth before establishing a top for the cycle.

Bank of England stays on hold, but a dovish front is building

Bank of England rates were maintained at 4.75% today, in line with expectations. However, the 6-3 vote split sent a moderately dovish signal to markets, prompting some dovish repricing and a weaker pound. We remain more dovish than market pricing for 2025.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.