US manufacturers increasingly concerned as Trump tariff optimism fades

US manufacturers are increasingly nervous about President Trump’s tariffs. They’re already disrupting supply chains, and the threat of still more next month looks to be hitting both confidence and future growth. The hope is for production 'reshoring', but that will take years to bear meaningful fruit.

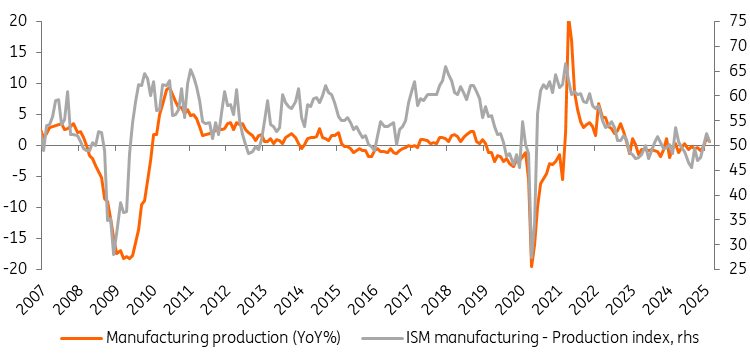

Early soaring sentiment has been reversed

The US economy was in a healthy position late last year with output growing at a near 3% rate, unemployment was low, the Federal Reserve had just cut its policy rate 100bp and equity markets were at all-time highs. The feeling at the time was that President Trump, who had just been elected, would boost the growth outlook further by slashing regulations and cutting the tax burden. Manufacturers were potentially going to be big winners with a proposal to cut Federal corporation taxes to just 15% while President Trump was keen to drive a revolution of reshoring of manufacturing to the US.

The result was soaring sentiment with the ISM manufacturing index’s production and new orders components returning to positive territory for the first time in two years.

ISM manufacturing survey and manufacturing production (YoY%)

Source: Macrobond, ING

However, the Administration has instead initially focused on immigration controls, government spending cuts and threats of trade protectionism, all of which create challenges in the near term for manufacturers. Threats of tariffs have already been used as a tool to incentivise foreign countries to comply with US demands in areas ranging from drug trafficking and border controls to defence spending.

President Trump has since announced 25% tariffs on steel and aluminium, impacting $200bn of imports and followed this up with an announcement of 25% tariffs on auto imports that totalled over $400bn in 2024. Tariffs will be expanded further on 2 April as President Trump seeks to rebalance trade in favour of US manufacturers. Dubbed “Liberation Day”, he will announce his plans regarding reciprocal tariffs for countries that the Administration believes are unfairly treating US companies.

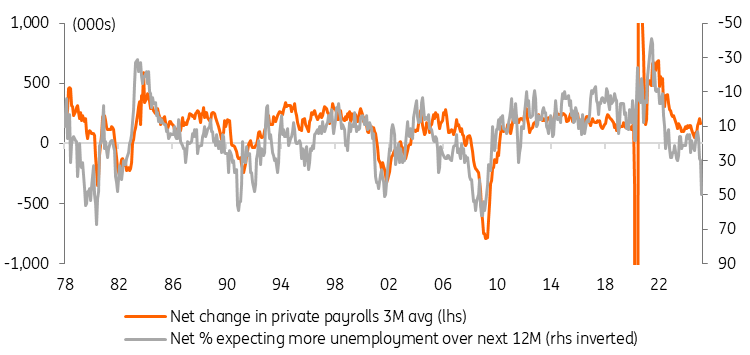

The threat of tariffs is already prompting concerns about higher prices that could squeeze consumer spending power. Additionally, households are worrying about the impact of the Department of Government Efficiency's spending cuts on jobs and entitlements. Falling equity markets have been adding to consumer fears for the economic outlook, with sentiment sliding sharply.

Households are much more pessimistic on the jobs market outlook

Source: Macrobond, ING

Manufacturers themselves are nervous. A sense of a weaker corporate profits environment due to cooling consumer demand and higher tariff costs is hurting sentiment, which in turn threatens reduced near-term investment and hiring. There is also a fear that uncertainty means a 'risk-off environment,' which results in wider credit spreads and higher corporate borrowing costs that further deter companies from putting money to work.

As such, economists have been downwardly revising US growth forecasts. Our own 2025 GDP prediction was scaled back from 2.5% in January to 2.1% in our March update, while the Federal Reserve has likewise revised its 2025 growth projection downwards by 0.4 percentage points.

2018 tariffs failed to boost growth or jobs

President Trump argues that unfair foreign competition has led to offshoring and job losses, causing social deprivation in parts of America. He thinks radical action is needed and believes tariffs can make US manufacturing prices competitive, encourage reshoring, and generate tax revenue for cuts elsewhere. Manufacturing's role in the US economy has declined for decades, from over 30% of workers in the 1950s to 8% today, with technology and automation driving job losses. Higher US production costs have led to offshoring, and wealthier Americans tend to spend more on services than goods. In 2018, Trump imposed tariffs, particularly on China, but loopholes allowed some production to be diverted to third-party nations, such as Vietnam and Korea. These actions failed to generate any meaningful improvement in US manufacturing performance, with the output volumes actually down 0.25% from where they were at the beginning of 2018; unemployment levels were unchanged.

Despite this, President Trump is doubling down, now implementing broader, more aggressive tariffs.

Broader tariffs means more pain this time

President Trump has claimed that “foreigners will pay” tariffs, despite the fact that the importing company pays the tariff when it arrives at a US port. The argument that the Administration uses is that if they introduce a 10% tariff and if the dollar appreciates 10% then this will mean that there is no price change for the US importer as the two will offset. Foreigners therefore pay through a loss of purchasing power via a weaker currency versus the USD.

Theoretically, that is possible, but if we look at the numbers today, it clearly doesn’t work. Administration officials and Donald Trump himself suggest that the average tariff rate charged on imports will fall within the 10-25% range. With the USD only having appreciated 3.5% on a trade-weighted basis since September, there will inevitably be higher costs for US importers unless they can convince the foreign producer to meaningfully cut their prices. If importers cannot convince foreign companies to bear the cost of the tariff, the choice will be some combination of tighter profit margins for US companies and passing part of the higher costs onto the US consumer.

Reshoring can't be achieved overnight

Now, US companies could, of course, choose to use US-made products instead of importing foreign goods, but this is not going to be possible for everything. The US imported $3.3tn worth of goods in 2024, yet the total value-added of US manufacturing as measured within the GDP report was just under $3tn. Therefore, the US manufacturing sector would need to more than double in size to remove the need for any imports. While that suggests huge scope for manufacturing expansion via reshoring, it can’t be achieved overnight and indicates the US economy will face higher costs.

In terms of the sectors set to be most impacted, the US imported $474bn of automotive vehicles, parts and engines in 2024, nearly $300bn of computers, computer accessories and semi-conductors, $62bn of civilian aircraft, parts and engines, $112bn of cell phones and $247bn of pharmaceutical preparations.

20% universal tariffs could cost every American $2000

While we need to wait for the 2 April announcement, if we assume all $3.3tn of imports are subject to a 20% tariff on average, then this would raise $660bn in revenue. Total consumer spending amounted to just under $20tn in 2024, and so if there is complete pass through of the cost to the consumer, then that same amount of purchases would now cost $20.66tn. This implies an approximate 3.3% increase in prices or an extra $2000 of annual costs for every single American!

We know that when washing machines were subject to a 20% US tariff in 2018, around 60% of the tariff appears to have been initially passed onto the consumer based on the numbers published within the consumer price report. If we see something similar this time around – and the importer and foreign producer absorb 40% of the tariff – then price levels in aggregate may rise a more modest 2%. However, in 2018, it was on a specific product and importers and retailers may have taken the view that they could afford to absorb some of the cost as they would still be making ample profits on other products.

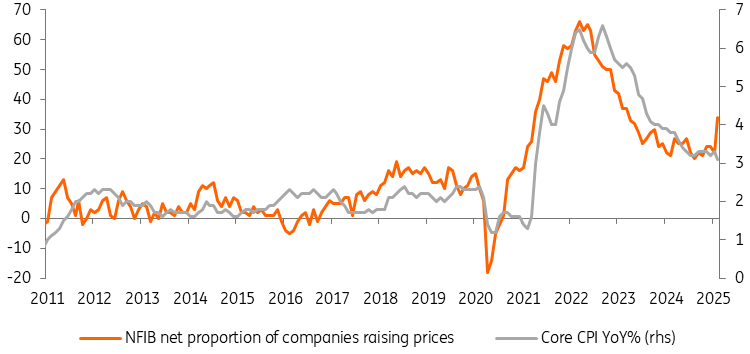

When the tariff is on everything, that will not be as easy, hence why we suspect it is more likely to be an 80%+ pass through to the consumer. Note that the National Federation for Independent Businesses has indicated members are pre-emptively raising prices and this is also evident in other business surveys, including the ISM’s purchasing managers’ indices, especially for long-term contracts.

Households are nervous about what this means for their spending power and in an environment of government austerity, which is casting a cloud over the outlook for the US jobs market, the risks are skewed towards weaker consumer spending. In turn, this points to softer demand for US-manufactured products.

Companies are pre-emptively raising prices

Source: Macrobond, ING

US exporters are vulnerable to foreign actions

The added concern for US manufacturers is that foreign governments may implement reciprocal tariffs that hurt the price competitiveness of US-made products in those markets. In 2024, the US exported around $2.1tr of manufactured goods, the largest categories being automotive and parts ($169bn), civilian aircraft, parts and engines ($124bn), pharmaceuticals ($107bn) with medical equipment, crude oil, chemicals and technology-related products also making significant contributions. Further complicating the situation are concerns about foreign consumer boycotts tied to both tariffs and President Trump’s other policy aspirations, including absorbing Canada and Greenland into the US, withdrawal of support for Ukraine and perceived support for Russia.

How this plays out is critical for the US manufacturing sector. A positive scenario is that an escalation of trade tensions actually leads to an eventual de-escalation. With most countries running a trade surplus with the US they fear a big drop in exports will hurt growth and jobs in their own country and they scale back tariff and non-tariff barriers applied to US goods. The US then withdraws its tariffs, delivering a more positive environment for global trade with fewer costly barriers to foreign markets.

A worst-case scenario is that trade partners respond with additional tariffs and the US responds again leading to an all-out trade war. With prices rising rapidly around the world this leads to steep declines in sentiment and spending. Stagflation is the result and central banks respond with higher interest rates that tips the global economy into recession.

We are not confident that other countries will be willing to scale back tariffs meaningfully and open up their markets to US products. An obvious stumbling block is the export of US agricultural products into Europe. We have also repeatedly heard that the US Administration believes it can raise billions, if not trillions of dollars in tax revenue from tariffs that can be funneled back to consumers via income tax cuts. Consequently, they may be reluctant to de-escalate the situation quickly, especially given the long-run goal of reshoring.

Moreover, President Trump has talked of an adjustment period and signalled that he is prepared to tolerate short-term economic pain in the hope of delivering a more positive path forward for the US manufacturing sector over the longer term. This means that we should be braced for weaker output later in the year.

The case for reshoring grows – But only for high value products

With more barriers to trade and higher costs, the case for reshoring at least some activity to the US looks increasingly strong. However, US manufacturing wages are amongst the highest in the world – the National Association of Manufacturers states that in 2023, manufacturing employees earned an average of $102,629, including pay and benefits. For China, it is around 25%, and for Korea, it is around 40% of that figure. Even in Germany, it is less than 75% of the US figure. This suggests that it would only make sense to reshore activity related to highly automated, high skill, high value-added production or for products where there is a strong market that consumers are willing to pay a premium for a 'Made in America' label.

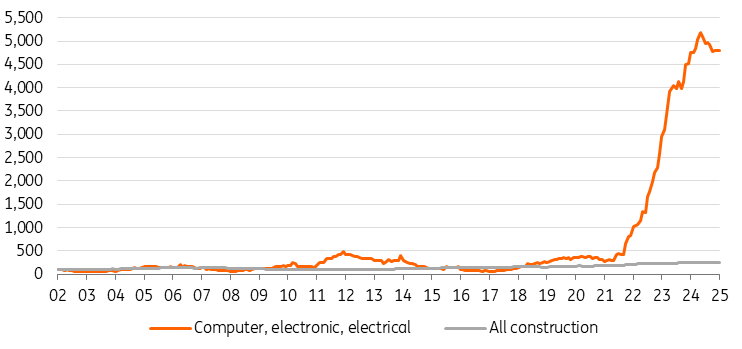

We are already seeing this with construction spending tied to semiconductor technology manufacturing up nearly 14-fold since the pandemic struck. This has been encouraged through President Joe Biden’s incentives to reshore semiconductor manufacturing through the CHIPS Act of 2022 (Creating Helpful Incentives to Produce Semiconductors). This has been supplemented by the Innovation and Competition Act, which authorised $110bn for technology research. Construction of data centres has also been particularly robust, and the excitement about advances in Artificial Intelligence will mean more investment and construction tied to this.

Outside of the hi-tech sector, construction activity tied to manufacturing has been respectable, but far more modest, up a little over 150% since the depths of the pandemic.

Technology-related construction has severely outpaced broader manufacturing-related construction

Source: Macrobond, ING

Pharmaceutical production is another area where we are already seeing announcements of investment in the US. Johnson & Johnson have announced a $55bn investment spending plan within the US over the next four years with Eli Lilly announcing a $27bn investment in its US manufacturing operations.

Nonetheless, it does take significant time to build a manufacturing plant, with Intel suggesting that for one of their plants, it takes three to five years with 6000 construction workers at a cost of $10bn. This is at the extreme end of the spectrum, but an aluminium smelter takes 2-3 years for construction in addition to the time taken to design and receive planning approval. Significant infrastructure is also typically required for all new manufacturing sites, including power, road, rail and water, which will add to the cost of reshoring.

Given the costs of moving production to the US – construction and workforce predominantly – it may be that many manufacturers decide that it is cheaper to keep production facilities where they are and just absorb the tariff within operating costs. Furthermore, some manufacturers may take the view that in time, there is scope for deals to be reached between the US and trade partners, with a chance that tariffs are scaled back. Others may make a bolder call and believe that when President Trump’s term ends in just under four years, a new president may take a different view on the effectiveness of trade tariffs and they are scrapped.

Therefore, we take a relatively conservative line that reshoring is likely to be concentrated in relatively high value-added sectors, which make up between 10% and 15% of total US imports. Nonetheless, the additional trade barriers mean that there is less incentive to offshore production, so future plants oriented to the US market are likely to be built in the United States. Given the time frame for planning and construction, we do not see the reshoring story boosting US manufacturing output notably until 2027 onwards.

Rising reshoring for more energy and infrastructure needs

Megatrends in energy and infrastructure are driving increased manufacturing activities. Rapid AI adoption is leading to the swift construction of data centers and related equipment, boosting energy demand and requiring enhanced power transmission lines and new power generation facilities. The Trump administration's focus on expanding US energy dominance and industrial competitiveness is increasing the appeal of manufacturing these in the US.

AI and infrastructure trends are also promoting domestic clean energy production. Reshoring clean energy already started under the Biden administration's Inflation Reduction Act and the Infrastructure Investment and Jobs Act, which attracted over $100bn in clean energy manufacturing investments.

Trump's tariffs on steel, aluminum, and Chinese imports are raising costs, but may further encourage reshoring. Clean energy manufacturers might renegotiate contracts, absorb higher prices with IRA tax credits, pass costs to consumers, or invest in US factories for a resilient supply chain. This transformation, however, will take considerable time.

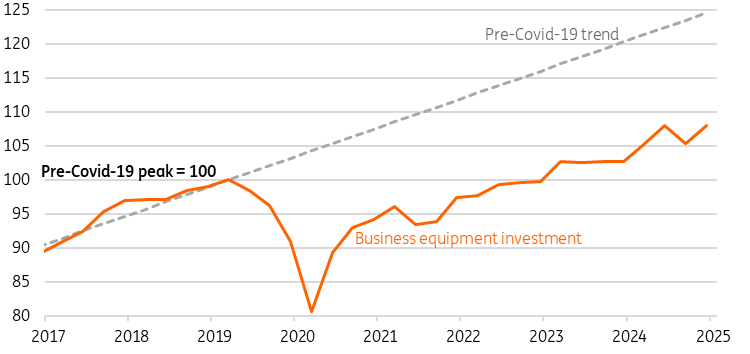

Tied to the reshoring story, a notable area of disappointment in the post-pandemic US growth story has been the weakness in business equipment investment. Volumes are tracking around 15% below the pre-Covid trend and accounting for inflation, there is scope for this to rebound by more than 25% over the next couple of years, equivalent to an extra $375bn of investment spending on industrial, IT, transport and other equipment. Reshoring would likely accelerate this situation.

Business equipment investment has been a real weak spot for the economy (Volumes 2Q2019 = 100)

Source: Macrobond, ING

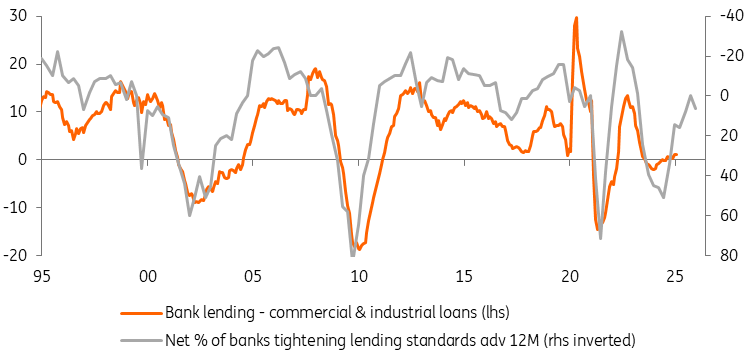

For the sector, lending conditions have improved significantly over the past 12 months. The chart below shows that the Federal Reserve’s Senior Loan Officer Opinion survey on lending standards has a good lead quality for the year-on-year change in outstanding bank lending for commercial and industrial loans. It suggests lending growth to corporate America will turn positive, although the uncertain economic environment caused by tariffs may limit the pace of growth in the near term.

Banks willingness to lend to the sector is on the rise

Source: Macrobond, ING

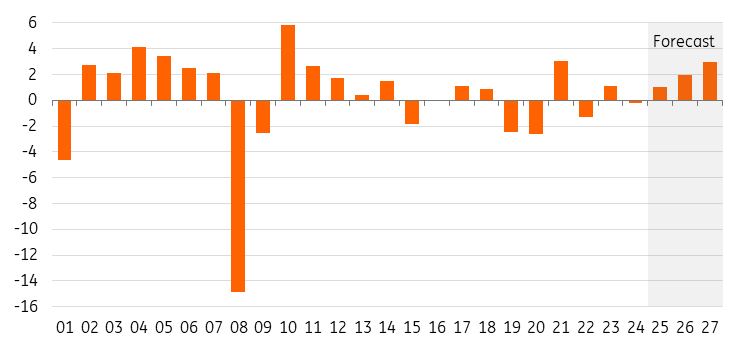

Right now, the future for US manufacturing is pretty bleak and, let’s not forget, it’s been struggling for several years; output in volume terms is barely 1% higher than before the Covid pandemic - just look at the chart below.

US manufacturing output YoY%

Source: Macrobond, ING

Gven the threat of retaliatory tariffs from trading partners, we’re scaling back our growth expectations for manufacturing output to 1% from 3% for this year. It’s hardly the economic miracle that President Trump and many Americans are hoping for.

Read the original analysis: US manufacturers increasingly concerned as Trump tariff optimism fades

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.