US labour market: Slowing but steady

We expect early April labour market data to continue signalling cooling, but still steady growth. Federal layoffs and sharply cooling immigration are set to weigh on employment growth over coming months, but the low number of jobless claims on the private sector suggests overall conditions remain stable.

We think that this week's March Jobs Report will show nonfarm payrolls (NFP) growth slowing to just 110k. Unemployment rate will likely tick higher to 4.2% but we do not expect to see a much further increase in the near-term given the tightening labour supply.

Last month's report was a mixed bag, as NFP growth remained at 151k despite the apparent headwinds. The participation rate edged down to 62.4% from 62.6%, but decomposing the figure reveals that the downtick attributed to an outflow of workers in the categories "55 years & over" and "20 to 24 years", while the prime-age participation rate remained at 83.5%.

The January JOLTs report was also solid, with job openings ticking higher to 7.7m (cons: 7.6, prior: 7.5m), and involuntary layoffs continuing their downward trend for the fourth consecutive month, reaching 1.6m (prior: 1.7m). Coupling this with jobless claims and the WARN advance notifications for mass layoffs hovering at modest levels, labour market conditions appear to remain steady.

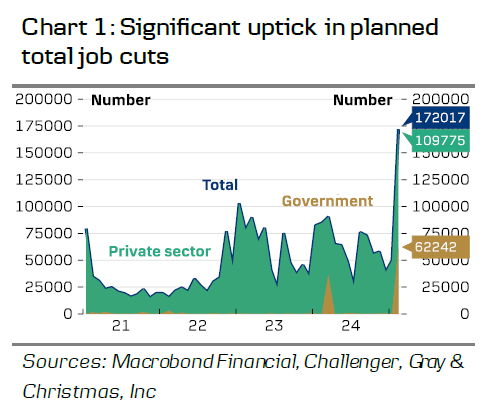

In light of the DOGE-related layoffs, the February jobs report pointed towards only a muted impact so far. This could, however, be due to the BLS survey reporting period ending before the settlement of the layoffs. Looking at the Challenger report for planned layoffs by US firms, the picture is quite different, with 172k announced job cuts in February (chart 1). Reductions on the public sector accounted for around 62k, but private sector numbers were up as well, perhaps due to cancelled government contracts and fear of trade wars. We recommend keeping an eye out for the upcoming March Challenger report, which could provide further clarity on the scale of DOGE's federal layoffs.

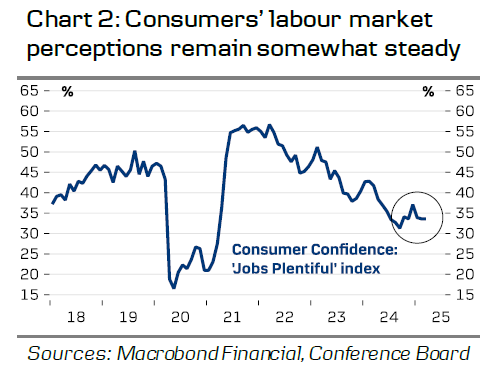

Consumer confidence continues to deteriorate, hitting the lowest level since 2013. Consumers have reported especially their future employment prospects weakening - potentially due to the uncertainty related to job cuts and higher inflation expectations. However, consumers' perception of current labour market conditions remains steady (chart 2), suggesting that the situation might not be as dire as what the headline shows.

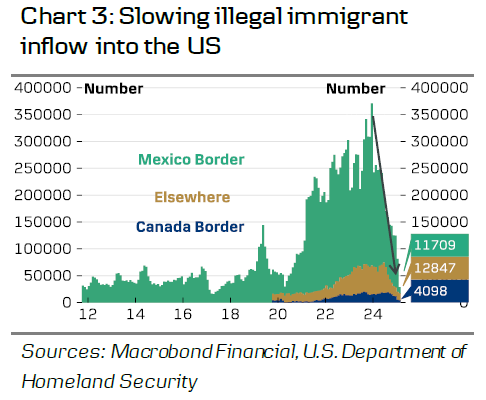

While immigration has been the most important driver of labour supply growth in the past years, the situation has changed completely (chart 3). Immigration slowed at a record pace, with illegal border crossings declining to just 28k in February, lower than during peak COVID-restrictions. With native-born labour force growth set to structurally decline, labour supply alone is likely to become a drag on potential growth. Notably, the effect is already evident in labour market readings, as the flow of workers from outside the labour force and into employment has slowed steadily over the past year.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.