US labor market strong, but not overheated

Pandemic has changed labor market

As one of two Fed targets, developments in the US labor market naturally get a lot of attention from the markets. Cooling of the labor market will likely be a consequence of rate hikes to achieve the inflation target, but it is not a prerequisite. The labor market is not overheated and, on the whole, has developed during the last few years as economic growth would have suggested. The US economy grew 5.5% in real terms from the onset of the pandemic in early 2020 through 1Q23, and employment grew 2.4% over the same period. Productivity grew at nearly the same rate as in the years before the pandemic, also providing no evidence of overheating. Even though wage growth is still historically high, this has to be seen in the context of inflation, which is also historically high. Even the Fed, however, does not see a wage-price spiral.

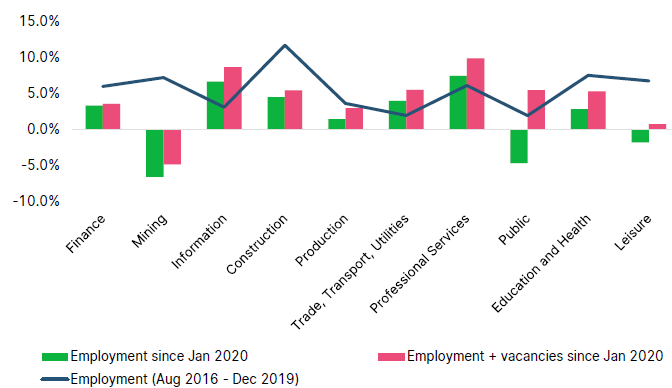

However, the labor market is different now than it was before the pandemic. This is due to shifts within the labor market that were triggered by the pandemic and have not yet been reversed. In the graph, we have shown the growth of employment in each sector. In addition, we have calculated what the growth rate would be if all additional vacancies were filled. Finally, as a reference value, we show the growth for the period of the same length before the outbreak of the pandemic.

The most obvious impact of the pandemic has been on the leisure sector, which has suffered greatly. Meanwhile, sales in the sector have recovered and have even grown slightly faster than the overall economy since 2020. However, employment is lagging significantly and is still lower than it was before 2020. Obviously, many workers have been absorbed into other sectors of the economy that showed high employment growth during the pandemic. The surprise is that as the pandemic subsided, these sectors did not see their

Employment growth by industry sector, in %

Source: Bureau of Labor Statistics, Erste group Research

The most obvious impact of the pandemic has been on the leisure sector, which has suffered greatly. Meanwhile, sales in the sector have recovered and have even grown slightly faster than the overall economy since 2020. However, employment is lagging significantly and is still lower than it was before 2020. Obviously, many workers have been absorbed into other sectors of the economy that showed high employment growth during the pandemic. The surprise is that as the pandemic subsided, these sectors did not see their employment numbers return. Three sectors stand out. Information, transportation, trade and utilities, and business services. Here, employment growth since the outbreak of the pandemic has been significantly higher than in the same period before the pandemic, which also showed higher overall economic growth of 8.4%. For delivery services, this can be explained as the increase in online trade is arguably permanent. In the case of accounting services, on the other hand, to name just one other group, the sharp rise in employment is not immediately apparent. Overall, however, these shifts are likely to be mostly lasting.

With unemployment rates near historic lows, the labor market is certainly tight. At the same time, however, employment growth has already slowed down considerably and is taking place primarily in the public sector and in health care and education. In both areas, underperformance since the outbreak of the pandemic plays a major role. This pent-up demand should continue to support the labor market for some time, but we think it is unlikely that the overall market will overheat as a result.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.