US Inflation Preview: Stocks set to surge if reality fails to meet high Core CPI expectations

- Economists expect Core CPI to have risen by 0.3% for the second consecutive month.

- Headwinds in the economy suggest underlying price rises may have decelerated.

- The Federal Reserve's focus on inflation means volatility is set to be sky-high.

To cut or not to cut in March? That is the question investors ask the Federal Reserve (Fed) – which says it is data-dependent. The inflation report is the No. 1 economic figure in recent years, providing the biggest clue of all. The report is set to trigger higher volatility than the Nonfarm Payrolls.

Here is a preview of the United States Consumer Price Index (CPI) for December, due on Thursday at 13:30 GMT.

Inflation last mile is the hardest

The headline Consumer Price Index (CPI) fell from the peak of 9.1% to 3% in the following year as global supply chains unsnarled and the Federal Reserve's rapid clip of rate hikes curbed demand. However, annual prices have hovered above the 3% mark since then, hitting 3.1% YoY in November. A minor increase to 3.2% is on the cards for December.

The Federal Reserve and investors closely follow Core CPI, which excludes volatile items such as food and energy. This is because the central bank can better control lending and investment via the interest rate tool than Oil prices, which are set in global markets.

Core prices are "stickier" – for example, wages of service providers such as beauty salon workers and lawyers do not easily fall. Underlying inflation stood at 4% YoY and is now set to drop to 3.8% – still substantially above the "holy grail" of 2%.

Core CPI YoY. Source: FXStreet

Disinflation was significant enough for the Federal Reserve to stop raising rates and signal more cuts than earlier forecast for 2024. However, Fed Chair Jerome Powell and his colleagues deliberately refrained from stating when the first loosening will occur. "Data dependent" remains the Fed's mantra.

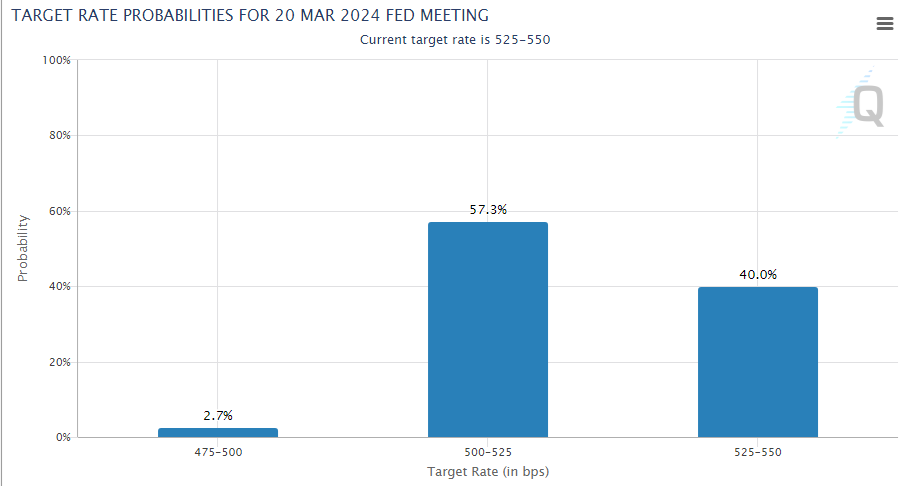

Markets ran with the Fed's dovish pivot, pricing as many as six cuts this year, double the Fed's estimates. Moreover, bond prices reflect an almost 60% chance of a rate cut as soon as in the March meeting. That may be too much, but a soft inflation figure would fuel the market fire.

March 2024 interest rate pricing. Source: CME FedWatch Tool

CPI expected market reactions

The first reaction tends to come from the Core CPI MoM, which reflects the latest moves in the figure that matters most. The economic calendar points to a second consecutive increase of 0.3%, which reflects an annualized rise of roughly 3.6%. That would call for further patience before cutting rates and perhaps a fresh climbdown for stocks, in addition to the battering in the first week of 2024. The US Dollar would further recover.

But, it would take just one-tenth, an increase of 0.2%, to reflect a more benign 2.4% annualized increase and to trigger hopes of a March cut firmly on the table. Stocks would rally, and the Greenback would grind lower, both resuming the trends of late 2023.

In both scenarios, other figures would also have a say, most importantly headline CPI YoY, which is the most cited figure by non-financial media. A stronger figure would enhance a stock sell-off in case of a 0.3% read in Core CPI MoM and would limit the rally in case of a 0.2% read. Conversely, a softer headline CPI YoY would cushion the blow from a 0.3% Core CPI MoM read, and it would further buoy stocks in case the monthly core figure is only 0.2%.

A substantial increase of 0.4% in Core CPI would hurt markets and boost the US Dollar, regardless of other data. A shock 0.1% increase – improbable, but cannot be ruled out – would trigger a market party and hit the Greenback hard.

Final thoughts

It is hard to exaggerate the importance of the CPI report, especially as uncertainty about the first rate cut since 2020 looms. Markets are energetic at the beginning of the year, increasing the risk of high volatility. I recommend trading with lower leverage around this critical event.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.