U.S. GDP: As Expected, First Quarter Slowdown—But Modest

First quarter 2018 GDP came in at 2.3 percent, an expected slowdown but less than feared given persistent seasonality issues. Consumer spending and business investment were slower and inflation continues to rise.

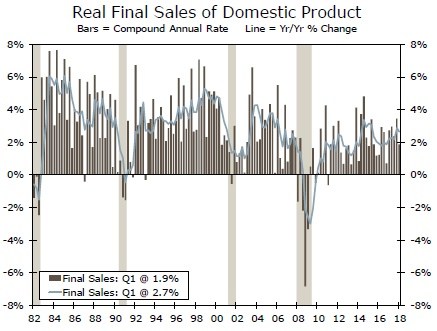

Real Final Sales: Q1 Slowdown—But Modest by Expectations

Real private final sales came in at 1.9 percent (2.7 percent year over year, top graph) with gains in consumer and business spending. Overall GDP came in at 2.9 percent year over year compared to 2.0 percent for Q1 2017— clearly a nice improvement. We expect GDP growth of 2.6 percent in 2018 compared to 2.3 percent in 2017.

Real consumer spending increased at a 1.1 percent annual pace in Q1, below the recent trend. The slowdown reflected a decline in durables spending, including motor vehicles which, in turn, may reflect the impact of hurricane recovery spending in the fourth quarter. Continued gains in consumer spending are expected given improvement in the labor market, compensation, consumer confidence and household wealth. For 2018, we estimate consumer spending to be up 2.5 percent.

Residential construction was flat, but government spending, both federal and state & local, contributed to growth. Residential investment is facing some headwinds as interest rates and land prices increase. Despite the notsostellar growth in housing starts, demand for apartments remains strong.

Trade reflected an improvement in export growth compared to a year ago and was a net addition to GDP in the quarter. For 2018, however, we expect trade to subtract from GDP. Inventories also positively contributed to GDP in the first quarter and are more in line with the gains in final sales—we expect inventories to add to GDP for all of 2018.

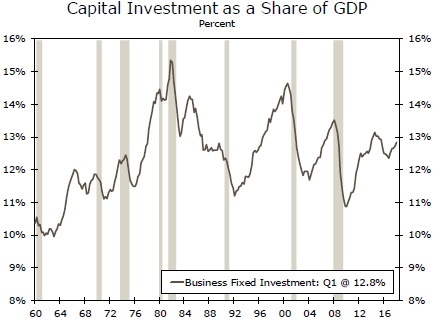

Capital Investment: Now and Over the Cycles

To achieve improved economic growth at 3 percent, the economy needs better equipment with better trained workers. Business fixed investment rose 4.7 percent while structures improved 12.3 percent—and are up year over year. This is a good sign for growth. As illustrated in the middle graph, the pace of capital investment has moderated as a share of GDP since the early 1980s. This is consistent with a moderation in productivity gains. Over the past three quarters, however, we have seen gains in spending on information processing, industrial and intellectual property segments.

Inflation: Rising—So Will the Fed Funds Rate

Overall GDP inflation came in at 2.0 percent in the fourth quarter while the core PCE deflator, the Fed’s benchmark, was up 2.5 percent compared to just 1.8 percent a year ago. Services are the culprit here, with a gain of 3.1 percent compared to 2.0 percent in Q1 2017. Services inflation has outpaced goods inflation throughout the 2015-2017 period. Rising inflation and continued moderate economic growth provide the basis for a FOMC decision to raise the funds rate in June. Our outlook is also for rising 2- and 5-year Treasury rates in response. Our model is for a flatter yield curve for this year.

Author

Wells Fargo Research Team

Wells Fargo