US: Economic resilience despite higher rates, the role of household finances

In the US, household deleveraging, fixed rate mortgages, rising financial income on the back of higher interest rates and dividends, in combination with an increase in net worth have contributed to the resilience of households in an environment of aggressive monetary tightening. Nevertheless, some caution is warranted. Aggregate data, by construction, do not shed light on the heterogeneity of households. The financially fragile categories will need to be monitored closely in an environment of high rates for longer, in view of possible spillover effects to the broader economy should their situation worsen significantly.

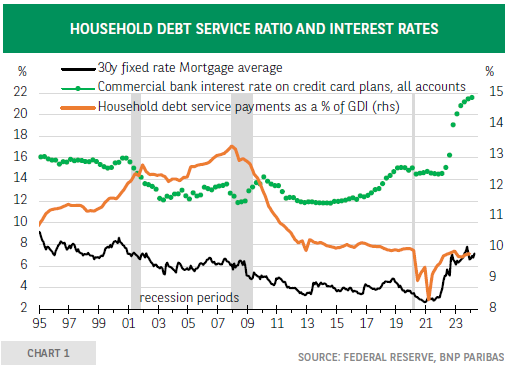

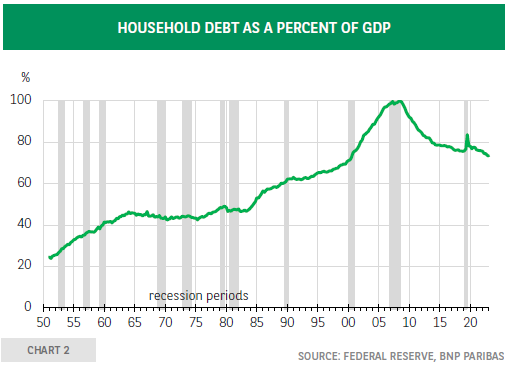

Faced with a swift and huge policy tightening by the Federal Reserve, the US economy has been surprisingly resilient. Household spending has played an important role in this respect, underpinned by the run-down of excess savings accumulated during the pandemic, the pace of job creations and strong wage growth. The financial situation of households has also helped. Despite a jump in interest rates on mortgages and credit card balances, the debt service -which includes principal repaymentsin percent of disposable income has been stable in recent years (chart 1), reflecting the beneficial impact of household deleveraging in previous years. Indeed, after peaking at 100% in the first quarter of 2009, household debt as a percent of GDP has been on a downward trend -only briefly interrupted by the drop in GDP during the pandemic- to reach 73.5% in the third quarter of 2023, the latest available data (chart 2). This stands in sharp contrast with the experience in the run-up to the recessions starting in March 2001 and December 2007, when the debt service ratio recorded a significant increase. Household resilience has also benefitted from the fact that the bulk of mortgage debt outstanding has been contracted at fixed rates. Based on data from the 2019 survey of consumer finances, “about 40% of U.S. households have mortgages, of which 92% have fixed rates and the remaining 8% have adjustable rates.1” This protects households from an increase in mortgage rates and the latter essentially influence the economy through the demand for new mortgages2.

When analysing monetary transmission, the focus tends to be on the negative impact of higher interest rates. However, the latter also generate an increase in financial income and, as shown in chart 3, this has largely shielded households from the impact of higher interest payments on non-mortgage debt3. In addition, household net worth, after a dip in 2022, has increased strongly since and is now at a record high. In real terms, the jump in inflation caused a large drop in 2022 before increasing again (chart 4). Testimony to a resilient economy, personal dividend income has continued to increase in recent years after rising very strongly in the aftermath of the pandemic (chart 5).

To conclude, household deleveraging, fixed rate mortgages, rising financial income on the back of higher interest rates and dividends, in combination with an increase in net worth have contributed to the resilience of households in an environment of aggressive monetary tightening. Nevertheless, some caution is warranted. Aggregate data, by construction, do not shed light on the heterogeneity of households. Some benefit from high interest rates whereas others suffer, and the Federal Reserve is of course aware of this issue. Quoting from its latest Financial Stability Report, “some borrowers continued to be financially stretched, and auto loan and credit card delinquencies for nonprime borrowers increased4 , although it should be added that delinquency rates are still low compared to history (chart 6).

The financially fragile categories will need to be monitored closely in an environment of high interest rates for longer5 in view of possible spillover effects to the broader economy should their situation worsen significantly.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.