US Dollar Forecast: Uncharted territory

- The US Dollar Index finished the week deeply in the red.

- Trump's “Liberation Day” rippled across the globe.

- Next of note on the US calendar will be the Inflation Rate.

After a forgettable week, the US Dollar (USD) lost its grip, adding to the previous decline and succumbing to the sharp selling pressure that eventually sent the US Dollar Index (DXY) to the 101.30-101.20 band for the first time since early October 2024.

The steep decline in the index gathered renewed and firm pace after President Donald Trump unveiled his so-called “Liberation Day” on Wednesday, which has also reinforced the prospects of a transatlantic trade war and has lent extra legs to the idea of a US economic slowdown.

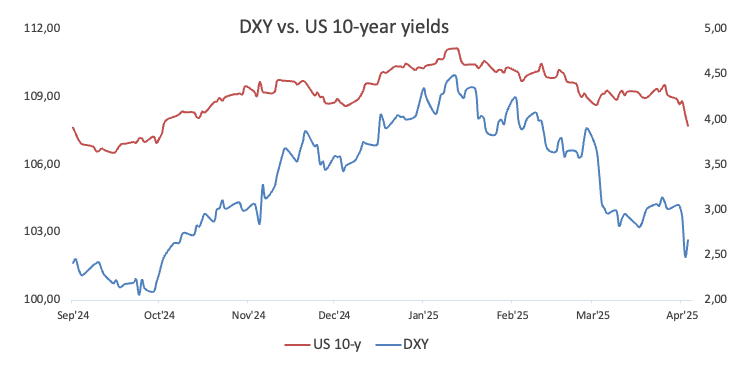

The Greenback’s intense move lower came in tandem with the equally pronounced retracement in US Treasury yields across various time frames.

Winds of change: Confronting trade turbulence and escalating prices

In a game-changing move, the United States unveiled its “Reciprocal Tariff to Rectify Trade Practices” plan on Wednesday.

Under this new policy, a baseline 10% tariff will apply to all imports, with additional country-specific surcharges ranging from 10% to 50%. That said, China faces a steep 34% levy on top of its existing 20% duty, while the European Union (EU) is subject to 20%, the UK to 10%, and Japan to 24%. The baseline tariffs will come into effect this Saturday, with the extra “reciprocal” rates following on April 9.

In addition, Mexico and Canada remain exempt from these reciprocal tariffs for now, thanks to a standing 25% blanket levy on any US imports not covered by the United States-Mexico-Canada Agreement (USMCA). Cars, auto parts, steel, and aluminum also stay in the clear, as they’re already taxed at 25%.

Although China, the EU, and several other countries have vowed to fight back, US Treasury Secretary Scott Bessent issued a stark warning: “I wouldn’t try to retaliate… As long as you don’t retaliate, this is the high end of the number.”

So, what’s the reasoning behind tariffs? Initially, higher import duties tend to trigger a short-lived spike in consumer prices—a one-time shock that’s unlikely to immediately force the Federal Reserve’s (Fed) hand. However, if these tariffs stick around or escalate, businesses might have little choice but to keep prices elevated, whether because competition dwindles or they seek larger margins.

This second wave of price hikes could eventually slow consumer spending, dampen economic growth, hit employment, and even revive deflationary risks. Over time, these cascading effects might push the Fed toward more forceful policy measures.

Steering through economic deceleration and rising inflation

The increasing weakness surrounding the US Dollar has been spurred by growing speculation of an economic slowdown, fueled by newly announced tariffs, tepid results from US fundamentals, and eroding market confidence.

While inflation still runs above the Fed’s 2% target—evident in both CPI and PCE figures—a resilient and robust labor market adds an intriguing twist to the story.

In the end, this blend of factors, combined with rising uncertainty over the impact of US tariffs both domestically and overseas, is expected to maintain the volatility in the Greenback, leaving conditions anything but mitigated.

Measured moves: The Fed’s prudent response to market uncertainty

On March 19, the Federal Reserve wrapped up its meeting by keeping the federal funds rate anchored between 4.25% and 4.5%.

Citing heightened uncertainty—from shifting policies to rising trade tensions—the Committee opted for a cautious stance. At the same time, it revised its 2025 forecasts, lowering real GDP growth from 2.1% to 1.7% and nudging inflation expectations up from 2.5% to 2.7%. These adjustments highlight growing worries about a stagflation threat, where slow growth intersects with higher inflation.

During his customary press conference, Fed Chair Jerome Powell reiterated that there is no immediate need for additional rate cuts.

In a flurry of insights from top Federal Reserve officials, policymakers painted a picture of cautious optimism amid mounting economic risks.

That said, New York Fed President John Williams noted that policy is "well positioned" and "moderately restrictive," allowing for careful data monitoring before any rate changes.

Richmond Fed President Thomas Barkin and Chicago Fed President Austan Goolsbee both highlighted inflation risks from tariffs, with Barkin emphasizing that rate cuts would depend on inflation trends and Goolsbee warning that new tariffs could spark renewed inflation or slow growth.

Fed Governor Adriana Kugler and Vice Chair Philip Jefferson also stressed that until inflation risks subside, keeping rates steady is the prudent course of action, while Fed Governor Lisa Cook urged the Fed to wait and watch emerging data before making further adjustments.

In addition, Federal Reserve Chair Jerome Powell warned on Friday that President Donald Trump's new tariffs are "larger than expected," and he predicted that the resulting economic fallout—including higher inflation and slower growth—will likely be just as significant. He remarked, "We face a highly uncertain outlook with elevated risks of both higher unemployment and higher inflation," a scenario that could jeopardise the Fed's twin mandates of 2% inflation and maximum employment. He emphasised that while it isn’t the Fed's role to critique the Trump administration's policies, its duty is to react to their impact on an economy that, only weeks ago, was enjoying a "sweet spot" of falling inflation and low unemployment

The road ahead for the Greenback

Next week, all eyes will be on the release of the US Inflation Rate figures and the unveiling of the FOMC Minutes from the March 18-19 meeting. Fed officials are also expected to offer some spirited commentary that could add an exciting twist to the unfolding economic narrative.

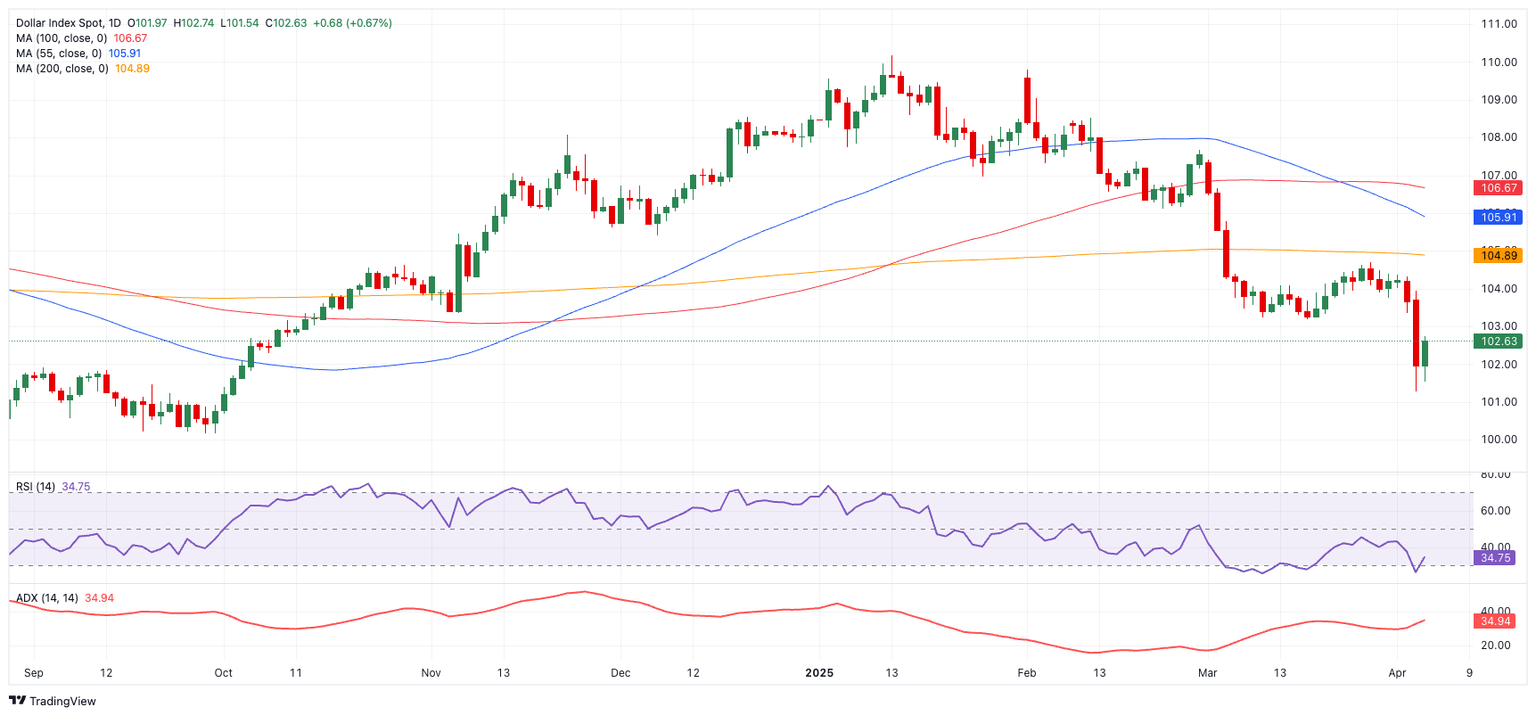

Charting the US Dollar Index

The US Dollar Index (DXY) remains technically under heavy pressure, trading below its key 200-day Simple Moving Average (SMA) of 104.86, which underscores a bearish sentiment.

The downward bias accelerated this week, prompting DXY to now face its immediate support at its 2025 floor of 101.26 (April 3) and further down at the 2024 trough of 100.15 (September 27), just shy of the crucial 100.00 level.

On the other hand, a much-needed rebound could push the index back to last week's high of 104.68 (March 26) before testing the 200-day SMA. Beyond that, the next hurdles are the provisional 55-day and 100-day SMAs at 105.91 and 106.63, respectively, seconded by the weekly high of 107.66 (February 28), the February peak of 109.88 (February 3), and ultimately the 2025 top of 110.17 (January 13).

Meanwhile, momentum indicators do not rule out further retracements in the near term: the daily Relative Strength Index (RSI) has rebounded to the area above 34, while the Average Directional Index (ADX) has advanced to approximately 34, suggesting that the current trend may be gaining some steam.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.