US Dollar Forecast: The real economy and tariffs dominate sentiment

- The US Dollar Index reversed three consecutive weeks of losses.

- The steady lack of clarity over US tariffs hurt sentiment.

- Markets will scrutinise data releases in the labour market.

Finally, a breath of fresh air for the US Dollar (USD).

After three consecutive weeks of closing in the red, the Greenback made a remarkable turnaround, rallying to push the US Dollar Index (DXY) past the key 107.00 mark by week’s end.

This recovery came alongside a notable dip in US yields across different maturity periods. In fact, short-term yields slid back to levels last seen in late October 2024, settling around 4.05%, while the 10-year benchmark yields revisited December 2024 territory, dipping below 4.25%.

US economy: Not so exceptional anymore?

The recent downturn in the US Dollar reflects a slowdown in key economic fundamentals, stirring fresh concerns among market watchers about a potential economic stumble.

Indeed, investor confidence has waned, sentiment indicators have dropped, and surprising reversals in January — such as a notable dip in Retail Sales and a contraction in Personal Spending — have only added to the unease.

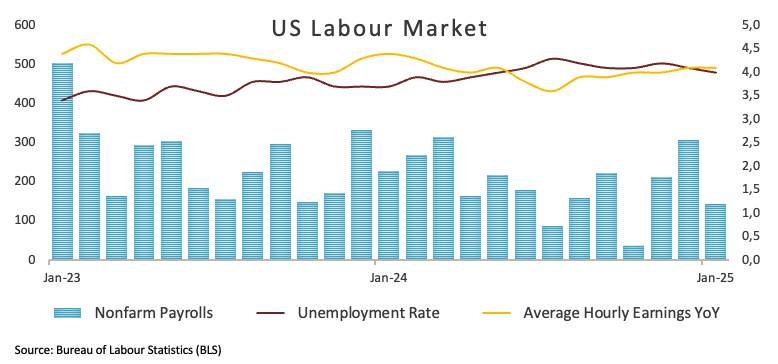

To some extent, these concerns are eased by the labour market's continued strength — even as employment insurance figures fluctuate from week to week.

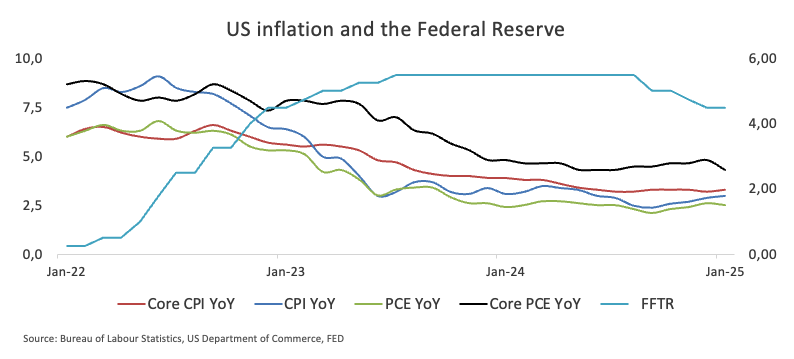

Meanwhile, inflation continues to prove stubborn, persistently exceeding the Fed's target whether measured by the Consumer Price Index (CPI) or the Personal Consumption Expenditures (PCE) report.

Navigating the storm: Tariff volatility and inflation worries

It seems President Trump shed some light over the lack of details surrounding its trade policy, tariffs in particular. That said, he announced on Thursday that levies on Canadian and Mexican Imports will kick in as scheduled on March 4.

At the same time, Trump imposed an extra 10% tariff on US imports of Chinese goods (totaling 20%), while there were no further announcements regarding tariffs on imports from the European Union (EU) at the time of writing, which he already hinted could be around 25%.

We need to differentiate between first-round effects and second round effects from the implementation of tariffs.

In the first case, the imposition of US tariffs on foreign imports could likely have an inflationary impact, which will eventually lead to US consumers having to pay more for those goods. In this, say, “one off” scenario, the Fed would unlikely modify its monetary policy.

However, if this trade policy persists or deepens in time, it could spark the emergence of second-round effects. In this case, producers/retailers could increase prices in a context of dwindled competition, or simply in order to get more benefits.

The consequences of this stance could affect demand, which in turn could lead to more serious effects on the broader economy such as hitting economic activity, as well as employment, and prompting the resurgence of deflationary pressures. In that case, the Fed might want to get more serious and start mulling some measures.

Staying the course: The Fed's conservative approach

In a show of confidence in the US economy, the Federal Reserve (Fed) kept interest rates steady at 4.25% to 4.50% during its January 29 meeting — halting three straight cuts from late 2024. Policymakers highlighted “somewhat elevated” inflation as a lingering concern, suggesting challenges still lie ahead.

In semi-annual testimonies to Congress, Fed Chair Jerome Powell affirmed there was no urgency to reduce rates further, citing a strong economy, low unemployment, and inflation still above the 2% target.

As the week unfolded, other Fed officials added their voices, revealing diverse perspectives on tariffs, inflation, and the direction of monetary policy. Some saw only a limited effect from tariffs, while others expressed caution over rising prices and broader economic uncertainties. Despite these varied outlooks, most officials agreed that waiting for more definitive signals on inflation and overall economic momentum is the best approach before making any significant policy moves.

- Austan Goolsbee (Chicago Fed): Emphasized a “wait-and-see” stance, highlighting the need for more clarity on the economic impact of new Trump administration policies — such as tariffs, immigration changes, tax cuts, spending cuts, and federal workforce reductions — before adjusting monetary policy.

- Tom Barkin (Richmond Fed): Adopted a similarly cautious view, preferring to wait for clearer evidence that inflation is moving back toward the Fed’s 2% target. He cited persistent uncertainty as a key reason for holding off on major policy shifts.

- Jeff Schmid (Kansas City Fed): Pointed to rising consumer inflation expectations, underscoring the importance of ensuring that price pressures remain fully contained. He expressed concern about this trend as a potential issue for policymakers.

- Beth Hammack (Cleveland Fed): Expects the Fed to keep rates unchanged for now, noting that although progress has been made, inflation still sits above the 2% goal. She emphasized the need for further evidence of easing price pressure before any rate cuts are considered.

- Patrick Harker (Philadelphia Fed): Warned that factors such as tariffs, a potential trade war or a shrinking labor force could push inflation higher. Nonetheless, in the absence of significant changes in inflation data, he sees little reason to deviate from the current interest rate policy.

Increased speculative bets put pressure on the Greenback

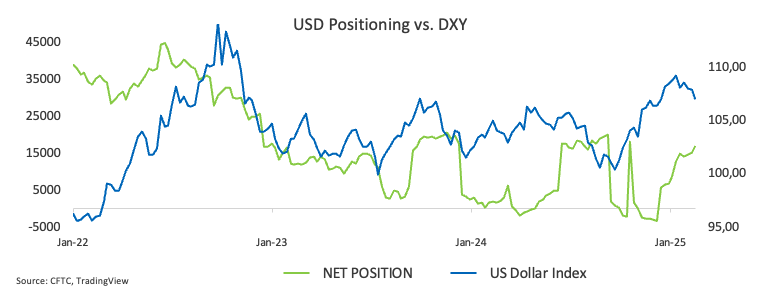

Speculators (non-commercial players) have continued to ramp up their bets on the US Dollar, with the latest CFTC Positioning Report showing a fourth-straight week of net long increases — now at around 16.8K contracts, the highest in months.

However, these crowded long positions could leave the currency exposed to any negative headlines, potentially sparking a rapid unwind and intensifying any correction in the index.

On the bright side, shrinking open interest may help contain the downside if sentiment suddenly shifts.

On the horizon: What lies ahead for the US Dollar?

All eyes are on next week’s US labour market. The focus will be on US February Nonfarm Payrolls (NFP) figures, seconded in relevance by job creation in the US private sector gauged by the ADP Employment Change release, and the usual weekly report on Initial Jobless Claims.

Traders and analysts are also keeping a keen lookout for any fresh commentary from Fed officials. And, as always, there's the ever-present possibility that President Trump might throw yet another curveball into the mix.

DXY spotlight: Momentum shifts and crucial levels

If the recovery gathers steam, DXY might challenge the provisional 55-day Simple Moving Average (SMA) at 107.92, prior to the February high of 109.88 set on February 3 — or even reaching the YTD top of 110.17 from January 13. A break above that mark could open the door to the next resistance level at the 2022 high of 114.77 recorded on September 28.

If sellers regain the upper hand, the index could find its first support at the 2025 bottom of 106.12 reached on February 24, seconded by the December 2024 trough of 105.42 and eventually at the critical 200-day SMA of 104.99.

Staying above that level is key to maintaining the bullish momentum.

Meanwhile, momentum indicators are giving mixed signals. The daily Relative Strength Index (RSI) is nudging close to 50, suggesting the continuation of the recovery, while the Average Directional Index (ADX) lingers around 16, pointing to a generally weak trend.

DXY daily chart

Nonfarm Payrolls FAQs

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation. A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work. The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower. NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa. Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold. Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components. At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary. The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.