US Dollar Weekly Forecast: Fed is seen on hold, shifting focus to politics

- US Dollar Index (DXY) closes the week with modest losses.

- US inflation tracked by the PCE remained sticky in June.

- The Fed is widely anticipated to keep its rates unchanged.

Decent contention emerged around 103.60

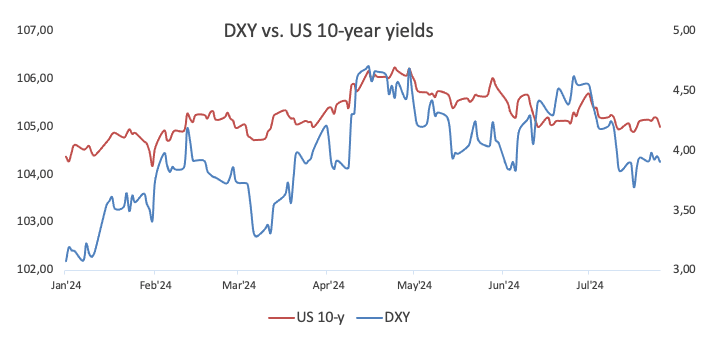

The Greenback navigated an erratic range so far this week, leaving the USD Index (DXY) floating in the 104.00–104.50 band against the backdrop of alternating risk appetite trends but, particularly, closely following developments around the Japanese Yen, which has become the best performer among its G10 peers so far in the month.

Despite the index managing to bounce off four-month lows near 103.60, it still needs to surpass the critical 200-day SMA at 104.34 in a sustainable fashion to restore the constructive outlook and dissipate fears of a deeper retracement.

The policy gap between the Fed and other banks is set to dwindle

The US Dollar’s (USD) bumpy road in the past five days followed almost exclusively events around the Japanese Yen, which, concurrently, came in response to a large unwind of short positions, expectations of a potential rate hike by the Bank of Japan (BoJ) at its meeting on July 31, as well as effects from the latest FX intervention by the BoJ/MoF tandem.

Also bolstering the side-lined tone in the Greenback came rising expectations that the Fed might start cutting its Fed Funds Target Range (FFTR) at its September gathering. Any move on rates at the Fed’s July 31 meeting appears absolutely discarded.

It is worth noting, however, that speculation of a September interest rate cut has suddenly and strongly commenced to pick up pace the minute after US inflation figures gauged by the Consumer Price Index (CPI) showed that the disinflationary trend in the US economy had resumed its traction in June. Those expectations were later reinforced by the extra cooling of the domestic labour market.

In addition, US inflation tracked by the Personal Consumption Expenditure (PCE) also showed a decline over the last twelve months in the headline print (2.5% vs. May’s 2.6%) while remaining sticky when it came to the core reading (2.6% vs. May’s 2.6%).

Meanwhile, the euro area, Japan, and the United Kingdom are all experiencing increasing disinflationary pressures. Against that backdrop, the European Central Bank (ECB) cut rates by 25 bps in June and delivered a dovish hold in July, while subsequent comments from policymakers left the door open to another rate cut beyond the summer. Furthermore, the Swiss National Bank (SNB) unexpectedly cut rates by 25 bps on June 20, while investors continue to pencil in a probable rate cut by the Bank of England (BoE) at its meeting next week. In contrast, the Reserve Bank of Australia (RBA) is expected to begin its easing cycle in the second half of 2025. Contrasting the above, while the Bank of Japan (BoJ) delivered a dovish message on June 14, another rate hike on July 31 has now emerged on the horizon.

Two interest rate cuts in 2024 now appear to be the most feasible scenario

The increasing market speculation about an earlier start to the Fed's easing cycle has been propped up by positive data. Given the decline in domestic inflation, along with a recent slowdown in key areas like the labour market and the manufacturing sector, market participants are now fully anticipating a quarter-point rate reduction in September.

The Fed is widely forecast to keep its rate intact next week, although market participants are expected to closely follow any changes in the Committee’s message, as its latest projection pointed to just one interest rate reduction, likely in December.

According to the FedWatch Tool by CME Group, there is about a 99% chance of rate cuts at the September 18 meeting and around a 98% chance of lower rates by year-end.

Something to consider with your morning coffee: The growing possibility of another Trump administration and the likely return of tariffs could disrupt (or even reverse) the ongoing disinflationary trend in the US economy, possibly shortening the Federal Reserve's easing cycle.

US yields remained choppy

The performance of the US fixed-income universe showed mixed results across the yield curve, as the short end finished the week with marked losses and revisiting levels last seen in January, while the belly retreated marginally and the long end clinched its second consecutive gain.

Upcoming key events

The salient event next week will be the Federal Open Market Committee (FOMC) event. Once passed, investors should shift their attention to the labour market, with the publication of the ADP report, the usual weekly Initial Jobless Claims and the Nonfarm Payrolls. In addition, the Consumer Confidence gauged by the Conference Board will also be in the spotlight along with the ISM Manufacturing PMI.

Techs on the US Dollar Index

The DXY lingers over the 200-day SMA of 104.34.

If bears regain the upper hand, the US Dollar Index could return to the July low of 103.65 (July 17) ahead of the March low of 102.35 (March 8). Further south, the December low of 100.61 (December 28) precedes the psychological threshold of 100.00.

On the upside, DXY faces interim hurdles at the 100-day and 55-day SMA at 104.84 and 104.86, respectively, before the June top of 106.13 (June 26), which is slightly below the 2024 peak of 106.51 (April 16). Once the index clears this zone, it may embark on a test of the November high of 107.11 (November 1), followed by the 2023 top of 107.34 (October 3).

Economic Indicator

Fed Interest Rate Decision

The Federal Reserve (Fed) deliberates on monetary policy and makes a decision on interest rates at eight pre-scheduled meetings per year. It has two mandates: to keep inflation at 2%, and to maintain full employment. Its main tool for achieving this is by setting interest rates – both at which it lends to banks and banks lend to each other. If it decides to hike rates, the US Dollar (USD) tends to strengthen as it attracts more foreign capital inflows. If it cuts rates, it tends to weaken the USD as capital drains out to countries offering higher returns. If rates are left unchanged, attention turns to the tone of the Federal Open Market Committee (FOMC) statement, and whether it is hawkish (expectant of higher future interest rates), or dovish (expectant of lower future rates).

Read more.Next release: Wed Jul 31, 2024 18:00

Frequency: Irregular

Consensus: 5.5%

Previous: 5.5%

Source: Federal Reserve

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.17% | -0.16% | -0.11% | 0.05% | -0.34% | -0.18% | 0.10% | |

| EUR | 0.17% | 0.00% | 0.07% | 0.25% | -0.18% | 0.01% | 0.28% | |

| GBP | 0.16% | -0.00% | 0.04% | 0.23% | -0.18% | -0.00% | 0.27% | |

| JPY | 0.11% | -0.07% | -0.04% | 0.15% | -0.22% | -0.07% | 0.23% | |

| CAD | -0.05% | -0.25% | -0.23% | -0.15% | -0.40% | -0.25% | 0.05% | |

| AUD | 0.34% | 0.18% | 0.18% | 0.22% | 0.40% | 0.18% | 0.49% | |

| NZD | 0.18% | -0.01% | 0.00% | 0.07% | 0.25% | -0.18% | 0.28% | |

| CHF | -0.10% | -0.28% | -0.27% | -0.23% | -0.05% | -0.49% | -0.28% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.