US December PCE Inflation Preview: Is there room for further US Dollar weakness?

- US PCE inflation is expected to continue to ease in December.

- Markets have largely priced in two more 25 basis points Fed rate hikes.

- GBP/USD is likely to react more significantly to a surprise than EUR/USD.

The US Bureau of Economic Analysis will release the Personal Consumption Expenditures (PCE) Price Index data for December, the Federal Reserve (Fed) preferred gauge of inflation, on Friday, January 27 at 13.30 GMT. Reuters estimates show that markets expect the core PCE inflation, which excludes volatile food and energy prices, to rise 0.3% on a monthly basis and forecast the annual rate to decline to 4.4% from 4.7% in November.

Earlier in the month, the US Bureau of Labor Statistics (BLS) reported that the Core Consumer Price Index (CPI) edged lower to 5.7% from 6% in December. Hence, a soft PCE inflation reading shouldn’t come as a big surprise. Additionally, markets have been pricing a less-aggressive Federal Reserve policy tightening since that data release.

Market implications

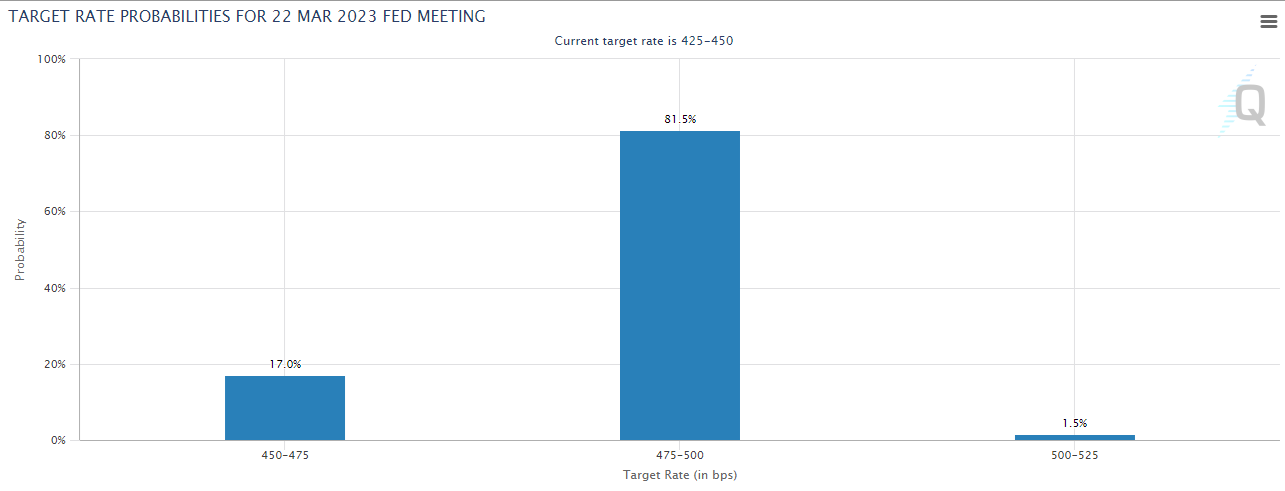

According to the CME Group FedWatch Tool, markets are pricing in a little-to-no chance of a 50 basis points (bps) Fed rate hike in February. Moreover, the probability of a total of 50 bps Fed rate increases at the next two policy meetings currently stands at 80%. Given the market positioning, there is little room for further US Dollar weakness in case PCE Price Index figures confirm the easing of price pressures. It’s also worth noting that investors are likely to refrain from making large bets only a few days ahead of the first FOMC policy meeting of the year.

Source: CME Group

Nevertheless, Wall Street’s reaction to the PCE data could impact the US Dollar valuation against its major rivals. Risk flows have been largely dominating the financial markets since the beginning of the year and an extended rally in the main US equity indexes into the weekend could make it difficult for the US Dollar to find demand.

On the other hand, a stronger-than-expected monthly increase in core PCE inflation could force investors to play it safe and provide a boost to the US Dollar. Again, ahead of next week’s Fed policy announcements, a steady rebound in the US Dollar Index could still be hard to come by.

Among major currency pairs, GBP/USD is likely to react more significantly to a hot PCE print than EUR/USD. European Central Bank (ECB) policymakers have been advocating for two more 50 basis points rate hikes amid rising wage inflation and investors are unlikely to bet against the Euro at least until next week’s policy meeting.

On the other hand, Reuters reported that, following the disappointing UK PMI data earlier in the week, markets were fully pricing in a Bank of England rate cut in 2023. Furthermore, the uncertainty surrounding the UK-EU post-Brexit negotiations complicates the situation further for the Pound Sterling moving forward.

GBP/USD Technical Analysis

GBP/USD continues to trade comfortably above the ascending trend line coming from late September and the Relative Strength Index (RSI) on the daily chart holds near 60, suggesting that the pair’s bullish bias stays intact.

On the upside, static resistance seems to have formed at 1.2450 ahead of 1.2500 (psychological level). With a daily close above that level, Pound Sterling could target 1.2600 (psychological level, static level) and 1.2660 (static level from June).

1.2300 (psychological level, static level) aligns as initial support. Below that level, the 20-period Simple Moving Average (SMA) forms the next support at 1.2200 ahead of 1.2150 (ascending trend line, 50-period SMA).

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.