US CPI Preview: It is the hard core that counts, five scenarios for critical inflation data

- Investors are looking for hard evidence that inflation has topped after several "soft" indicators.

- Economists expect a moderate deceleration in Core CPI MoM to 0.5% in July.

- With the Fed focused on inflation, every 0.1% counts for the market reaction.

Get real – that has been the message from hawks to Federal Reserve Chair Jerome Powell, until he has overseen massive interest rate hikes. Getting real is also what investors are looking to see from the upcoming Consumer Price Index report for July. So far, only soft survey data has pointed to softer inflation expectations. It is time for hard evidence.

First, I want to clarify that most Americans are interested in the prices of all goods – first and foremost the price at the pump, which is a daily reminder of inflation or lack thereof. On that front, there are undoubtedly positive developments. Oil prices began falling in June and are expected to be felt in the headline July CPI data.

Economists expect inflation to have decelerated from 9.1% to 8.7% YoY. Monthly, a modest increase of 0.2% is projected after a leap of 1.3% in June. Headline CPI is set to take one step back:

Source: FXStreet

Core counts

A drop in gasoline prices is what will make the headline and talk shows, with pundits arguing about Democrats' chances in the midterms. Markets will look the other way. What matters for investors and for the Fed is core inflation – prices of everything excluding energy and food.

No, Fed officials still drive cars and eat. So do investors. However, these volatile items are priced on global markets, where the central bank hardly has any impact. It can, however, curb demand by setting higher interest rates – encouraging saving and discouraging lending.

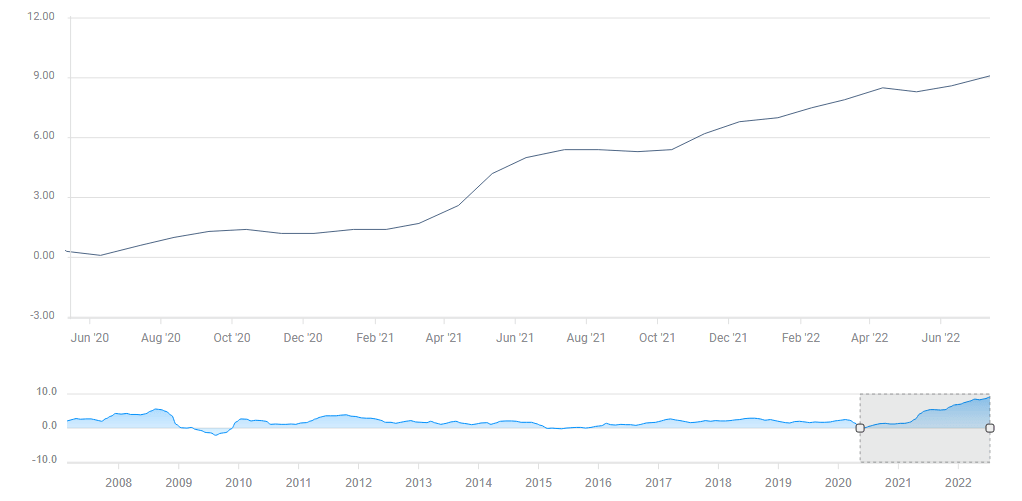

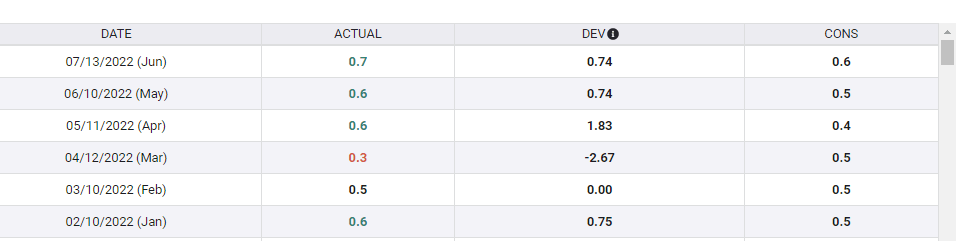

The Fed wants to see the impact of its recent policy changes – it began raising rates only in March – making monthly figures more important. Core CPI is expected to have accelerated from 5.9% to 6.1% YoY, owing to a more modest increase of 0.5% in monthly underlying inflation, down from 0.7% recorded in June.

Here are recent Core CPI developments:

Source: FXStreet

Economists were too optimistic in the past three months, in which the annualized rate of Core CPI stood at around 8%. Nevertheless, forecasters have probably learned their lessons, and there is room for optimism due to the fall in energy prices – it might have propagated to costs of other goods.

The Fed is laser focused on bringing inflation down, as comments from all members, before and after the superb Nonfarm Payrolls report have shown. That makes every 0.1% in Core CPI a major market mover.

Five scenarios

1) Within expectations: A Core CPI read of 0.5% MoM would shift the focus to the yearly increase. If the broader gauge indeed increases to 6.1%, it would seem that the lower monthly figure and the higher yearly one offset each other. Nevertheless, both figures would still be high, around triple the Fed's target of 2%.

Is that enough evidence to say that inflation has peaked? Probably not, and I expect the reaction to be mixed. Stocks would rise, but the dollar would likely gain ground, as it would leave the Fed at the forefront of central bank tightening. The moves in both would be minimal.

If that 0.5% read would be accompanied by an upward revision of previous months, it would add to dollar strength and could curb some of the enthusiasm in stocks, yet probably on the margins. A downward revision to June's data would limit dollar gains and add to stocks' upward momentum, but only just.

2) A moderate 0.1% beat: If Core CPI hits 0.6%, markets will read it as a sign that inflation is still strong. USD/JPY, which offers the most straightforward responses to inflation, would rise. The euro and pound would also be on the back foot.

Commodity currencies would also advance, but if stocks stabilize, so would the Aussie. The Canadian dollar would also weather the storm, as rising prices in the US mean a similar phenomenon up north and growing chances of aggressive monetary tightening by the Bank of Canada.

3) Raging inflation, 0.2% gap or more: A scenario in which Core CPI MoM hits 0.7% once again – or more – is not on the radar and would serve as a nasty surprise for policymakers and for stock bulls. Shares would tumble on expectations of quicker rate hikes and the dollar would reign supreme across the board. Low probability, high risk.

4) Moderate miss, 0.1% below estimates: If Core CPI hits 0.4%, it will trigger a stock rally – investors are already in FOMO mode and need small sparks to light a fire. For the dollar, it would finally provide some hard data that prices are falling, either as a side effect of lower energy prices or an unsnarling of supply chain issues.

The greenback's decline would likely be more pronounced against the yen, as 10-year bond yields would be the first to reflect the data, and USD/JPY is highly correlated with returns on benchmark US debt. Commodity currencies, especially the Aussie and the kiwi would also benefit.

However, the euro and the pound face their own issues, mostly in Russia, and would struggle to gain ground in response to a moderate miss.

5) Peak inflation is here, a miss of 0.2% or more: A return to Core CPI of 0.3% would be more than welcome by markets, which would rally hard in response to hard evidence of decelerating price rises. It would represent an annualized rate of less than 4% in core prices, a manageable level.

For stocks it would mean a rally, and for the dollar a downfall across the board. As with the scenario of a big beat, such deviations would trigger a straightforward response, but their likelihood is low.

Final thoughts

Markets' response to Nonfarm Payrolls was robust. That seems to merely be the warmup to inflation data, which is a high-stakes event given the current focus on price rises. I recommend trading with low leverage.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.