US CPI inflation is key for sentiment and US dollar

Market Overview

The recent spike in volatility and flight to safety was driven by the fear that the fires of inflation were being stoked. Born out of a jump in US earnings growth as part of the payrolls report, bond yields have risen sharply and equity markets have sold off. The past few days has seen a modicum of calm beginning to creep back into market sentiment. However this could be the calm before the next storm as traders look ahead with trepidation at the US CPI inflation numbers today. Expectation of inflation has been rising this year but will there be hard confirmation of inflation? Consensus actually expects a mild tick lower on both headline and core CPI, but any upside surprise would get the market’s pulse rate pumping again. The yen has been the main beneficiary during this time of stress, and would certainly find yen strength with a significant shot in the arm again. The dollar has also lost some of its recovery in the past few days but this would also regain momentum too. However, probably the key factor would be equity markets coming back under renewed pressure. For the outlook of the coming days at least, the US CPI data will be crucial.

Wall Street closed mildly higher in a relatively benign session, with the S&P 500 +0.3% at 2663, with Asian markets mixed (Nikkei -0.4% on a stronger yen), whilst European markets are starting on the front foot.. In forex the dollar is under pressure ahead of the crucial US CPI data this afternoon, with the yen having again found strength overnight despite a slight miss on the Japanese Q4 2017 GDP growth data (Q4 annualised at +0.5% revised down from +0.9%). The New Zealand dollar is also positive on the back of an encouraging inflation survey. In commodities, the weaker dollar is again helping to support gold, whilst even the oil price is looking to stabilise.

Considering the volatility that was generated from the Average Hourly Earnings a couple of weeks ago, today is an extremely important day for traders, with US consumer inflation to be announced. However, first up id the Eurozone flash GDP at 1000GMT which is expected to improve to 2.7% for the Year on year from +2.5%) which would be +0.6% QoQ. The US CPI inflation data will take all the focus at 1330GMT with consensus expectation that headline CPI will drop to +1.9% from +2.1% last month, whilst the core CPI is expected to also tick lower to +1.7% ( from +1.8% last month). Traders will also be on alert for US Retail Sales at 1330GMT which are expected to be show ex-autos growing once again by +0.4% for the month (+0.4% last month). The EIA oil inventories are expected to again see a crude build, of 2.7m barrels (+1.9m last week) with distillates at -1.7m (+3.9m last week) and gasoline at +1.5m (+3.4m last week).

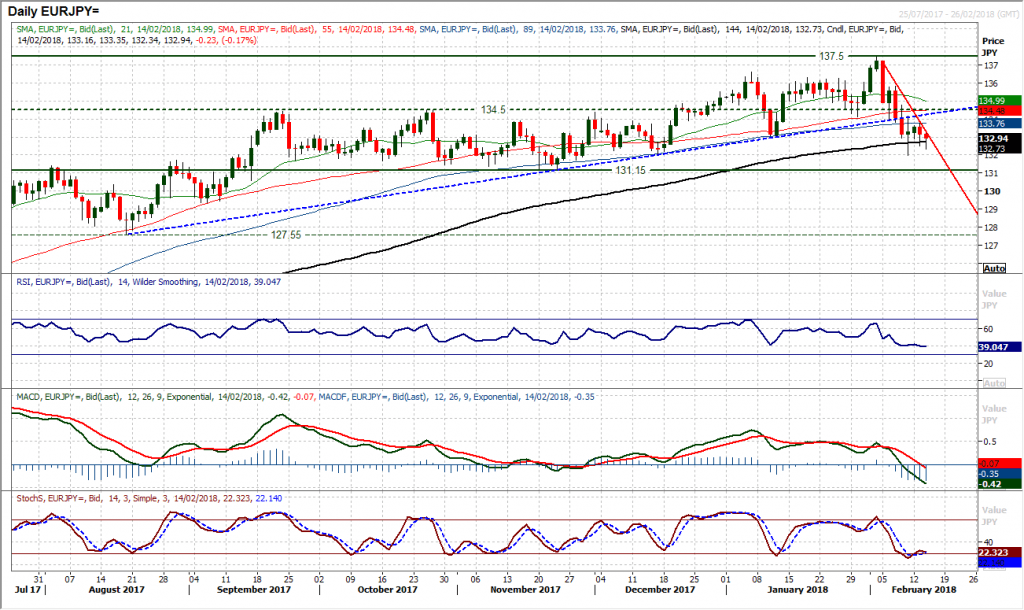

Chart of the Day – EUR/JPY

As markets have traded with an increased sense of risk aversion over the past couple of weeks, the yen has been strengthening, even against the euro which has held up relatively well against the majors. This has broken a shallow downtrend on EUR/JPY as the market has corrected back with a series of negative candles. This has resulted in increased downside pressure on what is a key medium term support on EUR/JPY at 131.15 which if broken would be a significant change of sentiment on the pair. The outlook retains a technical configuration of buying into weakness but the market now appears to be at a significant crossroads and the bears are threatening to really grasp control. Over recent months, the RSI has continually picked up from around 40 to end the corrective moves, however, this is being severely tested as the RSI has dropped into the 30s today. Furthermore, the MACD lines are on the brink of decisively falling below neutral for the first time since April. The support at 131.95 from last week’s low could be key to protect 131.15 but yesterday’s bear candle is a concern, especially with additional losses early today. The hourly chart shows that the resistance at 134.15 will be key now as a lower high.

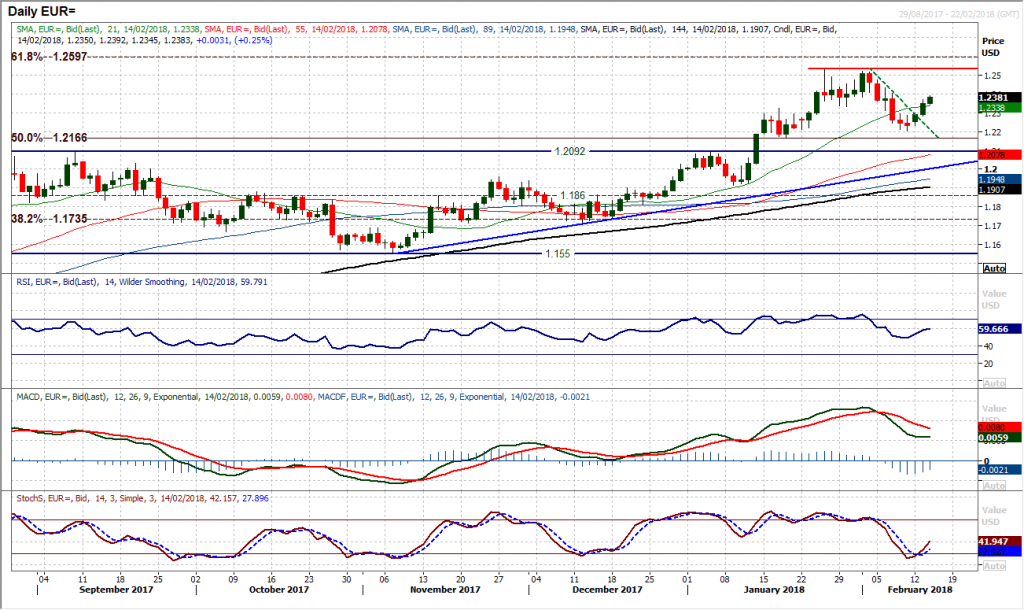

The near term recovery for the dollar seems to have lost its way in the past few sessions as the euro looks to rebound again. The corrective phase on EUR/USD that lasted just over a week has now bounced from $1.2205 to break a sequence of lower highs and looks to now be building a renewed push higher. A second successive completed positive candle was formed yesterday as the market also closed above the previous breakdown at $1.2335. Daily momentum indicators have had a configuration of unwinding within a medium term bull market and as such, the Stochastics have ticked higher (arguably with a buy signal), the MACD lines are stabilising above neutral and the RSI is rising back above 50. The hourly chart shows a run of higher lows is also now forming. Te near term support band $1.2335/$1.2345 will be a gauge today for continued gains, whilst hourly momentum is positively configured. A break above resistance at $1.2400/$1.2435 would re-open $1.2520. The US CPI data is the main caveat for the moves today.

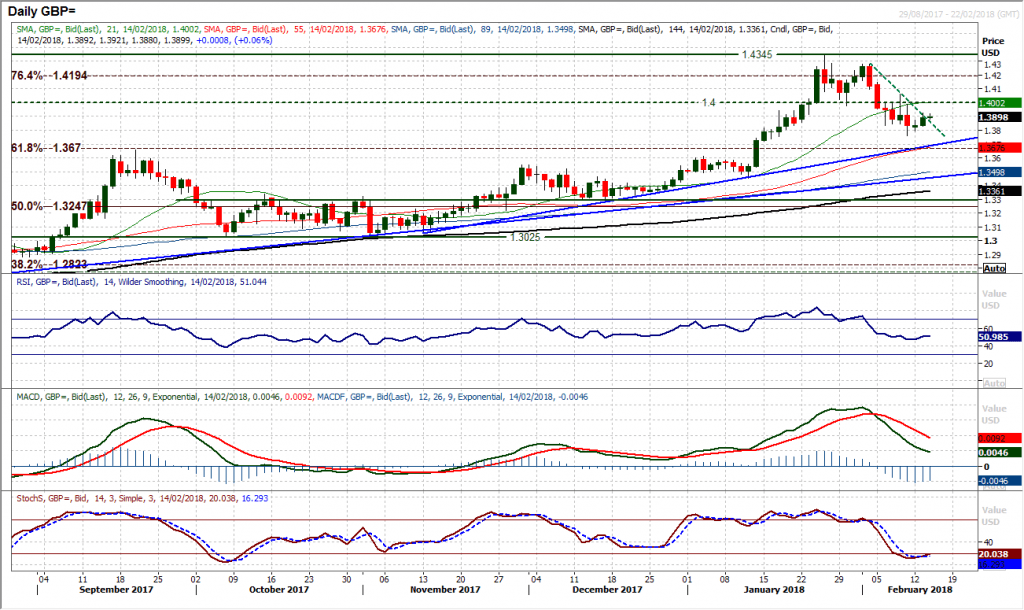

Although Cable is not as far developed in re-asserting bull control, there is still a degree of renewed optimism as the market loos to build higher once more. The positive candle formed yesterday means that there is now a sequence of higher daily lows forming above last week’s low at $1.3765. The recent corrective move has always felt like being a near term correction within a medium to longer term bull market with the three month trend support coming in at $1.3690. Furthermore, the daily momentum indicators have been medium term positively configured, with the corrective move unwinding overbought momentum. The RSI is looking to pick up again from 50 whilst the MACD lines are above neutral. However there needs to be a move back above the key breakdown at $1.3975 to allow the bulls to regain confidence again. The hourly chart suggests it is still early days for the bulls, but holding on to support at $1.3850 today would certainly help. Watch out for the US CPI data this afternoon.

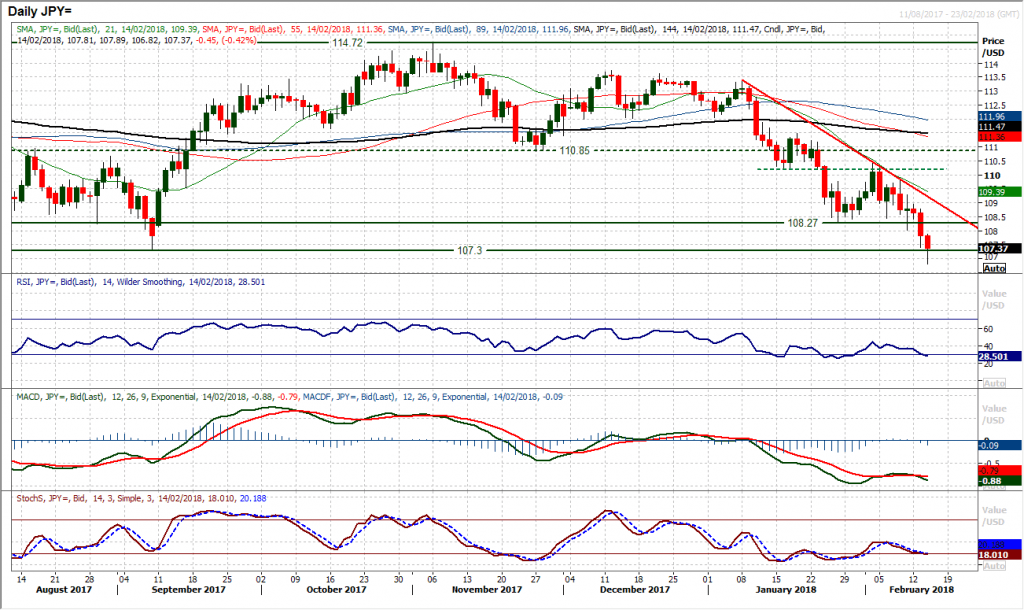

The yen continues to strengthen significantly against the dollar as USD/JPY has fallen below the key support at 107.30 overnight to levels not seen since November 2016. If there is a decisive two day close below 107.30 then it would seem that the ranging phase of the past year would have been broken. The concern is that momentum indicators are set up to suggest that there is not only negative configuration but also downside potential in the current move. This comes with the bear kiss on the MACD lines, whilst Stochastics and RSI are both not excessively stretched for a bear phase. There has been an acceleration lower in the past couple of sessions with the market clear of the old support at 108.27 which is now a basis of resistance, whilst the hourly chart shows resistance at 107.90/108.00. Intraday rallies are also being seen as a chance to sell still, with the hourly RSI failing around 40/50 now. Initial support is at 106.80 but there is little to hold up the market until 105.50. The reaction to US CPI this afternoon could be crucial for the medium term outlook.

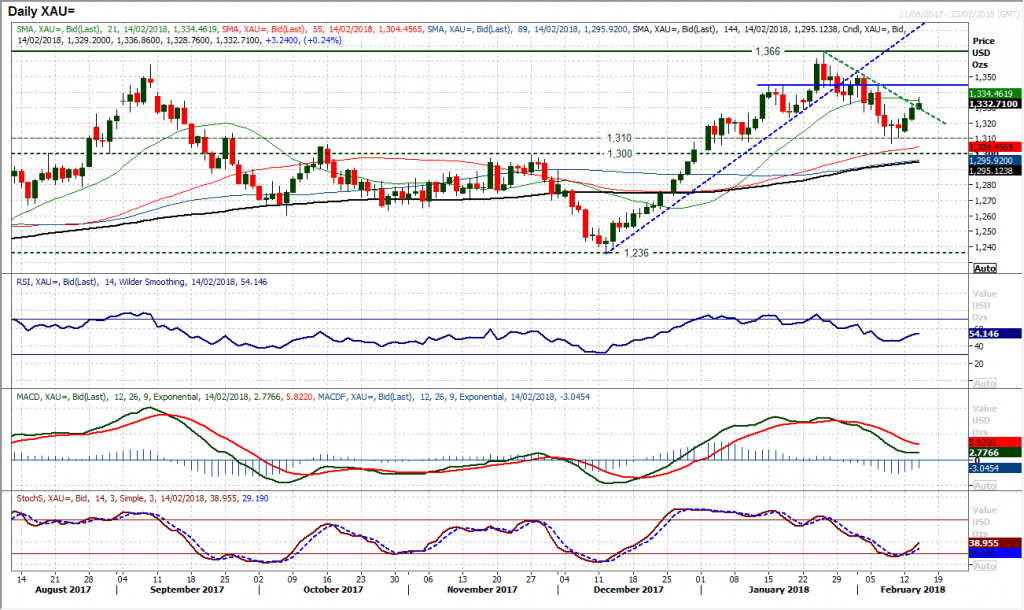

Gold

The gold bulls will have been extremely happy with the reaction to the long term pivot support $1300/$1310. Last week’s low at $1306.80 has since been followed by a series of very encouraging positive candles, with the market posting two successive strong bull candles, and now further early morning gains have broken a two week downtrend. This comes with the momentum indicators picking up again. The MACD lines looing to bottom above neutral in addition to the Stochastics and RSI also picking up, suggests that the support at $1306.80 is firm now. The hourly chart shows a run of higher lows building (the latest at $1322.70) whilst the move above resistance at $1332 this morning can also be important if the market is able to close above today. Look to use intraday weakness for this near term recovery to continue. A break back above resistance at $1344/$1346 would open initially $1351 but also mean the key high at $13666 is back on. The US inflation data this afternoon is once more key though.

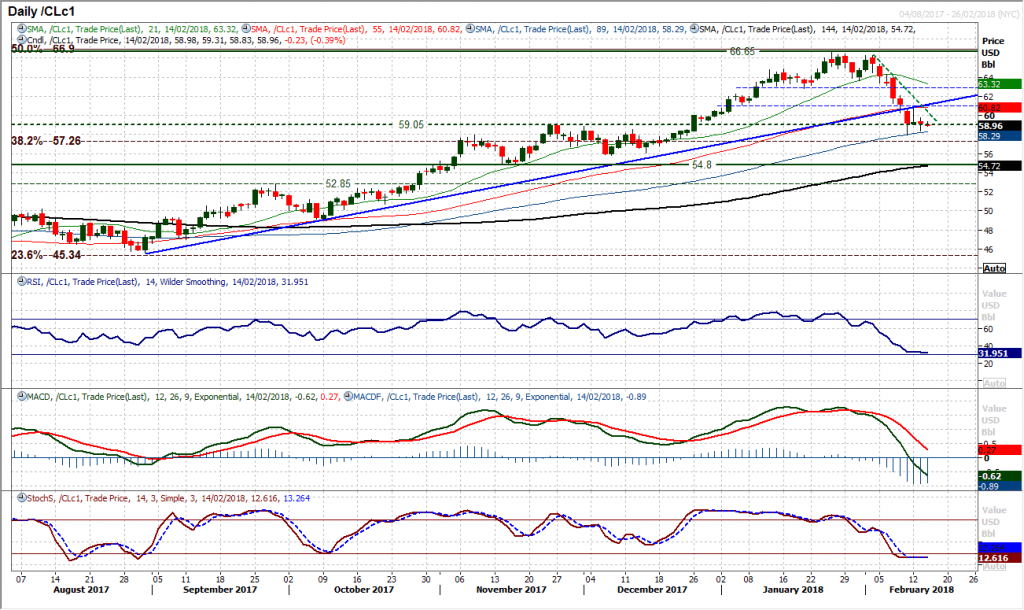

WTI Oil

The break below the 5 month uptrend has been a key move to deteriorate the longer term outlook. Having broken the trend on Friday, the market rally on Monday subsequently failed under the old trend to leave the bears in control now near term. The momentum indicators remain corrective and the pressure of using intraday rallies as a chance to sell continues. The hourly chart shows bearish configuration on the hourly RSI which fails around 50/60 and the hourly MACD lines are continually failing around neutral. Resistance comes in at $60.85 and then $62.10 but having broken back under the support band $59/$60 the pressure continues to eye the key November/December lows at $54.80/$55.90. With the market bouncing from $58.40 yesterday, Friday’s low at $58.05 is now key near term and a breakdown would re-open the downside. There is a slight element of consolidation that has crept into the market, but it would need a decisive move above$60.85 to hint that the buyers are gaining a foothold. For now the outlook for a corrective move lower continues.

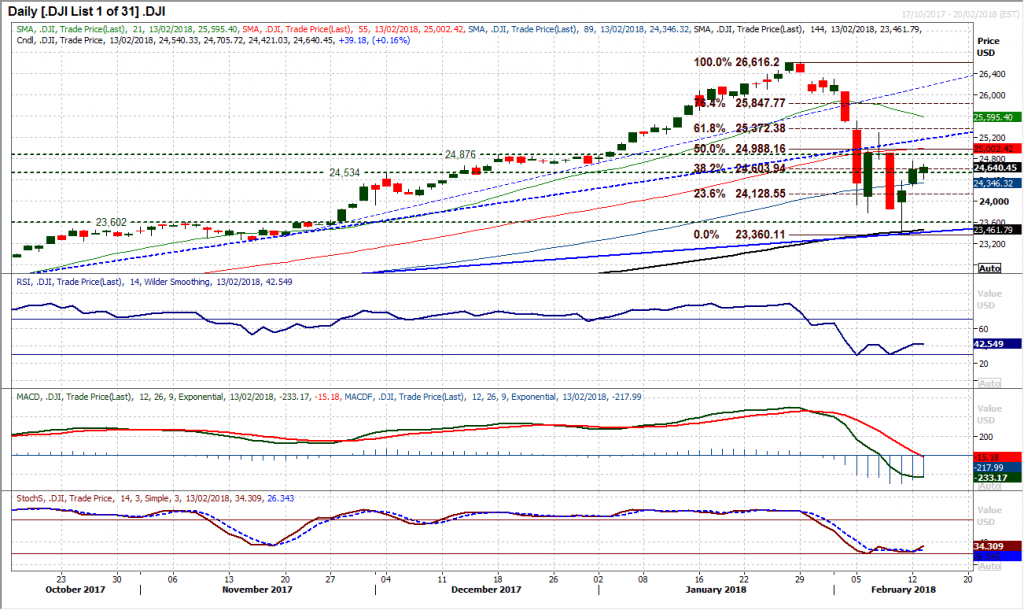

Dow Jones Industrial Average

Is it possible that the volatility is beginning to subside? The key could be how the market now reacts today. Last week’s huge rebound was quickly pounced upon by the sellers again and the market fell sharply again. However the rally of Friday and Monday has so far resisted the resumption of the bear control. Furthermore, yesterday’s daily range of (just) 284 ticks was by far the lowest range since sentiment changes on Non-farm Payrolls Friday, compared to the Average True Range which is still a whopping 607 ticks. The problem is that so far there is still a run of lower key highs in place that the bulls need to overcome. Monday’s rebound high at 24,765 needs to be watched and then 25,294. The hourly chart could hold the clues, as with the bears in control all the rallies have failed under 60 on the hourly RSI and all the MACD lines have failed under neutral. Initial support at 24,290 from Monday’s low.

Author

Richard Perry

Independent Analyst