US CPI inflation finally lower, PPI slightly higher, US unemployment claims fell, drop in US consumer

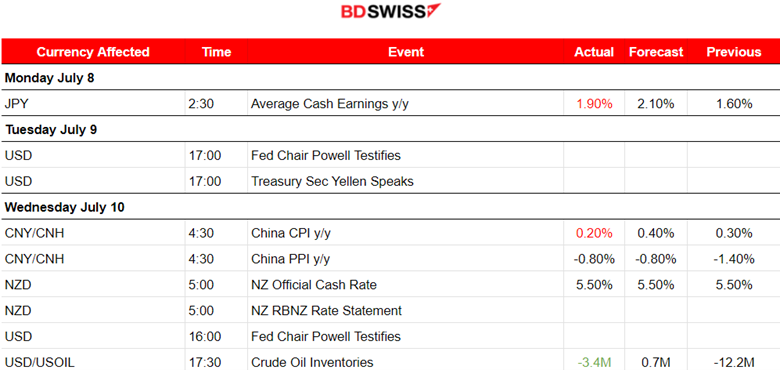

Previous week’s events (week 08 - 12.07.2024)

US economy

Fed Chair Jerome Powell has acknowledged the improving trend in price pressures but told lawmakers this week he was not yet ready to declare inflation had been beaten and that “more good data” would strengthen the case for rate cuts.

Initial claims for state unemployment benefits fell 17,000 to a seasonally adjusted 222,000 for the week ended July 6, the lowest level since late May.

Inflation

US CPI

The U.S. consumer prices fell for the first time in four years in June drawing the Federal Reserve another step closer to cutting interest rates in September. The lower-than-expected CPI inflation reading helped boost confidence among officials at the U.S. central bank that inflation is cooling after surging in the first quarter.

The CPI dipped 0.1% last month, the first drop since May 2020, after being unchanged in May. The CPI was weighed down by a 3.8% decline in gasoline prices, which followed a 3.6% decrease in May.

In the 12 months through June, the CPI climbed 3.0%, the smallest gain since June 2023. That followed a 3.3% advance in May. The annual increase in consumer prices has slowed from a peak of 9.1% in June 2022.

US PPI

U.S. producer prices increased slightly more than expected in June amid a rise in the cost of services, but that did not change expectations that the Federal Reserve could start cutting interest rates in September.

The producer price index for final demand rose 0.2% last month after being unchanged in May. In the 12 months through June, the PPI increased 2.6%. That was the largest year-on-year gain since March 2023 and followed a 2.4% advance in May.

PCE inflation was forecasted to have edged up 0.1% in June after being unchanged in May. Estimates for the core PCE price index converged around a 0.15% rise. Core inflation ticked up 0.1% in May. Both PCE and core inflation were seen increasing 2.5% year-on-year in June after rising 2.6% in May.

Interest rates

RBNZ

New Zealand’s central bank (RBNZ) held the cash rate steady at 5.5% on Wednesday. The decision was in line with the expectations.

The RBNZ said it expected headline inflation to return within the 1% to 3% target range in the second half of this year, down from 4% in the first quarter.

The rate hikes have sharply slowed the economy, although recent data showed New Zealand moved out of a technical recession in the first quarter of 2024 with growth of 0.2%.

Currency markets impact – Past releases (week 08 - 12.07.2024)

Server Time / Timezone EEST (UTC+03:00).

Currency markets impact

-

Fed’s Powell highlights: A slowing job market signalling that rate cuts may take place soon. “Inflation has eased notably” in the past two years, he added, though it still remains above the central bank’s 2% target.

-

China’s inflation was reported to be weak, falling to 0.20% on a yearly basis. Weak domestic demand is the reason. No major impact on the market was recorded.

-

On the 10th, the RBNZ decided to keep rates steady causing the NZD to depreciate significantly. An intraday shock was recorded that caused the NZDUSD to drop nearly 50 pips before a retracement took place. The drop though continued to take place.

-

On the 11th of July, the UK monthly GDP figure, released at 9:00, reported growth for the U.K. economy. Monthly real gross domestic product (GDP) is estimated to have grown by 0.4% in May 2024 after showing no growth in April 2024. The GBP was appreciated only momentarily. The intraday shock was minimal.

-

At 15:30, a massive intraday shock took place affecting the markets. The strongly anticipated U.S. inflation report was reported surprisingly lower than expected at 3%, down from 3.3%. The USD depreciated heavily. USDJPY fell to near 400 pips before retracing. The initial response for U.S. indices was a jump and then a full reversal with a non-stop steady drop. Gold Jumped.

-

U.S. unemployment claims were actually reported lower at 222K, close to figures seen in June, but the market completely avoided this release.

-

The U.S. PPI data released at 15:30 showed that the wholesale price inflation accelerated in June beating expectations. The Core reading was 0.2% higher than the expected figure. At the time of the release the USD was affected by a minor shock, however, a steady depreciation followed.

-

The U.S. consumer sentiment declined unexpectedly to the lowest level in eight months and caused further depreciation of the currency. The sentiment index fell to 66 in July from 68.2, according to the preliminary reading from the University of Michigan. Inflation expectations improved, with an initial figure to be reported 2.9%. This reading coincides with the recent inflation data that showed cooling, at least for the CPI inflation. The USD pairs moved to the downside during the figure releases.

Forex market monitor

Dollar Index (US_DX)

The index turned to the downside as economic indicators finally show that inflation is lowering for the U.S. On the 11th of July, the CPI inflation report surprised the markets with a weak figure. A shock took place causing massive USD depreciation against a basket of currencies, a 0.70 points drop before retracement took place. Market expectations were met in regard to lower prices and borrowing costs. Dollar weakening also took place even after the PPI inflation report on the 12th. Despite the higher-than-expected released figures, USD deprecation continued as market participants are convinced that interest rate cuts are going to take place soon.

EUR/USD

The EURUSD experienced an uptrend starting on the 10th of July. Obviously, the USD was driving the market. The USD deprecation was reinforced by the news. The CPI data report helped boost confidence that inflation is cooling after surging in the first quarter. EUR on the other hand is not greatly affected. The ECB had taken the decision to cut rates once so far and inflation was reported lower in the Eurozone.

USD/JPY

The USDJPY lowered this week as the USD experienced a strong weakening, mainly from the inflation report. However, at the same time, a great amount of JPY buying during the news releases caused the USDJPY to drop heavily. On the 11th, BOJ intervention caused a 400 pips drop in the pair before it eventually retraced. The next day, on the 12th, two more cases of sharp drops indicate intervention trying to strengthen the JPY. USDJPY just like the U.S. dollar index is facing a strong support area at 157.4.

Crypto markets monitor

BTC/USD

The latest price data formed a triangle indicating that volatility levels lowered and as mentioned in our previous analysis upon triangle breakout on the 10th, it led to a jump. The price remained higher, settling at 58K USD but eventually moved to the downside until the 12th. On that day the price reversed to the upside, crossing the 30-period MA on its way. It was the start of an uptrend that surprisingly led the price to continue steadily upward during the weekend. At the start of the week, on Monday 15th, the price jumped to nearly 63K USD. That is a remarkable recovery for Bitcoin’s price.

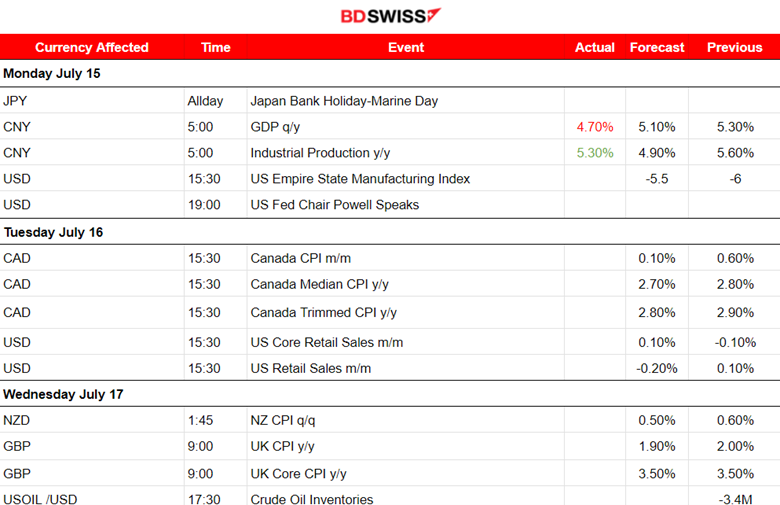

This week’s events (week 15 - 19.07.2024)

Coming up:

-

Inflation data release for Canada, New Zealand, and the U.K.

-

Interest rate decision from the ECB.

-

Retail Sales reports for the U.S., Canada and the U.K.

-

Labour data releases for the U.K. and Australia.

Currency markets impact

On the 16th of July, the CPI inflation data for Canada will be released. It is expected that the figures will be reported lower. This could be the case as the labour data show great weakness. The unemployment rate reached higher and higher and of course this should have an impact on prices. CAD pairs could see an intraday shock upon release. A surprise to the upside though is not to be excluded and that could lead to high CAD appreciation.

At the same time, at 15:30, the U.S. retail figures will be released and will potentially affect the USD pairs at that time. Expectations are mixed with regard to the figure type. A moderate shock is expected.

On the 17th the inflation report for the U.K. will take place at 9:00. The GBP pairs will be probably affected greatly by an intraday shock. The annual inflation figure is expected to be reported lower while the Core figure is expected to remain unchanged. The ECB has also cut rates just like the BOC and it could be the case that prices remain unchanged due to the fact that even with elevated rates, inflation is very hard to bring down.

At 4:30 on the 18th the labour market data for Australia is going to be released. Economists expect weaker labour market data. The truth is that inflation in Australia is not lowering at all. The RBA might actually take drastic decisions, for example, another hike. The most recent reports show that figures continuously beat expectations in regard to employment change. AUD pairs could see appreciation with another surprise to the upside.

Claimant count change last time was reported way higher than expected for the U.K. Expectations now are that it will be reported lower. The U.K. is facing a low unemployment rate actually under 5% and inflation was reduced to 2%. However, the BOE did not proceed with any cuts yet. It might be the case that indeed the number of people claiming unemployment-related benefits will be reported again high but the expectation will probably be met as it is close to the recent average figure. GBP pairs could see a moderate shock even without a surprise taking place.

On the 18th the ECB is going to decide on rates. It is expected that there will be no change in interest rates giving the Eurozone time to digest last month’s first cut since 2019 as the direction of inflation is quite uncertain. EUR pairs could be affected greatly.

On the 19th the U.K. retail sales report will take place and it is expected that the retail sales figure will show a decline in retail sales, a turn from growth that was previously reported. This suggests that economists expect that economic conditions are deteriorating and coincide with the expectation that inflation will be further lowered. GBP pairs could see increased volatility and GBP depreciation in such a case.

The Canada retail sales report is taking place the same day and is also expected to show reductions. CAD pairs could be affected by a moderate shock. Another deterioration is expected in Canada’s business conditions as suggested by the expected figures. A surprise to the upside can be excluded since the employment change figure reported recently was actually a decline indicating much weakness.

Commodities markets monitor

US Crude Oil

The price settled near the 80.5 USD/b level, below the MA, but on the 10th it eventually reversed to the upside. This movement was a correction/retracement to the 61.8 Fibo level as depicted on the chart. The price boost to the upside was a result of a reported decline, -3.4M barrels in Crude Oil Inventories in the U.S. against a forecast of 0.7M growth. During the U.S. inflation news yesterday on the 11th Crude oil prices saw some retreat but eventually reversed to the upside. After several tests of the resistance 82.10 USD/b, it finally broke that resistance. After finding strong resistance at near 82.5 USD/b the price reversed to the downside on the 12th breaking that triangle formation. It did not, however, reach the 80.2 USD/b support but it has the potential to do so as long as it moves away from the 81 USD/b level significantly towards the downside.

Gold (XAU/USD)

The price eventually moved to the upside on the 9th of July crossing the 30-period MA on its way up. The target level of 2,380 USD/oz was reached as per our forecast in the previous analysis and the price even moved higher reaching the resistance at 2,387 USD/oz before retracement took place. On the 11th, the USD weakening that took place during the U.S. inflation report release caused the price to jump, initially reaching near 2400 USD/oz. After testing that resistance intraday, another breakout led to the price reaching even the resistance near 2,423 USD/b before retracing to the MA. On the 12th the price continued with retracement after the previous day’s peak. When it touched the MA it reversed to the upside to continue with a sideways path. A triangle formation is now apparent and we wait for its breakout to take advantage of the rapid movement in one direction that will probably occur. 2,380 USD/oz is the target level for a downward breakout. To the upside target level would be 2,430 USD/oz.

Equity markets monitor

S&P 500 (SPX500)

Price movement

The CPI inflation y/y figure was reported on the 11th and the index dropped as per our forecast in the previous analysis. Expectations about lowered borrowing costs starting in September are boosting investment in stocks. After the shock on the 11th, the market experienced another shock on the 12th after the release of the PPI data, Consumer sentiment and inflation expectations. A jump occurred with the price finding resistance around 5,660 USD before retracing to the intraday mean. Huge volatility for the index last week as depicted on the chart.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.