- July headline CPI stays at 5.4%, core slips to 4.3%, about as forecast.

- Dollar weakens, Treasury yields are mixed, as the case for rate hikes diminishes.

- Used-car prices rise 0.2% in July after June’s 10% increase.

American consumer prices delivered the first hint that the rampant gains since January may have reached their apogee, lending support to the Federal Reserve claim that inflation increases will be transitory.

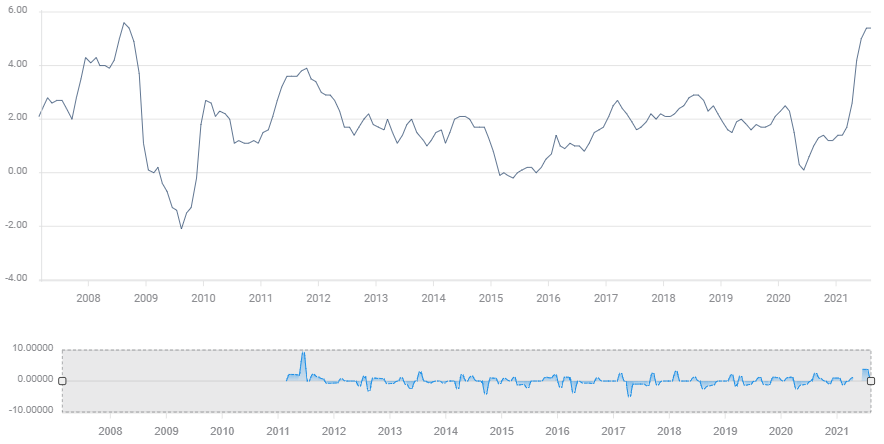

The Consumer Price Index (CPI) rose 0.5% as forecast in July, down from 0.9% in June. The annual rate was unchanged at 5.4%, matching the largest increase since August 2008, reported the Labor Department in Washington, D.C. It had been predicted to drop to 5.3%.

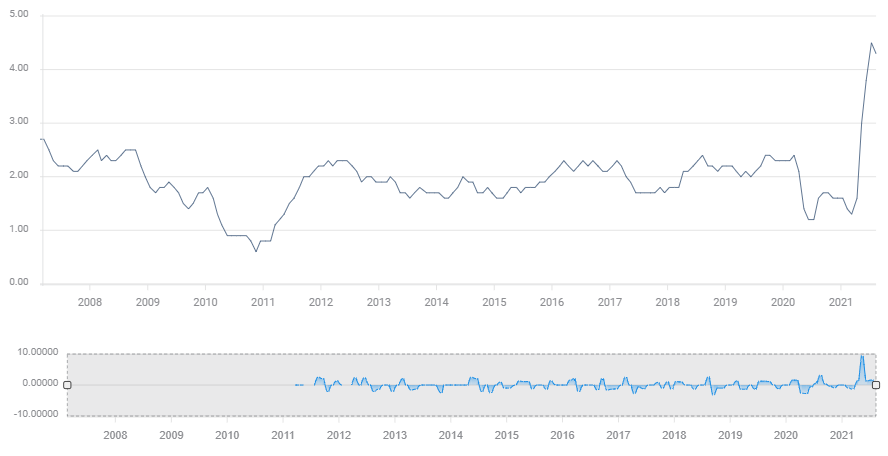

Core prices, which exclude volatile energy and food costs, climbed 0.3% on the month, also down from 0.9% in June and lower than the 0.4% projection. The yearly rate was 4.3% in July, as expected by analysts, from 4.5% prior.

Prices have been on a tear this year as the economy reopened and consumer demand, supply chain disruptions and labor shortages combined with the reversal of last year's lockdown collapse, drove inflation gains to their highest in over a decade.

CPI

Core CPI

Yearly inflation more than tripled from 1.4% in January to 5.4% in June and July and the core rate soared from 1.4% at the beginning of the year to 4.5% in June and 4.3% in July.

Federal Reserve policy

The Federal Open Market Committee (FOMC) has kept the fed funds rate near zero for the past 18 months and maintained short-term yields at record lows with $120 billion a month in purchases of Treasuries and mortgage-back securities.

The Federal Reserve has maintained for almost a year, since adopting inflation-averaging as its policy diagnosis last September, that the outsize price jumps will diminish and halt as the disparity from the lockdowns dissipates.

Treasury yields and the dollar had been on the rise since last week when comments from several Fed officials, including Vice-Chair Richard Clarida, and the stronger than expected Nonfarm Payrolls report on Friday, made it seem that the labor market conditions for a reduction in the bank’s bond purchases might be nearing.

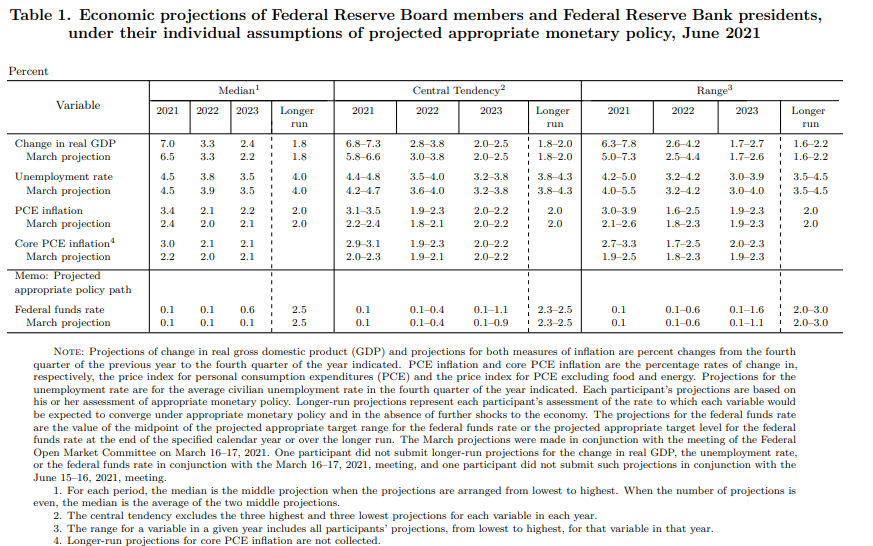

Central bank officials have given no timeline for the projected policy reversion but the June Projection Materials which compiles Fed estimates, raised the annual Personal Consumption Expenditures Price Index (PCE) forecast for 2021 to 3.4% from 2.4% and the core rate to 3.0% from 2.2%.

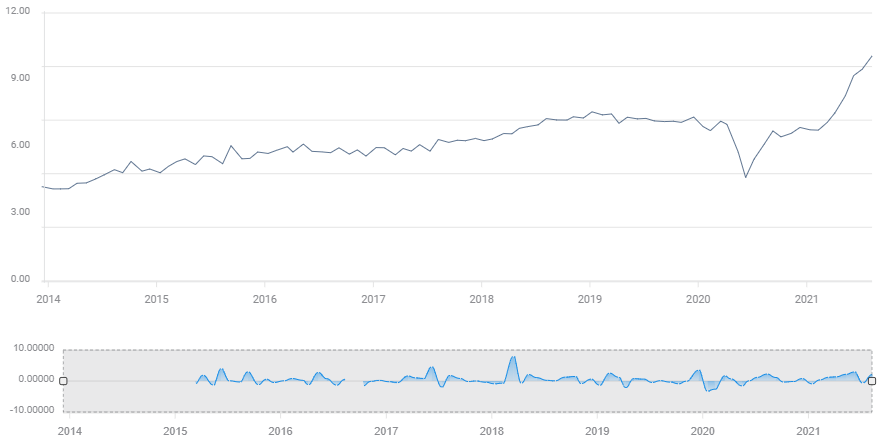

The PCE averages through June were 2.8% and 2.5% for core. These rates will rise as the year extends with much higher numbers in the final two quarters.

Core PCE

\

July’s PCE figures will be reported by the Bureau of Economic Analysis on August 27.

Market response

The dollar faded as the CPI report was released, losing about 30 points versus the Japanese yen, the euro and the sterling, falling versus the rest of the majors and maintaining those reverses into the early afternoon.

Equities rose with the Dow up 195.15 points, 0.55% to 35,458.82 at 121:56 pm, a new 52-week high. The S&P 500 had added 5.60 points to 4,442.35, also a new annual high.

Dow

CNBC

S&P 500

CNBC

Treasury yields moderated their increases of the last few days, with the 10-year losing 1 basis point to 1.33% and the 30-year increasing 1 point to 1.994%.

GDP and consumer spending

The US economy expanded at a 6.5% annual rate in the second quarter following the 6.3% pace in the first three months of the year.

Consumer spending rose 11.8% in the second quarter, as the vaccination program ended lockdowns and American responded with a burst of purchases, travel and activities from vacations to dining out.

Used car and truck prices, which rose rapidly in the first half of the year as new cars became scarce due manufacturing delays caused by computer chip shortages, moderated in July adding just 0.2%, after jumping 10% in June.

Clothing prices were unchanged following June’s 0.7% gain. The cost of transportation services dropped slightly after rising more than 1% inJune.

Conclusion

The slight moderation of CPI in July has not changed the economic background that will maintain much higher levels of inflation in the second half of the year.

Labor shortages, rising energy costs and widespread component and supply chain scaricities, will keep the pressure on businesses to maintain profit margins.

For instance, the leisure and hospitality sector, the hardest hit in the job losses of last year, still has more than 1.6 million openings.

Employers have been forced to raise pay or offer signing bonuses as the Labor Department reported 10.07 million unfilled positions in June, the highest on record for the Job Openings and Labour Turnover survey (JOLTS).

JOLTS

FXStreet

Firms have shown an ability and a willingness to pass some of these costs on to consumers instead of absorbing them as they have over the past decade.

If the July NFP report which is due September 3, provides another healthy dose of job creation, the Fed may be hard-pressed not to announce a policy shift at the September 21-22 FOMC meeting, regardless of the intervening inflation development.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

GBP/USD clings to recovery gains above 1.2650 after UK data

GBP/USD clings to recovery gains above 1.2650 in European trading on Friday. The mixed UK GDP and industrial data fail to deter Pound Sterling buyers as the US Dollar takes a breather ahead of Retail Sales and Fedspeak.

EUR/USD rises to near 1.0550 after rebounding from yearly lows

EUR/USD rebounds to near 1.0550 in the European session on Friday, snapping its five-day losing streak. The renewed upside is mainly lined to a oause in the US Dollar rally, as traders look to the topt-tier US Retail Sales data for a fresh boost. ECB- and Fedspeak also eyed.

Gold defends key $2,545 support; what’s next?

Gold price is looking to build on the previous rebound early Friday in search of a fresh impetus amid persistent US Dollar buying and mixed activity data from China.

Bitcoin to 100k or pullback to 78k?

Bitcoin and Ethereum showed a modest recovery on Friday following Thursday's downturn, yet momentum indicators suggest continuing the decline as signs of bull exhaustion emerge. Ripple is approaching a key resistance level, with a potential rejection likely leading to a decline ahead.

Trump vs CPI

US CPI for October was exactly in line with expectations. The headline rate of CPI rose to 2.6% YoY from 2.4% YoY in September. The core rate remained steady at 3.3%. The detail of the report shows that the shelter index rose by 0.4% on the month, which accounted for 50% of the increase in all items on a monthly basis.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.