US CPI: Fed rate cut remains in play, but 25 vs 50bps debate unsettled

Key points

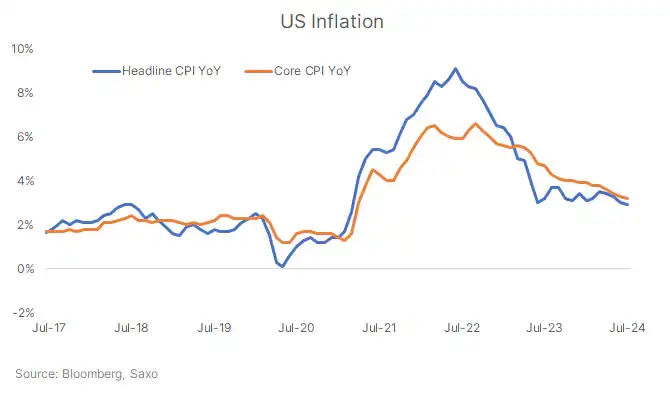

Disinflation progress: The latest US CPI report indicates a 2.9% YoY increase in headline inflation for July, slightly below expectations. Core CPI rose by 3.2% YoY, matching forecasts. On a MoM basis, both headline and core inflation increased by 0.2%, consistent with expectations, suggesting continued disinflationary trends.

Fed put remains in play: With the disinflation progress, a September Fed rate cut remains possible as the central bank tries to balance the risks on both sides if its mandate. There was nothing in the inflation report to derail a September cut despite some concerning trends on shelter and supercore inflation on a MoM basis.

Fed rate cut magnitude debate unsettled: The debate on whether the Fed cuts rates by 25 or 50bps in September is still unsettled. The decision will likely be influenced more by growth indicators than inflation alone. Upcoming data on retail sales, jobless claims, and the August jobs report will be crucial in determining whether the Fed opts for a 25bps or 50bps cut. We lean towards a 25bps rate cut barring a growth shock or another rise in unemployment rate.

Disinflation progress continues as expected

The latest US CPI report showed headline inflation rising by 2.9% YoY in July, slightly below the expected 3.0%. This marks the slowest annual inflation rate since March 2021. Meanwhile, core CPI, which excludes volatile food and energy prices, increased by 3.2% YoY, aligning with expectations and marking the lowest rate since April 2021. The 'supercore' metric, which focuses on services excluding housing, rose by 4.5% YoY, its slowest pace since February 2024.

On a MoM basis, both headline and core inflation rose by 0.2%, consistent with expectations. Taken together with the softness seen in wholesale inflation, or PPI, earlier in the week, these numbers suggest a mild downside bias for July core PCE which is scheduled for release on August 30. These reaffirms that the disinflationary trend is continuing, offering the Federal Reserve some reassurance that inflation is moving towards its 2% target.

There were a few red flags, however. Shelter costs, the largest component of the CPI basket, reaccelerated to 0.4% MoM, up from 0.2% in June. This resurgence in shelter prices could lead to higher overall inflation in the coming months, and would be worth keep an eye on. The supercore measure also picked up on a month-over-month basis, reaching a three-month high. However, a cooling labor market and slower wage growth could help to contain further increases.

Fed debate shifts to growth indicators

The disinflation progress is likely to keep a September Fed rate cut on the table. However, the debate on the magnitude of that rate cut is still unsettled.

While inflation remains a crucial factor, the Fed's next move may hinge more on growth indicators than inflation alone. The market is now closely watching upcoming data on retail sales, the weekly jobless claims and the August jobs report (due Sept 6).

These growth indicators will be critical in shaping the Fed's outlook, as they provide insight into the economy's underlying momentum and the ending debate around whether the US economy is heading for a recession or it can achieve a soft landing. The debate within the Fed about whether to cut rates by 25 or 50 basis points could be swayed by these growth figures, as they reflect the broader health of the economy.

Fed likely to lean towards 25bps cut, barring a growth shock

Given the current inflation dynamics and growth outlook, the Fed might lean towards a more cautious 25bps rate cut at the next meeting. The pace of disinflation was not compelling enough to justify a larger rate cut, and market has somewhat pared the expectations of a 50bps rate cut in September.

Although inflation is moderating, structural factors such as aging demographics, fiscal policies, and the green transformation could keep inflationary pressures alive in the medium to long term. Additionally, with growth indicators still presenting a mixed picture, the Fed may prefer a smaller cut unless there is a significant negative shock to growth. Another jump higher in the unemployment rate could also propel the Fed to cut by 50bps. But for now, it appears that a larger cut could be perceived as a sign of panic.

US Dollar to stay supported

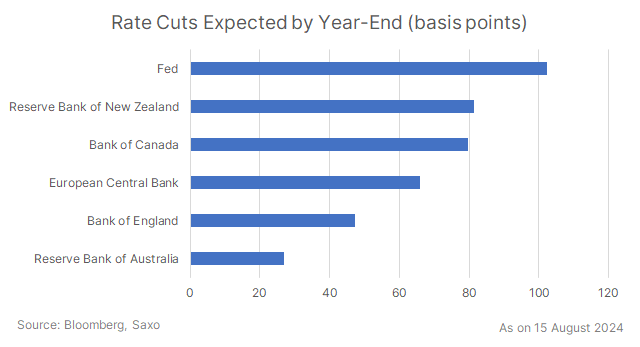

With the Fed's support measures still in place, there could be downward pressure on the US dollar. However, the market is currently anticipating a more aggressive rate cut cycle from the Fed compared to other major central banks. The expectation is for the Fed to reduce rates by 100bps by the end of the year, while the ECB is anticipated to cut by 65bps, and the BOE by less than 50bps. If Chair Powell takes a less dovish approach than the market expects, the US dollar might stay resilient. However, downside pressures could accelerate if growth data indicates more cracks in the US economy, which could lead to markets tilting their bias towards a 50bps cut in September more forcefully.

Watch for comments from Jackson Hole Economic Symposium starting August 22 for additional clues on Fed policy. This annual event organised by the Kansas City Federal Reserve gathers central bankers from around the world, academic economists and specialised media. It has served as an important and interesting forum to assess the effectiveness of central bank policy and explore new thinking and has also served as a platform to announce new policy directions. The topic for the event is "Reassessing the Effectiveness and Transmission of Monetary Policy"

Read the original analysis: US CPI: Fed rate cut remains in play, but 25 vs 50bps debate unsettled

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.