US Consumer Sentiment Preview: Index faces potential decline amidst mixed signals

- Economists anticipate a slight decline in the University of Michigan's Consumer Sentiment Index for November.

- The market and the US Dollar may weaken in response to concerning data.

- The US Dollar Index is recovering from below 105.00, but with limited strength.

The University of Michigan (UoM) will release the preliminary Consumer Sentiment Index for November, along with its crucial 5-year Consumer Inflation Expectations, on Friday, November 10, at 15:00 GMT.

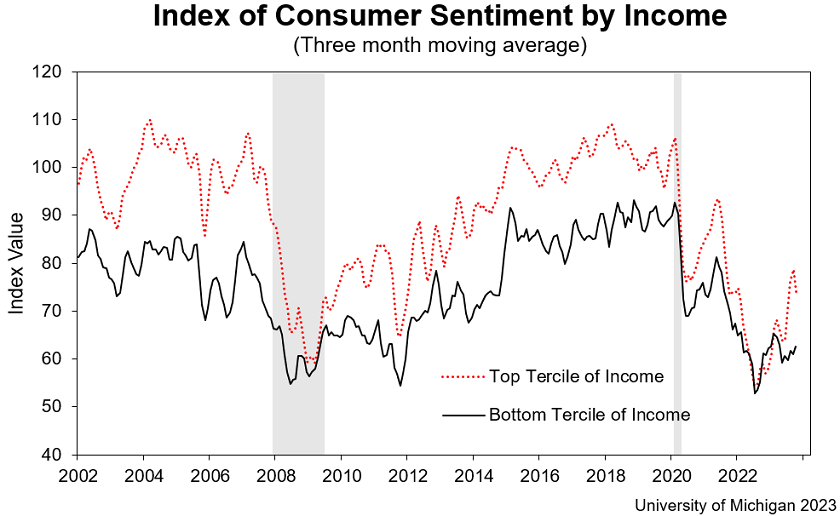

This early release presents an opportunity to gauge consumer sentiment ahead of the important holiday season. Market consensus is for a slight decline from 63.8 to 63.7. This level remains far from pre-pandemic figures and does not reflect the robust growth the US economy recorded during the third quarter, powered by consumer spending. It would be the weakest reading of the Consumer Sentiment Index since June and the fourth consecutive decline.

US Consumer: Spending with a sour face?

Since November, equity prices in Wall Street have been rising, with major indices reaching their highest levels since mid-September. Meanwhile, inflation has been gradually easing, and Crude Oil prices have significantly declined. While this could potentially have a positive impact, geopolitical risks may offset these factors.

Despite the moderation in consumer sentiment, consumer spending has been a key driver of Q3 GDP growth. The index peaked in July at 71.2 and has since gradually declined. A further deterioration in consumer sentiment could weigh on market sentiment and impact the US Dollar.

It will also be essential to watch the inflation expectations component of the report. Last month, year-ahead inflation expectations sharply rose from 3.2% (the lowest level over two years) to 4.2% (the highest reading since May 2023). Long-run inflation expectations (5-year) also edged up from 2.8% to 3.0%. Market participants will be interested to see if this rebound is sustained or if it resumes its decline.

Mixed signs from the DXY

The US Dollar Index (DXY) is currently rebounding after reaching levels below 105.00, for the first time since mid-September. The current recovery can be seen as a correction of the decline from 107.10 (November 1 high).

The US Dollar lost momentum following the FOMC meeting and weak US employment data, which reinforced market expectations that the Fed's tightening cycle is complete. However, with the US economy outperforming its European counterparts, strong fundamentals provide support to the USD, which could limit further declines.

From a technical perspective, if the DXY rises above 106.20, it will return to the familiar range of 105.50 - 106.80. However, if it remains below 106.00, there is a risk of further downside in the short term. The 105.00 area is a crucial support level; a break below it could target 104.45. On the upside, a break above 107.00 would pave the way for a test of the 2023 high at 107.34.

The University of Michigan Consumer Sentiment Index is not expected to have a decisive impact. Still, it could help either resume the DXY decline or provide a basis for a potential rally.

-638351327990099100.png)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.