US Consumer Price Index May Preview: Fed policy is set but there is room for surprise

- Annual CPI forecast to be unchanged at 8.3% in May.

- Core prices expected to drop to 5.9% from 6.2%.

- Steep oil and gasoline price gains in May tilt inflation risk upward.

- Fed tightening policy will be unchanged, markets could react to differentials.

April’s small decline in headline inflation, the first since last August, could be headed for oblivion in May as oil prices resumed their ascent with a 7.0% gain.

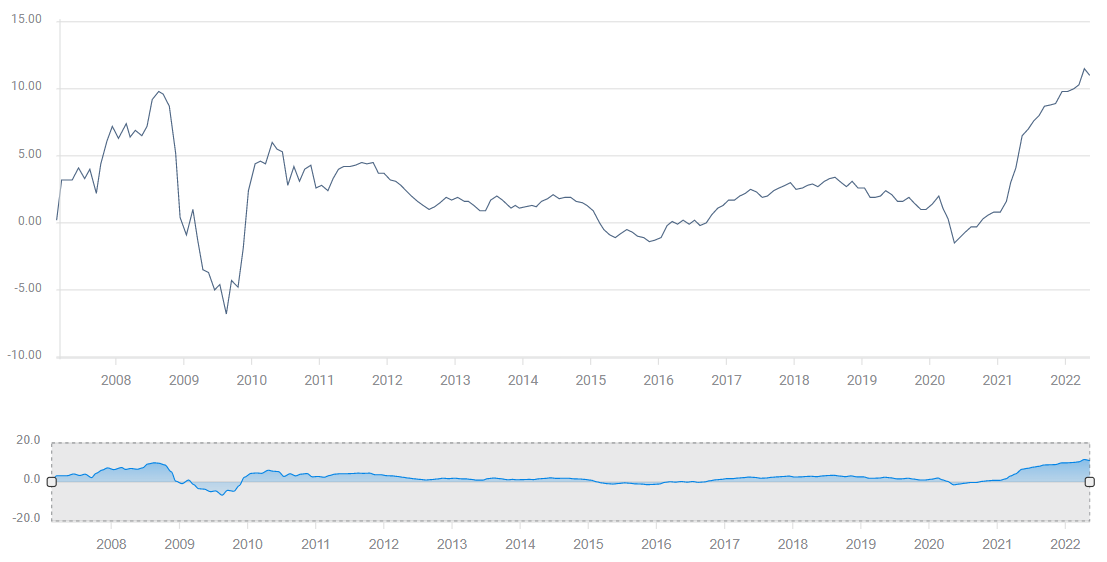

The Consumer Price Index (CPI) is forecast to remain at 8.3% after April’s inflation rate dropped from a four-decade high at 8.5% in March. Monthly prices are projected to rise 0.7%, more than double their 0.3% gain in April.

Core inflation, without the food and energy costs that have been in advance of general prices for more than a year, is expected to fall to 5.9% from 6.2% in April. The month’s increase is predicted to be 0.5%, just below the 0.6% gain in April.

Producer Price Index and West Texas Intermediate

Increases in the Producer Price Index (PPI) in the US have led CPI since January 2021 and have been forerunners of the gains in retail expenses.

The generalized inflationary environment over the past year has reduced or eliminated the prior tendency for producers and retailers to absorb a portion of manufacturing and distribution price increases to maintain market share for their products and stores.

Annual producer prices rose 11% for the year in April, and even though the May increase is expected to ebb to 10.7%, there is a considerable backlog of previous gains that have not been passed on to consumers. These prices will continue to filter through from the Producer Price Index (PPI) to the consumer index.

PPI

Oil and gasoline prices are another source of increased pressure on CPI in May.

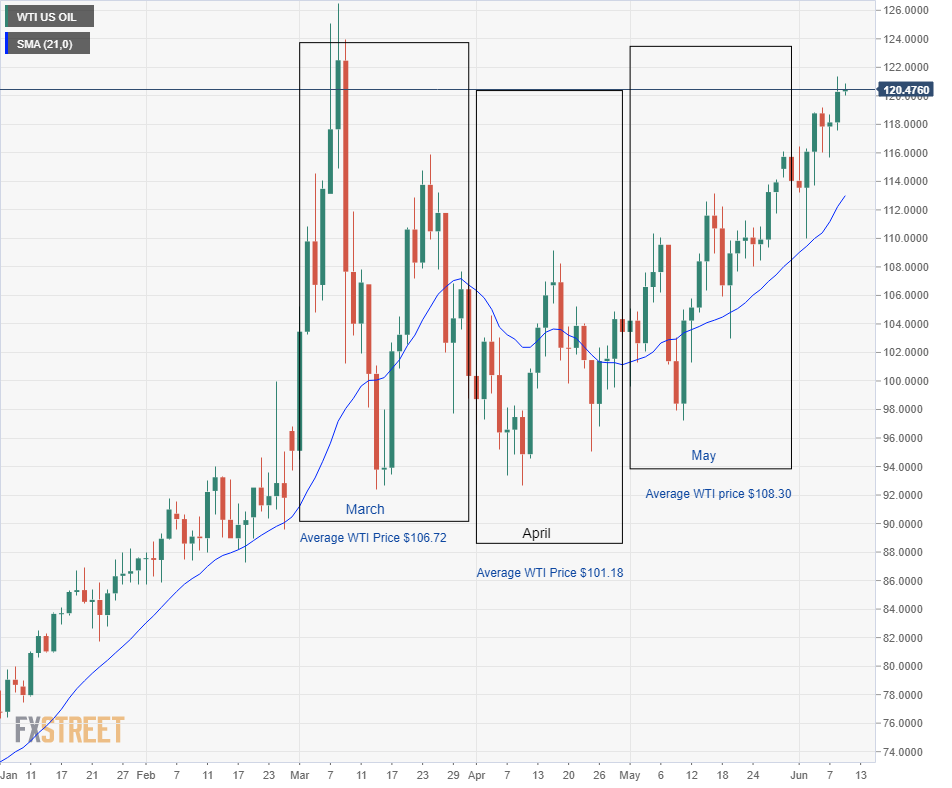

From March to April the average price of West Texas Intermediate (WTI), the North American crude oil standard, fell 5.2%. This helped to account for the decline in the consumer index from 8.5% to 8.3%. Because oil is such a ubiquitous industrial commodity, present in nearly all production and distribution endeavors, its price effect is much wider than can be eliminated by simply excluding its immediate costs as core inflation gauges do. From March to April core CPI fell from 6.5% to 6.2%, slightly more than the overall index.

Oil prices reversed in May. The average price for a barrel of WTI last month was 7.0% higher than in April with much of the increase coming in the second half of the month, unpredicted and unincorporated in analysts’ estimates.

WTI

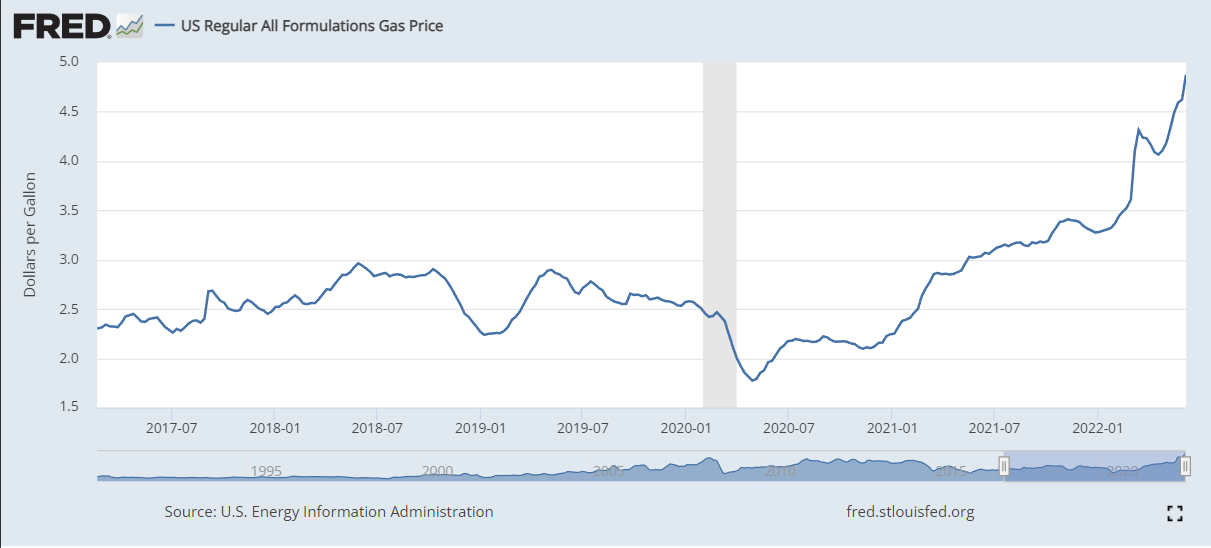

Gasoline prices were also climbing in May. The national average for a gallon of regular gasoline jumped 10.6% from the first week of the month to the last. That surge was likely not captured by the survey predictions formulated early in the month.

Federal Reserve policy

Federal Reserve policy is set for the next two meetings with 50 basis point increases expected at the June 15 and July 27 assemblies. Treasury futures have the odds for a half-point increase at the June 15 FOMC at 90.7% with the balance for a three-quarter point hike. At the July 27 conclave, the odds are 81.8% for a second half-point raise with 17.3% favoring three-quarters and 0.9% expecting a full point.

Next week’s Federal Open Market Committee (FOMC) on June 15 will also produce the bank’s second rate, inflation and GDP estimates for this year. In March the fed funds rate was expected to be at 1.9% at year end, with PCE inflation at 4.3%, core at 4.1% and GDP at 2.8%. It is safe to say that the first three will be higher and the last lower next week. The evolution will tell markets what the governors’ current thinking may be, but the Fed has been playing catch-up on inflation for more than a year and its predictions have been well behind reality. Most important will be the so-called central tendency for the fed funds rate. Anything less than 3.0% will be a major surprise.

Market reactions to CPI

Even though Fed policy for at least the next two meetings will not be affected by the CPI results for May or June, there is considerable room for a market response depending on the deviation from forecasts. Market risk lies primarily with a higher than predicted inflation number. There are good reasons to suspect that a portion of the May oil and gas price increases were not captured in the analysts surveys that produce the forecasts.

Treasury rates

Treasury rates have recovered from their swoon in the last two weeks of May. The yield on the 10-year Treasury has closed above 3.0% in two of the last four sessions and a higher than expected figure for May CPI could send the return on this commercial benchmark above the prior closing high of 3.13%.

A weaker than forecast CPI result will not push this or other Treasury yields lower for the plain reason that the Fed will be hiking rates for this year based on already existing inflation.

Currencies

The dollar has been mixed of late, rising sharply against the yen and the Bank of Japan’s (BoJ) moribund rate policy, but losing ground versus the euro. The ECB's relatively dovish policy choices on Thursday took some of the steam out of the united currency which closed at its weakest level in two weeks, though it is still more than two figures above its five-year low of 1.0350 on May 13. The greenback has lost points against the Canadian dollar since mid-May as oil prices had soared above $120.00.

Stronger American inflation plays to higher US interest rates, both immediately in the credit markets and long-term, in a potential higher endpoint for the Fed. Either way the most sensitive pair is the USD/JPY, though higher rates are an overall plus for the dollar.

Equities

Equities have largely priced in the Fed’s rate policy but higher inflation is a looming threat to the remaining percentage points of economic growth. The latest Atlanta Fed GDPNow estimate is 0.9% for the second quarter. It would not take much of a contraction in consumer spending, perhaps made necessary by shrinking purchasing power, to push the economy into a second quarter of decline and recession. The inflation threat to growth is an unpriced problem for equities. Translation: higher inflation, lower stocks.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.