US Consumer Price Index: Does weak inflation means weak demand?

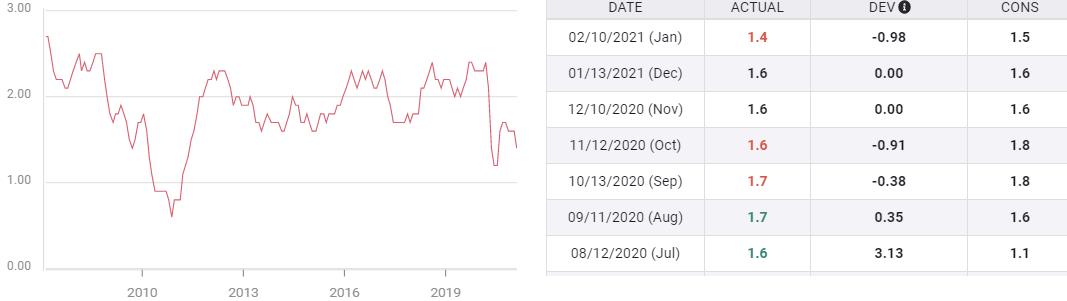

- Annual Core CPI falls to 1.4%, a seven-month low in January.

- Headline CPI drops to 0.3% on the month, stable at 1.4% yearly.

- Poor holiday Retail Sales prompted January price markdowns.

Inflation in January gave no indication that consumer demand is helping to bolster prices as the core rate slipped to a seven-month low and the headline pace was unchanged.

The Consumer Price Index rose 0.3% in January as forecast following December's 0.4% increase. Annually, the rate was unchanged at 1.4%, just under the 1.5% prediction.

After falling to 0.1% in May 2020 and 0.6% in June from 2.4% in January and February, CPI has averaged 1.32% for the past six months with a 0.2% range from 1.2% to 1.4%.

Core CPI, excluding Food and Energy, was flat in January on a 0.2% forecast and a 0.1% gain in December. The annual rate rose 1.4% in January following December's 1.6% increase. The estimate was 1.5%. The six-month range for Core CPI has been 1.4% to 1.7%. The January and February 2020 rate was 2.35% and the six-month average is 1.6%. Last month's annual inflation was the lowest since June.

Core CPI, YoY

FXStreet

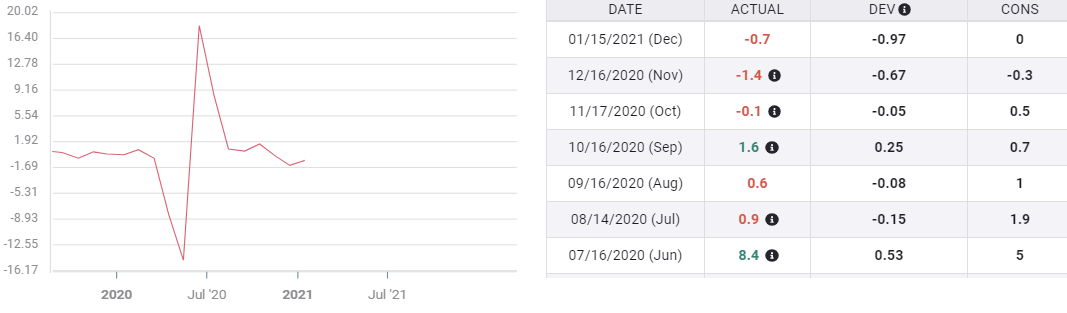

Retail Sales

Consumer demand slowed substantially in the fourth quarter as virus infections picked up in many parts of the country and California again shuttered its economy in December.

Retail Sales had recovered smartly from the spring economic closure rising more in May and June, 26.6%, than they has fallen in March and April, 22.9%.

After the replacement of the sales lost in the lockdown months sales averaged a healthy 1.03% in July, August and September.

However, in the final three month of the year that crashed into decline at -0.73%, including -1.05% for November and December holiday shopping season.

The January Retail Sales results will be reported by the Census Bureau on February 17 with 0.8% forecast for Sales and 0.4% for the Control Group after their 0.7% and 1.9% declines in December.

Retail Sales

Clearly the return of the pandemic and the renewed isolation had instilled a sense of caution in consumers despite the desire for cheer.

Inflation

Inflation's return has been more measured. Subsequent to the lockdown collapse in May and June when retailers were forced into drastic price cuts as consumers stopped shopping except for essentials, CPI has averaged 1.32% for six months, a bit over half (55%) its January and February rate of 2.4% and Core CPI has been 1.6% (68%) of its prior average of 2.35%.

The greater resilience of the core rate was because it did not collapse in the lockdown as the index was insulated from the plunge in food prices during and after the closure as retailers attempted to clear merchandise.

Conclusion and the dollar

Consumer prices in the New Year reflect the success or failure of the holiday season.

If retailers have unsold inventory they offer it at a discount in January. That was true this year with Retail Sales falling in November and December as parts of the nation revisited the unpleasantness of the spring and stores were forced to steep price reductions in January.

The currency market's view of the dollar is riding on the outlook for the US economy. Weak inflation is a reminder that consumer demand, upon which much depends, has not rebounded from its pandemic laced drop in the fourth quarter. Perhaps the January Retail Sales figures next week will provide reassurance.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.