US Consumer Confidence Preview: An uptick in confidence can boost the USD

- CB Consumer Confidence is expected to recover modestly in March after the first slide in four months.

- Financial markets seem to have fully digested the Federal Reserve’s caution

- US Dollar retreats from one-month high, preserves its bullish bias.

The United States (US) will publish March CB Consumer Confidence on Tuesday, expected to have improved to 106.9 from 106.7 in February. The report aims to provide detailed information on consumers’ attitudes and expectations, reflecting current business conditions and likely developments for the months ahead.

The February reading was a negative surprise as the index contracted from 110.9 in January while ending a three-month winning streak. According to the official release, the step back in consumer confidence was broad-based and reflected persistent uncertainty about the US economy. Breaking down the headline February figure, the Present Situation Index fell back to 147.2 while the Expectations Index slipped to 79.8, below the 80 level that is usually a sign of an upcoming recession.

On a positive note, however, “Average 12-month inflation expectations ticked down further to 5.2% in February. After peaking at 7.9% in mid-2022, expected inflation has now fallen to its lowest level since March 2020, when it stood at 4.5%.”

The report will likely have a diminished impact after the US Federal Reserve (Fed) unveiled its monetary policy decision last week alongside fresh growth, inflation and employment updates. The central bank kept rates unchanged as widely anticipated and acknowledged inflation will likely take longer to achieve policymakers’ 2% goal. Furthermore, officials upwardly revised their growth forecasts, hinting at a strong economy. That means the risk of a recession seems well-controlled at the time, regardless of the downtick in the CB Consumer Confidence sub-component. Finally, the US Fed signaled a rate cut is likely in the June meeting as policymakers still foresee rates down 75 bps through 2024.

USD possible scenarios

Meanwhile the US Dollar retains most of its recent gains. The American currency has gathered strength on the back of solid local data supporting the idea the economy will dodge a recession. Financial markets seem to have fully digested rates won’t come down as fast as previously expected. Encouraging US macroeconomic reports now tends to boost the USD rather than risk appetite.

With that in mind, a better-than-anticipated CB Consumer Confidence reading will likely help the USD revert modest Monday losses. A reading above January’s 110.9 will likely be the best catalyst for US Dollar demand. On the other hand, another contraction in the headline reading could put additional pressure on the American currency, although a USD sell-off remains out of the picture.

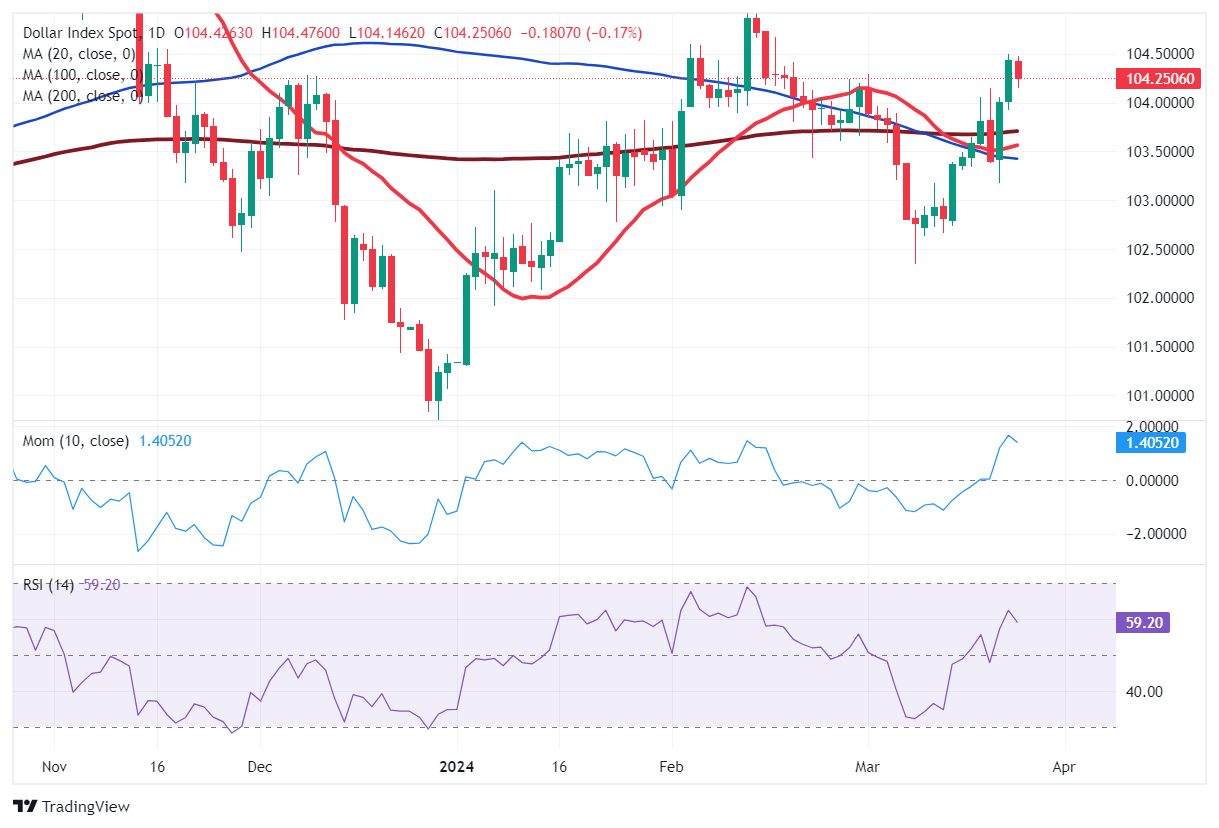

Ahead of the announcement, the Dollar Index (DXY) hovers near 104.20 after reaching a one-month high of 104.49 last Friday. According to technical readings in the daily chart, the decline remains corrective, with technical indicators retreating from their recent highs but still developing within positive levels. At the same time, DXY remains comfortable above its moving averages, with the 200 Simple Moving Average (SMA) providing strong support in the 103.70 region.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.